How Much Has Kalshi Actually Earned? Dissecting the Prediction Market Business Behind 200 Million Trades

TechFlow Selected TechFlow Selected

How Much Has Kalshi Actually Earned? Dissecting the Prediction Market Business Behind 200 Million Trades

From order book mechanisms and fee structures to regulatory gray areas—this is a comprehensive breakdown of the business logic behind this $11 billion–valued company.

Author: Sam Schneider

Translation & Editing: TechFlow

TechFlow Intro: Prediction markets are emerging as a new gambling infrastructure. Author Sam Schneider pulled all 203 million historical trades from Kalshi’s public API and found that over 82% of contract volume comes from sports betting, with the platform having accrued $545.6 million in trading fees. This article dissects the business logic of this $11 billion–valued company—from its order-book mechanics and fee structure to its regulatory gray zone.

Full Text Below:

Imagine it’s 2005, and you’ve founded a company called Meth Labs, Inc. You’ve acquired customers, raised venture capital—and suddenly, you’re listed on the New York Stock Exchange, ticker symbol $METH. People can buy or sell your stock—or even execute an iron condor. The NYSE provides a centralized marketplace where buyers and sellers transact as information flows continuously.

The above describes the NYSE—but there are many other stock exchanges (NASDAQ, LSE, SSE, etc.), all matching buyers and sellers of securities. In fact, markets are so essential to society that—even if you’re not a fervent day trader—you constantly interact with them. Uber connects intoxicated riders with drivers; Facebook Marketplace links people with secondhand furniture; and your dad is trying to connect you with a job.

Suppose you want to retire and sell your $METH shares to donate to charity. Who will buy them? At what price should you sell?

Markets do two things:

- They determine the price at which people are willing to buy and sell (price discovery).

- They provide a trading venue—because no one next door may want to buy your $METH (liquidity).

But what if the market doesn’t reveal a per-share price—but instead reveals the probability that a specific event will occur? That’s a prediction market.

Whether it’s scribbling bets on paper in an underground cockfighting ring—or using well-capitalized, centralized platforms like Kalshi and Polymarket—prediction markets differ fundamentally from stock trading:

- They’re binary: an event either happens or it doesn’t.

- Contracts settle when the event occurs, the outcome is determined, or the expiration date arrives.

You can’t buy $METH stock on a prediction market—but you can bet that $METH’s share price on January 6 will fall between $122 and $124.

Today, we’re buying a gun at Bass Pro Shops. Uh—sorry, Claude’s hallucinating again. Today, we’ll examine how billions of dollars are flooding into these markets; how FTX’s legacy lives on; what proportion comes from sports betting; and exactly how much Kalshi has earned. Let’s learn a new way to gamble.

History & Introduction

Kalshi and Polymarket launched in 2018 and 2020, respectively. Though these two now dominate the current duopoly, prediction markets have deeper roots. One pioneer is the Iowa Electronic Markets (IEM), operating since 1988.

Betting on your own “beliefs” might get you into trouble, but the wisdom of crowds remains a valuable forecasting tool. Consider Wolfers and Zitzewitz’s 2004 paper:

“These markets predict vote shares for Democratic and Republican candidates with an average absolute error of about 1.5 percentage points… Gallup’s final polls had a prediction error of 2.1 percentage points.”

Yet… for decades, something was missing—the piece preventing us from aggregating predictions, building markets, scaling to millions of users, and monetizing them. That missing puzzle piece is well-funded crypto Web applications offering you free groceries, letting you wager on whether the next pope will be transgender—just as Hayek envisioned in “The Use of Knowledge in Society.”

We’ll focus on Kalshi shortly—but other projects and protocols exist in this space.

How Does It All Work?

Prediction markets expand the surface area of human gambling. For example, I might bet $10 that I’ll drink ten beers before midnight—and my wife’s boyfriend might doubt me. I say “yes”; he says “no.” Swap me for LeBron James, beer for points, and midnight for game end—and you’ve got a real market tradable on Kalshi.

In Kalshi’s system, a market refers to a binary market settling as “Yes” or “No.” An event is a group of such markets, and a series clusters similar yet independent events. For instance:

- Highest daily temperature in Miami is a series.

- Each day within that series is an event.

- Each event contains multiple markets: e.g., “[68°–69°]” or “[69°–70°].”

Each market has both a “Yes” and a “No,” each with its own order book. What’s an order book? First, let’s clarify some terms…

Caption: Diagram of core Kalshi trading terminology

Every trade on Kalshi matches a Maker and a Taker—just like our “purely fictional,” absolutely never-happened scenario. On Kalshi, Makers and Takers bet against each other—not against the platform. You’re not buying stock—you’re buying a contract: $1 if correct, $0 if wrong.

