Semiconductors up 78% year-on-year, software down 12% year-on-year: “Liquidity siphoning” is unfolding within the tech sector

TechFlow Selected TechFlow Selected

Semiconductors up 78% year-on-year, software down 12% year-on-year: “Liquidity siphoning” is unfolding within the tech sector

Semiconductors—the true god of versions.

Author: Claude, TechFlow

TechFlow Introduction: The Semiconductor ETF (SOXX) has surged 78.5% year-to-date (YTD), while the Software ETF (IGV) has declined 12.5% over the same period—a spread of over 90 percentage points, marking an all-time extreme.

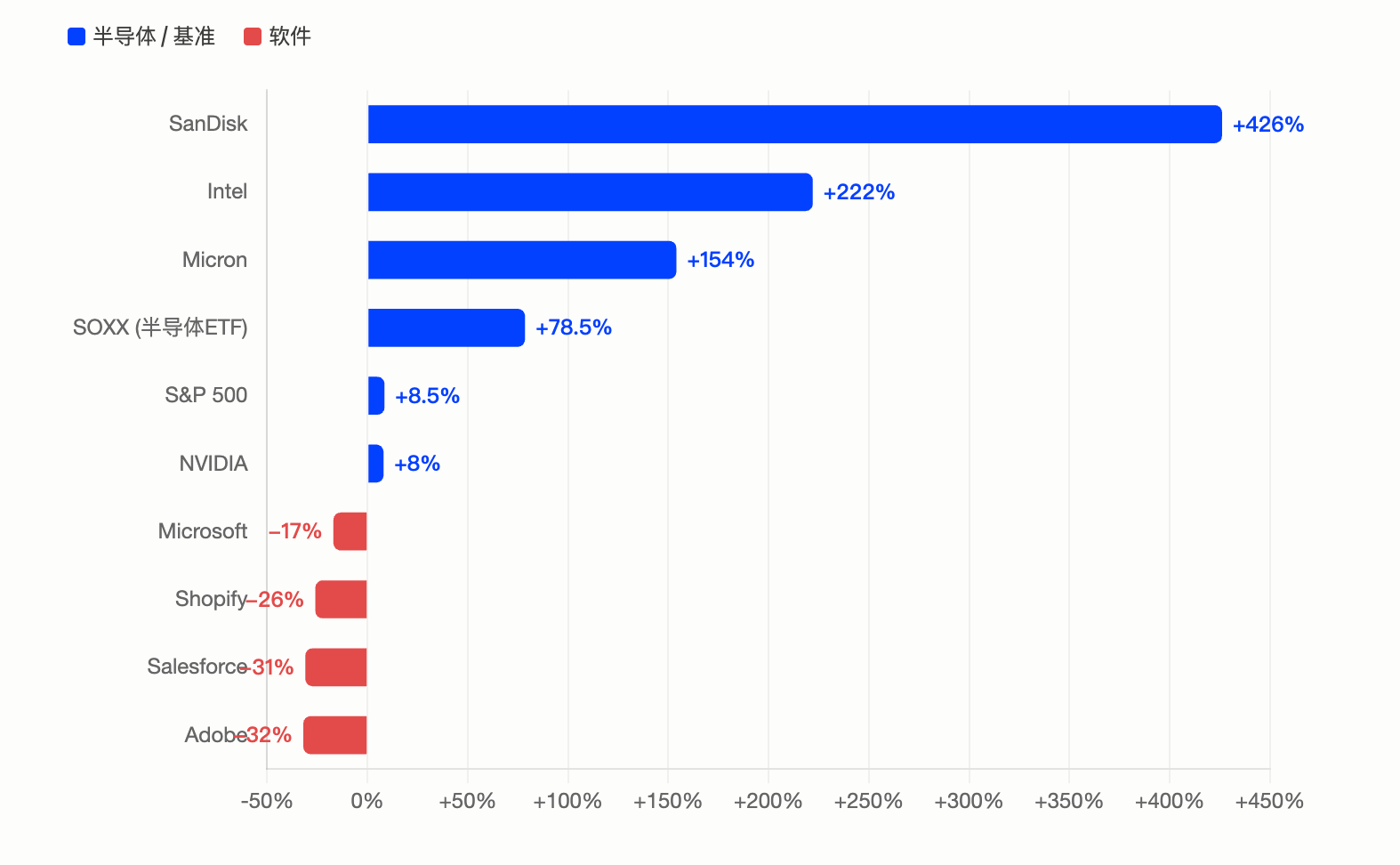

SanDisk led the S&P 500 with a 426% YTD gain; Intel tripled; Micron rose 154%; meanwhile, Microsoft, Adobe, and Salesforce each fell more than 17% YTD. The four hyperscale AI infrastructure companies are projected to spend nearly $700 billion on capital expenditures (capex) in 2026—capital flooding into the chip supply chain like a black hole, while the software sector faces a dual squeeze from AI substitution narratives and capital flight.

Recently, a top post on the investment subforum of Reddit overseas declared semiconductor stocks “basically a black hole sucking everything else away,” sparking widespread resonance.

Data validates this intuition. As of the market close on May 22, the iShares Semiconductor ETF (SOXX), which tracks the semiconductor sector, posted a YTD return of 78.5%, while the iShares Expanded Tech–Software ETF (IGV), tracking the software sector, delivered -12.5% over the same period. Despite both falling under the broader technology umbrella, their YTD performance gap exceeds 90 percentage points.

According to Tickeron, all S&P 500 software stocks currently trade below their 200-day moving averages, whereas approximately 89% of semiconductor stocks remain above theirs. Both sectors plunged together to zero during the 2022 bear market—but since then, their trajectories have diverged completely. This split was not gradual but explosive.

