Goldman Sachs Research Report Analysis: Semiconductors Beat Expectations Across the Board in Q2, But Stock Prices Already Priced In

TechFlow Selected TechFlow Selected

Goldman Sachs Research Report Analysis: Semiconductors Beat Expectations Across the Board in Q2, But Stock Prices Already Priced In

Understanding how much a company has risen previously is often more important than understanding how much it earned this quarter.

By: Rita

TechFlow Guide

In Goldman Sachs' latest Q2 earnings preview for US semiconductor stocks, it offers a somewhat contradictory judgment: nearly all sub-sectors are expected to beat earnings estimates, but this may not be good news. The reason is straightforward: the PHLX Semiconductor Sector Index rose 88% in Q2, while the S&P 500 rose only 14% during the same period; this gap has already priced in most of the positive news ahead of time.

What is truly worth reading in this preview is that the specific ratings given by Goldman Sachs have begun to decouple from the earnings expectations themselves. While both are expected to beat estimates, some companies remain bullish, while others are downgraded to neutral or even bearish; the dividing line lies not in earnings, but in how much the stock price has risen previously.

The three main lines Goldman Sachs is bullish on are semiconductor equipment, compute, and memory. Expectations for the analog chip line have also been raised overall. Compute benefits from upward revisions in capital expenditure by hyperscale cloud providers, with room for upward revisions in expectations for server CPUs and specific ASIC projects. In the memory line, Goldman Sachs favors hard drives and NAND flash, reasoning that there has been no significant new supply for these two product categories recently. In the semiconductor equipment line, Goldman Sachs expects WFE spending to pull forward shipments, with long-term visibility already extending to 2028. Regarding analog chips, Goldman Sachs prefers companies with greater exposure to industrial, aerospace & defense, and data center end markets; the logic is that the recovery pace of demand in these areas is more stable than consumer electronics, and the certainty of earnings realization is higher.