As price-sensitive rational agents, I’m willing to risk $10 to win $20—and my wife’s boyfriend feels the same. Both sides post money, implying a 50% (10/20) probability for the event. Using “event contract” terminology:

- We split this into 20 $1 contracts.

- Each party locks up $0.50 per contract.

- At settlement, the winner claims the other’s $0.50.

As volume grows, tracking via order books becomes essential.

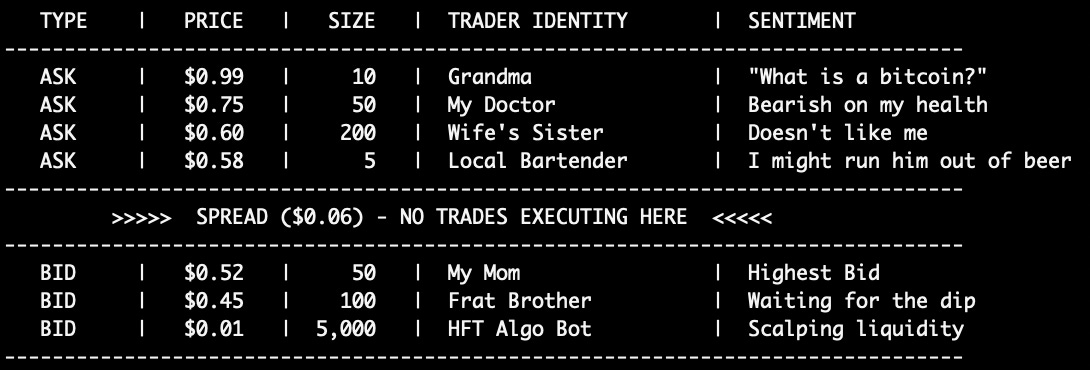

Caption: Order book schematic showing bid and ask orders

Order books can be visualized in many ways—typically displaying orders, whether bids or asks, quantities, and timestamps.

Bids represent all buyers; asks represent all sellers. In the diagram above, bids and asks are ranked from best to worst price. The gap between the highest bid and lowest ask is the spread.

In liquid markets (e.g., the Super Bowl), spreads may be just one cent. In illiquid markets, spreads widen because no one wants to stand on the opposite side—hence Kalshi’s incentives for liquidity providers and market makers.

Back to the order book: When a Market Taker sees $0.52 as a bargain, they match with my mom (visible on the bid side) for 50 contracts. The asset price “moves” to $0.52—and that bid disappears from the book. This is price discovery—or more precisely, the market pricing a probability. Gamblers update my liver failure probability to 52%. Here’s what Kalshi’s real order book looks like:

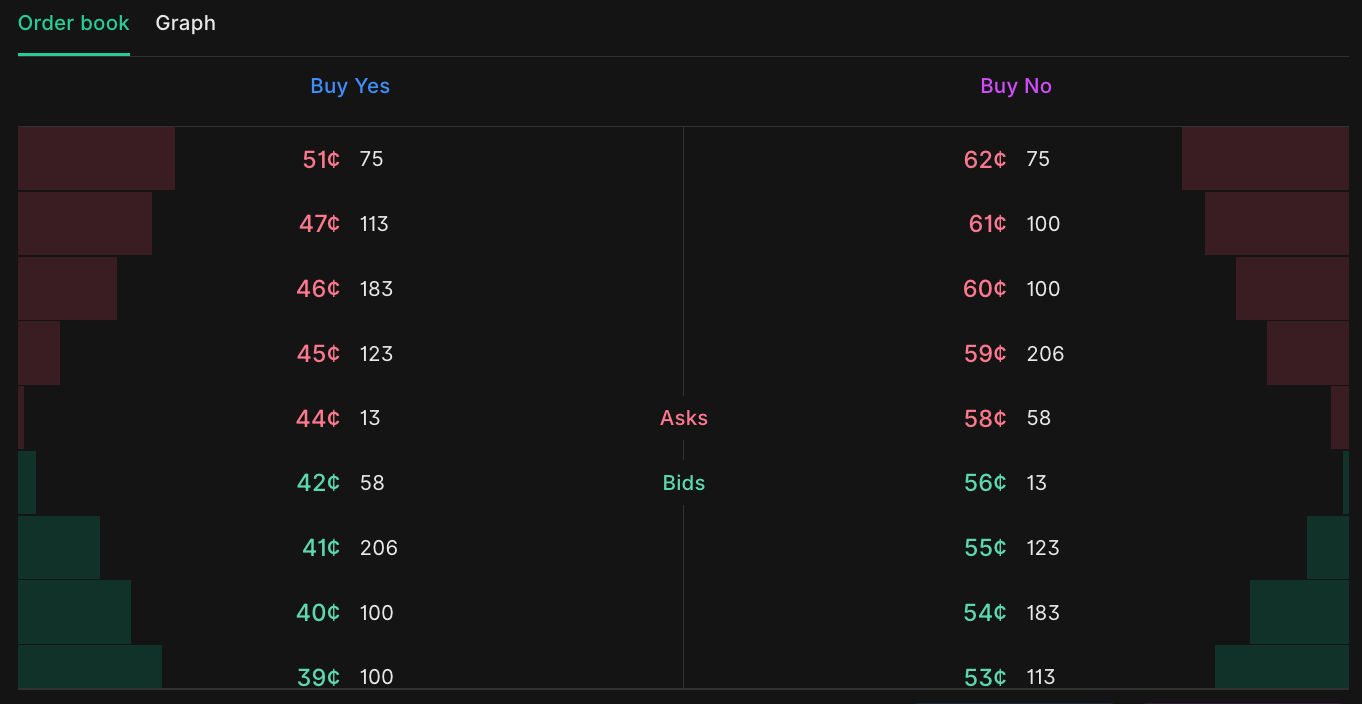

Caption: Real Kalshi order book interface—left side “Yes,” right side “No”

You’ll notice separate “Yes” and “No” sides. Kalshi contracts settle as “Yes” or “No,” and traders actively trade both sides.

- On the “Yes” side: 13 contracts offered at $0.44 (lowest ask); 58 contracts available at $0.42 (highest bid); spread = $0.02.

- On the “No” side: 58 contracts offered at $0.58 (lowest ask); 13 contracts available at $0.56 (highest bid); spread = $0.02.

Wait—that seems odd. Why are both sides perfect mirrors? Why do “Yes” bids and “No” asks have identical contract counts—and why do $0.42 + $0.58 = $1.00? Because buying “Yes” equals selling “No.”

Now that we understand orders—how does matching work?

Kalshi uses a price-time priority algorithm on its Central Limit Order Book (CLOB). On the surface, it sounds intuitive—orders sorted by price, then time. But building an exchange and processing massive order volumes is far from simple. For deep dives into matching engines, see DataBento’s guide. On Kalshi’s exchange, all orders require full collateral—so margin trading isn’t supported.

For a time, MIAXdx—a clearinghouse under MIAX—cleared Kalshi’s trades. MIAXdx was formerly LedgerX, acquired and rebranded by MIAX through… drumroll… FTX’s bankruptcy proceedings acquisition. Later, Kalshi decided, “We’ll build our own clearinghouse”—registering Kalshi Klear with the Commodity Futures Trading Commission (CFTC) in August 2024 and receiving approval. And here’s a full-circle twist: Robinhood recently acquired… LedgerX… from MIAX!