SanDisk Up 426% to Lead S&P 500; Intel’s Triple-Digit Gain Crushes AMD

The numbers at the individual stock level are even more staggering.

Per Benzinga Pro data, SanDisk (SNDK) rose ~426% YTD—the top-performing stock in the S&P 500 in 2026—and followed up its 559% surge in 2025 with another massive rally. This NAND flash memory specialist, spun off from Western Digital, saw NAND prices jump over 200% year-on-year amid AI-driven demand. Its fiscal Q3 revenue soared 250% year-on-year to $5.95 billion, with non-GAAP gross margin reaching a sky-high 78.4%.

Per 24/7 Wall Street, Intel (INTC) gained ~222–225% YTD—roughly double AMD’s gain. Intel’s rebound stems from an extremely low base, progress on its 18A process node, rumors of Apple foundry orders, and CEO Lip-Bu Tan’s disclosure on yield improvements during a CNBC interview. Short sellers were crushed: per S3 Partners, Intel’s market cap increased by over $440 billion since its March 30 low, inflicting over $12 billion in unrealized losses on shorts.

Micron (MU) rose ~154% YTD, with a cumulative 12-month gain of 661%. Earnings support this momentum: in its fiscal Q2 2026, Micron reported $23.9 billion in revenue—a 196% year-on-year increase—and adjusted EPS of $12.20, far exceeding the consensus estimate of $9.21. DRAM accounted for 79% of total revenue, with high-bandwidth memory (HBM) as the primary growth driver. SK Hynix Chairman Seok-Hee Choi even predicted that memory chip shortages could persist through 2030.

In contrast, NVIDIA (NVDA)—the true “cash printer” of AI compute—rose only ~8–15% YTD, significantly underperforming these second-tier semiconductor peers. Per The Motley Fool, NVIDIA’s current forward P/E ratio stands at ~21.5x, nearly identical to the S&P 500’s 20.3x. This signals that the market no longer assigns NVIDIA a growth premium; instead, capital is rotating into lower-valued, higher-leverage chip stocks.

$70 Billion Capex: The “Arms Race” Among Hyperscalers

The semiconductor rally is backed by real money.