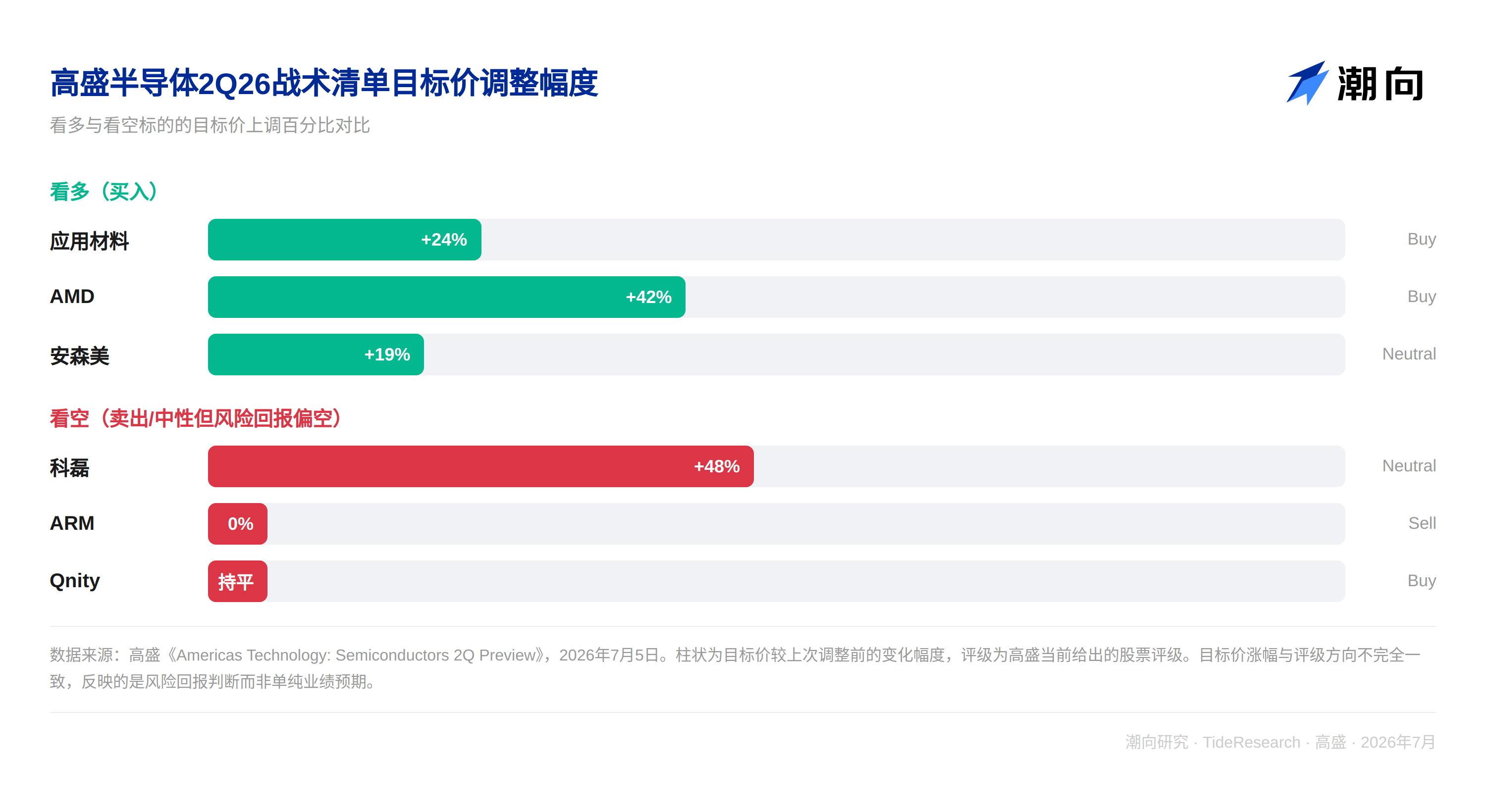

Same Beat, Diverging Ratings

In the tactical list given by Goldman Sachs, Applied Materials (AMAT), AMD, and onsemi (ON) are bullish, while the tier with weaker risk-reward ratios includes KLA (KLAC), ARM, and Qnity (Q).

Looking at the cases of ARM and KLA together best illustrates the issue. ARM's earnings themselves are not bad; Goldman Sachs believes its operational fundamentals are robust. The issues lie in two areas: first, the continued weakness in the smartphone market will drag down its licensing revenue, and second, operating expenses are higher than expected. Looking at these two points alone, it amounts to at most "Q3 guidance slightly below market expectations," not enough to warrant a "bearish" rating. What truly crushed the rating is the stock price; ARM's previous gains were already significant, pricing in optimistic expectations for several quarters ahead, so even a slight miss is enough to trigger a downgrade.

KLA represents another kind of decoupling. This round of equipment spending is focused on DRAM capacity expansion, and DRAM production naturally has lower demand intensity for inspection and metrology equipment compared to logic chips; this has nothing to do with KLA's own operational capabilities, but is purely a structural allocation issue of this round of capital expenditure. Even if earnings beat estimates slightly, it is highly likely to underperform peers. Although the target price was raised from $155 to $230, the rating remains just neutral.

Applied Materials, AMD, and onsemi Remain Bullish

The situation for the companies that remain bullish is exactly the opposite.

The logic for Applied Materials is that DRAM demand will drive it to become one of the top growth companies in the industry in 2026; Goldman Sachs sees visibility into 2028 and also believes there is room for price increases, with the target price raised from $520 to $645.

For the AMD line, server CPU demand will drive this quarter's earnings to beat estimates; even if the PC side may drag things down, the target price was raised from $450 to $640, and the 2027 earnings per share forecast is 13% higher than the market consensus.

onsemi represents another typical case; previously, due to rumors of acquiring Synaptics, the stock price once fell 30%, and market expectations were already set very low. Goldman Sachs believes this instead offers a good risk-reward ratio, with the target price raised from $80 to $95.

The common point among the three cases is that the stock prices had not previously risen to the extent of exhausting expectations, so beating earnings can truly be realized as stock price upside.

Memory Sector and Qnity: Two Extremes of Logic

The memory sector embodies this logic even more extremely. SanDisk's target price was raised sharply from $1,200 to $2,200, with the 2026 earnings per share forecast more than 30% higher than the market consensus; Seagate's target price was raised from $700 to $960. The logic for both is tight supply of hard drives and NAND, and continuously strengthening pricing. Western Digital's rating remains neutral, and the target price was also raised from $400 to $650, but the year-to-date gain has already reached 240%, significantly outperforming the PHLX Semiconductor Sector Index. This is why, despite equally positive earnings expectations, the rating cannot be raised to buy.

Qnity is the most subtle case in this logic. It is a wafer manufacturing materials company spun off from traditional materials business and listed independently. Goldman Sachs lists it in the rating maintain buy list, and its judgment on the improvement of foundry capacity utilization and operational execution is also long-term positive. But in the tactical grouping of this preview, Goldman Sachs still classifies it into the tier with weaker risk-reward ratios, reasoning that the stock price has already risen significantly previously, and the room for further upside is not as ample as before. This is different from the cases of KLA and ARM where the earnings themselves have flaws. Qnity is the only type among the three cases where "the company has no problems, the stock price has no problems, it is just no longer cheap,"恰好 completing the full spectrum of the decoupling of ratings and earnings: even with a buy rating, it does not mean that the stock price upside in the next period will be proportional to the degree of earnings realization.

TechFlow Perspective

What is truly interesting about this preview is that it inadvertently exposes a blind spot in institutional ratings: the rating itself measures the difference between earnings expectations and how much expectation the stock price has already reflected, not simply a judgment on whether earnings are good or bad. Neither ARM nor KLA are companies with deteriorating fundamentals; the former is backfired by its own gains, and the latter is dragged down by the structural allocation of this round of capital expenditure. Both have little to do with the companies' own operational capabilities.

Another point worth noting is that Goldman Sachs has or seeks investment banking business relationships with most of the companies mentioned in the report. Such interest relationships do not necessarily mean biased judgments, but when reading target prices and ratings given by institutions, a bit more independent verification is always correct.

For investors, the truly useful part of this report is to remember that in the same earnings season, beating expectations and whether the stock price can rise further are never the same thing. Understanding how much a company's stock has risen previously is often more important than understanding how much it earned this quarter.

Disclaimer

This article is a compilation and interpretation of third-party broker research reports by TechFlow Research. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the broker's analysts, represent only the position of their affiliated institution, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market has risks, decisions need to be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News