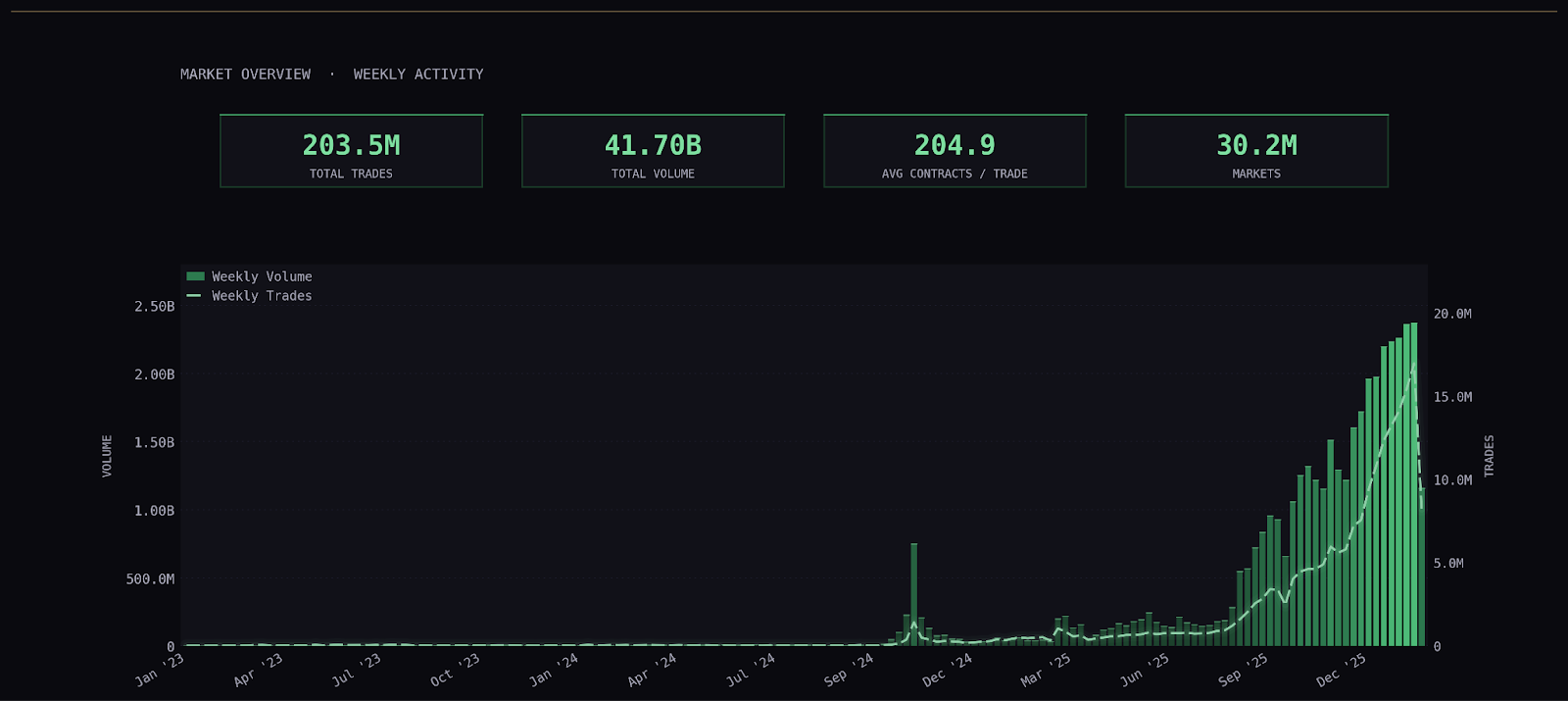

Data

I pulled historical data via Kalshi’s Markets API and Trades API: ~30 million markets, 203 million trades, total volume exceeding $41.7 billion.

Caption: Kalshi trading volume trend—total > $41.7 billion

Where does this volume come from? Kalshi’s own website and app drive significant traffic. It also partners with Futures Commission Merchants (FCMs)—intermediaries executing futures trades for clients. You likely know them: Robinhood (where you rolled over your IRA) Robinhood, WeBull (where teens trade crypto) WeBull, and Coinbase (where you hold altcoins) Coinbase.

By volume, #1 is the 2024 U.S. Presidential Election ($535M+); #2 is the 2026 Super Bowl Champion (~$244M).

Wait… Super Bowl… isn’t that… sports betting?

Isn’t This Just Sports Betting?

Kalshi is regulated by the CFTC (Commodity Futures Trading Commission), which oversees U.S. derivatives markets. I say “regulated”—but more accurately, it’s barely regulated. The Commodity Exchange Act (CEA) establishes the CFTC’s legal framework. This framework lets the CFTC ban onion futures—but also permits 18-year-olds to trade on Kalshi. Kalshi even boasts on its FAQ page that the “minimum registration and participation age” is 18+, directly comparing itself to… sports betting platforms. Sports betting platforms must navigate state-by-state regulations: some states ban it outright; others require bettors to be 18 or 21 (usually 21).

Okay—but Kalshi is different. You’re trading contracts with other people—not a house. And you can bet on anything—not just sports, right? I’m not playing against a bookmaker, right?

Caption: Kalshi contract volume by category—sports accounts for >82%

Over 82% of contracts are… sports. Kalshi runs on volume: more contracts traded = more fees earned. Even better—it’s the first gambling platform legally accessible to 18-year-olds. Oh, and they offer parlays, accounting for >5% of total volume!

As for “not playing against a bookmaker”—quote Kalshi’s article titled “Who Am I Trading Against on Kalshi?”:

“Another important participant on the exchange is Kalshi Trading. Kalshi Trading is a separate entity from Kalshi Exchange… They’re just another ordinary participant on the exchange, like anyone else.”

If it smells like a bookmaker, trades like a bookmaker—it probably is a bookmaker—*BANG*, author drops dead.

Back to the Data!

Market volumes follow a power-law distribution. Grouping total dollar volume by order of magnitude makes this clear.