Per Financial Times and aggregated institutional data, the four hyperscale AI infrastructure companies—Microsoft, Alphabet (Google’s parent), Amazon, and Meta—are expected to collectively spend between $650 billion and $725 billion on capex in 2026—nearly doubling from ~$410 billion in 2025. This represents the largest concentrated infrastructure investment cycle in tech history.

Per Tom’s Hardware, Jefferies analyst Brent Thill stated bluntly: “The AI economy is healthy. Bearish narratives are garbage.”

Breaking it down: Amazon led with $44.2 billion in quarterly capex, as AWS grew 28%; Alphabet spent $35.67 billion in Q1 capex—up 100% year-on-year—with Google Cloud backlog surging past $460 billion; Microsoft’s 2026 calendar-year capex reached $190 billion, including ~$25 billion attributable to rising storage chip and component prices; Meta raised its full-year capex guidance to $125–145 billion.

Per Om Malik’s blog, all three hyperscalers recorded large non-cash investment gains in their Q1 earnings: Alphabet booked $36.8 billion (mainly from Anthropic equity appreciation), Amazon $16.8 billion, and Microsoft $5.9 billion (from OpenAI). Though capex burns cash aggressively, the AI investment assets themselves continue appreciating.

Software Stocks Crushed by AI Substitution Narrative; IGV Posts Worst Drop Since 2008

The flip side is the brutal collapse of software stocks.

Per The Motley Fool, the software sector plunged sharply after Anthropic launched Claude Code early in 2026—not because markets rewarded AI innovation, but because they punished SaaS firms perceived as vulnerable to AI displacement. IGV briefly posted its worst decline since 2008.

As of late May, Microsoft was down ~17% YTD, Adobe ~32%, Salesforce ~31%, and Shopify ~26%. The S&P 500 Software & Services Index trades ~21% below its 200-day moving average—the widest deviation since June 2022. Per Goldman Sachs and other institutions, short positions in mid- and large-cap software firms have surged dramatically over the past three months, with cybersecurity and SaaS names attracting the heaviest shorting.

This divergence reflects two layers of logic. First is direct capital siphoning: market liquidity is finite. When $700 billion in capex pushes chip stocks into parabolic territory, capital must exit somewhere. As the Reddit poster put it: “Fundamentally sound software companies just sit flat or drift lower, while the semiconductor index shoots straight up.”

Second is a revaluation of narrative. Rapid advances in AI agents are forcing markets to reassess the moats of SaaS business models: when AI can autonomously code, fill forms, and handle customer service, how long can seat-based subscription models endure? The Motley Fool notes that surviving software firms will need genuine data assets, proprietary workflows, and deep customer integrations—attributes AI cannot easily replicate.

Peak Cycle—or Structural Shift? Two Key Questions Remain Unanswered

The Reddit user closed his post with two questions—the ultimate investor queries about whether the semiconductor rally can sustain.

Yet neither question has been answered.

First: How long can hyperscaler capex last?

Per CNBC, Pivotal Research forecasts Alphabet’s 2026 free cash flow will plunge ~90% year-on-year—from $73.3 billion in 2025 to $8.2 billion. Of Microsoft’s $190 billion annual capex, $25 billion alone is consumed by rising storage chip and component prices. These firms are betting future profits on AI revenue yet to fully materialize.

Second: Is software the next rotation target?

Per Bank of America CIO Michael Hartnett’s prior Flow Show report, software is among the best contrarian long opportunities for Q2 2026—given its extreme deviation from both its 50-day and 200-day moving averages.

That said, the semiconductor rally isn’t necessarily over. The Philadelphia Semiconductor Index (SOX) posted a record 18 consecutive trading-day gain streak ending April 25, rising ~45% during that stretch. Per Intellectia analysis, some veteran analysts have begun comparing the current pattern to the 1999–2000 internet bubble, warning of a potential 25–30% correction. Yet SOX won 22 of its last 23 trading days and set 15 intraday all-time highs—momentum itself serving as a signal.

As the Reddit user observed: “I don’t want to call a top—because I’ve been wrong too many times before. But when returns concentrate so heavily in one sector, it starts to smell like late-cycle.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News