Caption: Power-law distribution of market volumes, grouped by order of magnitude

Among zero-volume markets, 80% are parlay (Combos). Each parlay is a standalone market quoted via Kalshi’s RFQ system—many find no counterparties.

Using the same volume grouping, splitting by settlement result shows: higher-volume markets skew toward “Yes” outcomes.

This implies base probabilities lean toward “No.” Volume effects make sense too—an event with many sub-markets disperses volume across them, with only one or few settling “Yes.”

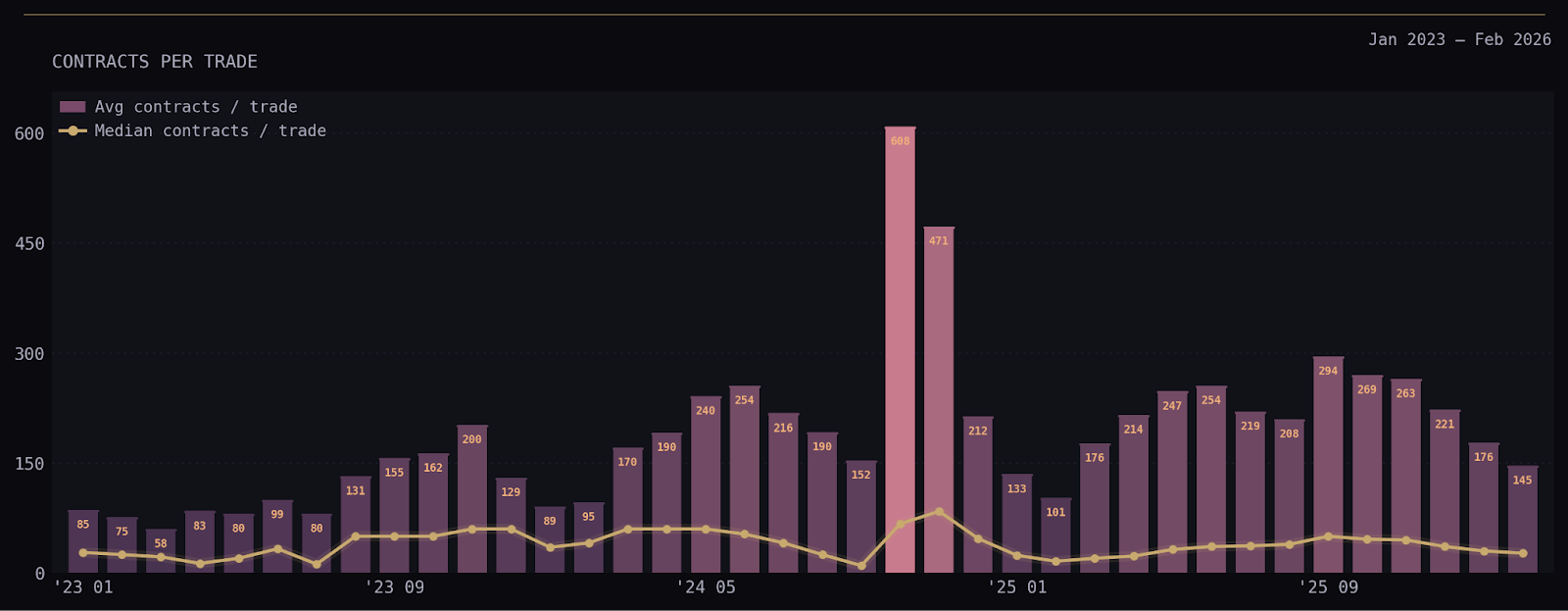

Average contracts per trade range between 150–250. A massive spike occurred in 2024 when someone placed a 1-million-contract order during the U.S. election. The median is far lower—under 50 for most months.

Caption: Average vs. median contracts per trade

Fee Comparison: Traditional Betting vs. Kalshi

If traditional betting resembles roulette—where the house profits from odds—Kalshi resembles poker: the platform takes a rake, indifferent to who wins or loses.

On traditional betting platforms, you’ll see “even money”—50/50 odds—for events like the Super Bowl coin toss. But the platform won’t give true 50/50 odds—instead quoting ~52.4% for both sides, above fair probability.

- In a fair market, you’d bet $10 on a coin toss and win $10. On a betting platform, inflated odds mean you win only $9.09.

When two people each bet $10 on opposite sides of a coin toss, one walks away with $19.09, the other with $0—and the platform pockets $0.91: 4.5% of total wagers. This is industry jargon: vig, juice, hold, etc.

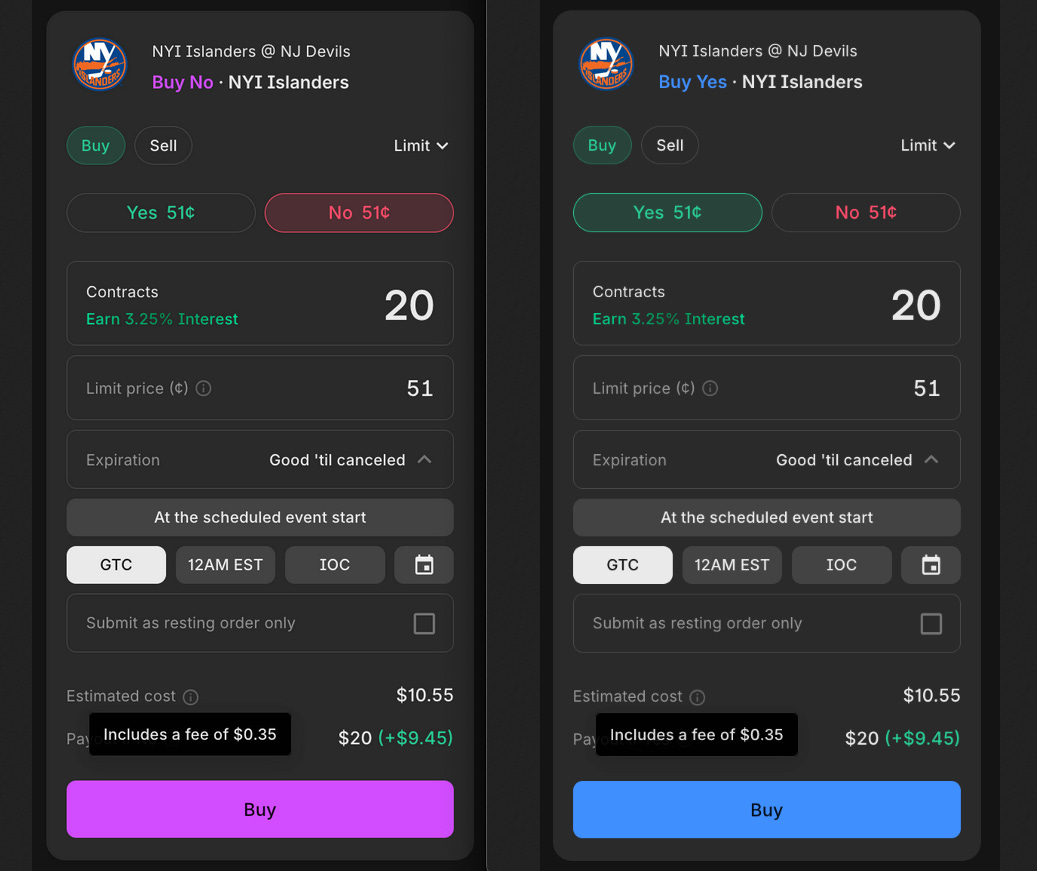

Example: Islanders vs. Devils—exactly 52.4%/52.4% on betting platforms. On Kalshi, the contract trades at $0.51 (51%). So you should trade on Kalshi—since 51% beats 52.4%, right?

Caption: Fee comparison—betting platform vs. Kalshi for the same game

No! Slightly worse odds on betting platforms are offset by Kalshi’s $0.35 taker fee:

- Kalshi: Bet $10.55 (20 contracts × $0.51 = $10.20 + $0.35 fee) → win $20

- Betting Platform: Bet $10.55 → win $20.14 (same stake, $0.14 more than Kalshi)

But that’s incomplete—Kalshi offers liquidity incentives and volume incentives. Plus, its fee schedule varies across markets—and Kalshi pays yield on open positions, compounded daily.

Fees: The Math

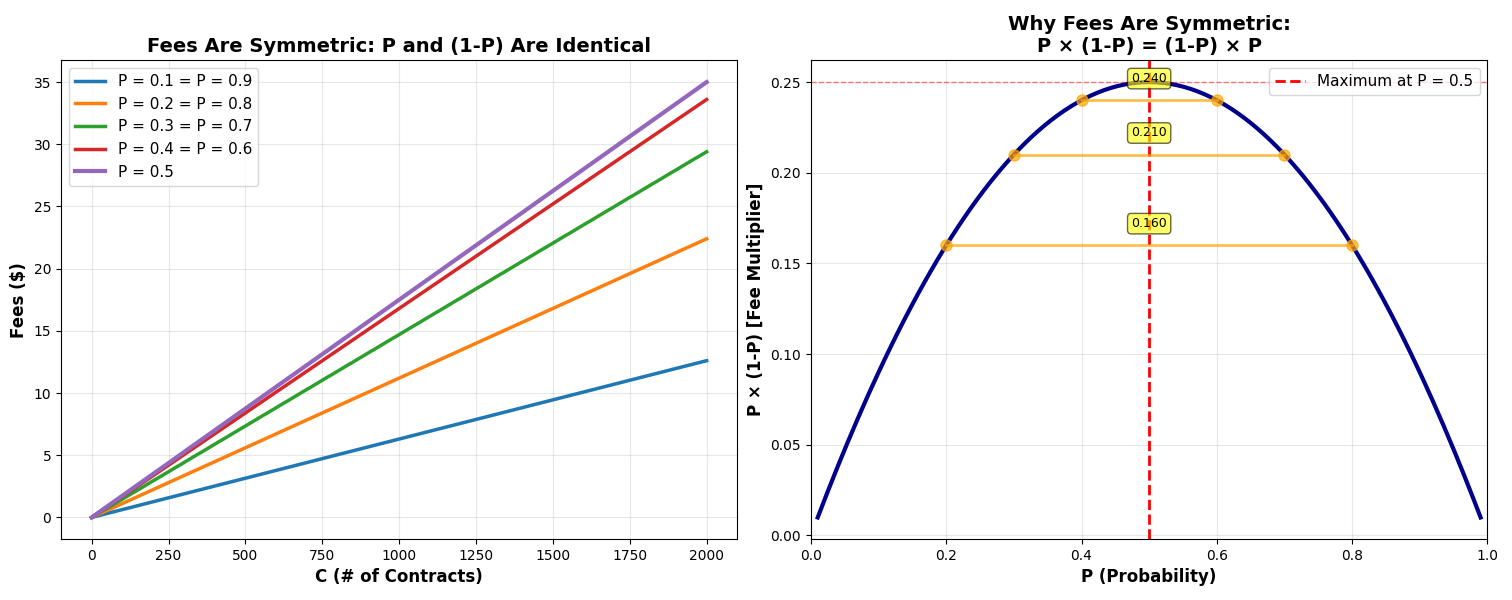

How much does Kalshi earn in fees? Start with taker fees. Formula:

Fee = ceil(0.07 × C × P × (1−P))

Where C = number of contracts, P = price (range $0.01–$0.99).

Plotting fee vs. P and C: fee rises linearly with C; P×(1−P) shapes the curve—showing fees drop as implied probability moves away from 50%. Highest and lowest probability contracts incur minimal fees.

Caption: Fee vs. implied probability and contract count; right plot shows P(1−P) curve

What we’re seeing here is the Bernoulli distribution, modeling a single “Yes/No” event (i.e., one market).

- Variance = P(1−P), where P = “Yes” probability—matching Y-axis on right plot.

- Variance ranges from 0 to 0.25.

- Entropy (uncertainty/randomness in probability distribution) peaks at P = 0.5.

Why doesn’t Kalshi use flat fees? Likely due to micro-level trading dynamics:

- If a contract trades at $0.98, max profit is just $0.02. A flat $0.02 fee yields zero profit—nobody trades.

Maker fee slope matches taker fees—but scaled down by multiplier 0.0175 (¼ of taker’s): Fee = ceil(0.0175 × C × P × (1−P)).

After downloading Kalshi’s full 203 million trades, I know every contract’s exact execution price. Plugging P and C into the formula gives Kalshi’s total revenue from all contracts: $545.6 million.

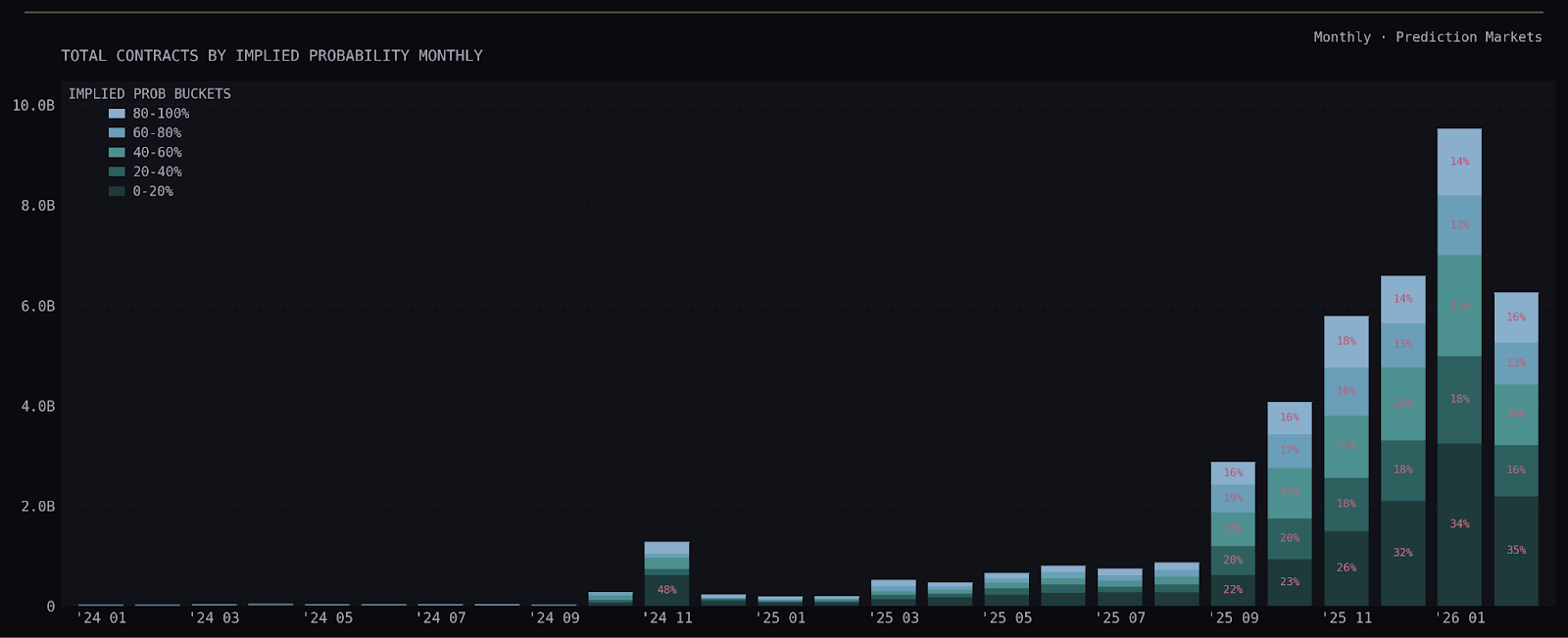

Kalshi’s monthly volume by implied probability distribution:

Caption: Monthly trading volume by implied probability

Kalshi’s monthly fee revenue:

Caption: Kalshi’s monthly fee revenue trend

Popularity of these markets is exploding—DraftKings, FanDuel, and Fanatics are rushing to join the party. The party’s name: “We do essentially the same thing as betting—but now it’s pseudo-regulated, and 18-year-olds can play.”

Settlement

An interesting settlement case: Dallas vs. Green Bay tied in an NFL game. The market settled at 50/50—neither “Yes” nor “No,” neither $100 nor $0. Prediction markets lack “push” or “void” concepts. In ambiguous cases, Kalshi intervenes. In the data, Kalshi labels such outcomes “scalar”—over 170,000 markets carry this tag.

Kalshi’s settlement process appears highly manual. A dedicated market team reviews results carefully. Each market cites authoritative reference sources. For example, the Super Bowl lists multiple data sources and specific rules. Yet they couldn’t determine whether Cardi B “performed”, ultimately settling at the last traded price.

Polymarket declared “Yes, she performed”, illustrating their differing resolution approach—using UMA’s optimistic oracle. We’ll explore that later.

Conclusion

That’s it—I still have nine beers to drink, and I’m already massively over word count.

Legal Sidebar: There’s another prediction market called PredictIt, focused on political forecasts. PredictIt is operated by Aristotle, a firm specializing in political campaign data mining. Launched in 2014 as a non-profit educational project by Victoria University of Wellington, New Zealand, it secured a no-action letter from the CFTC—similar to the one granted to the IEM—subject to restrictions and academic purpose requirements. Then in 2022, PredictIt was targeted by the CFTC for failing to operate per agreement. In 2025, they defeated the CFTC comprehensively in federal court—and “the Cadillac of prediction markets” returned.

In short, players in this “event contract” space are submitting various letters and letters to the CFTC, requesting non-enforcement for failing to meet standard reporting requirements. So far, the CFTC appears to agree, citing “limited applicability of traditional swap reporting rules to exchange-traded event contracts.” Other issues remain—like classification of Kalshi and Robinhood—but broader discussions on regulation, taxation, and reporting obligations for these “new” entities are ongoing elsewhere.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News