Goldman Sachs Research Report Analysis: SpaceX From Launch Provider to AI Computing Giant, Three Trillion-Dollar Markets Expanding Simultaneously

TechFlow Selected TechFlow Selected

Goldman Sachs Research Report Analysis: SpaceX From Launch Provider to AI Computing Giant, Three Trillion-Dollar Markets Expanding Simultaneously

SpaceX is no longer that "rocket-building company." Goldman Sachs defines it as a vertically integrated "Infrastructure as a Service" enterprise.

By: Rita

TechFlow Guide

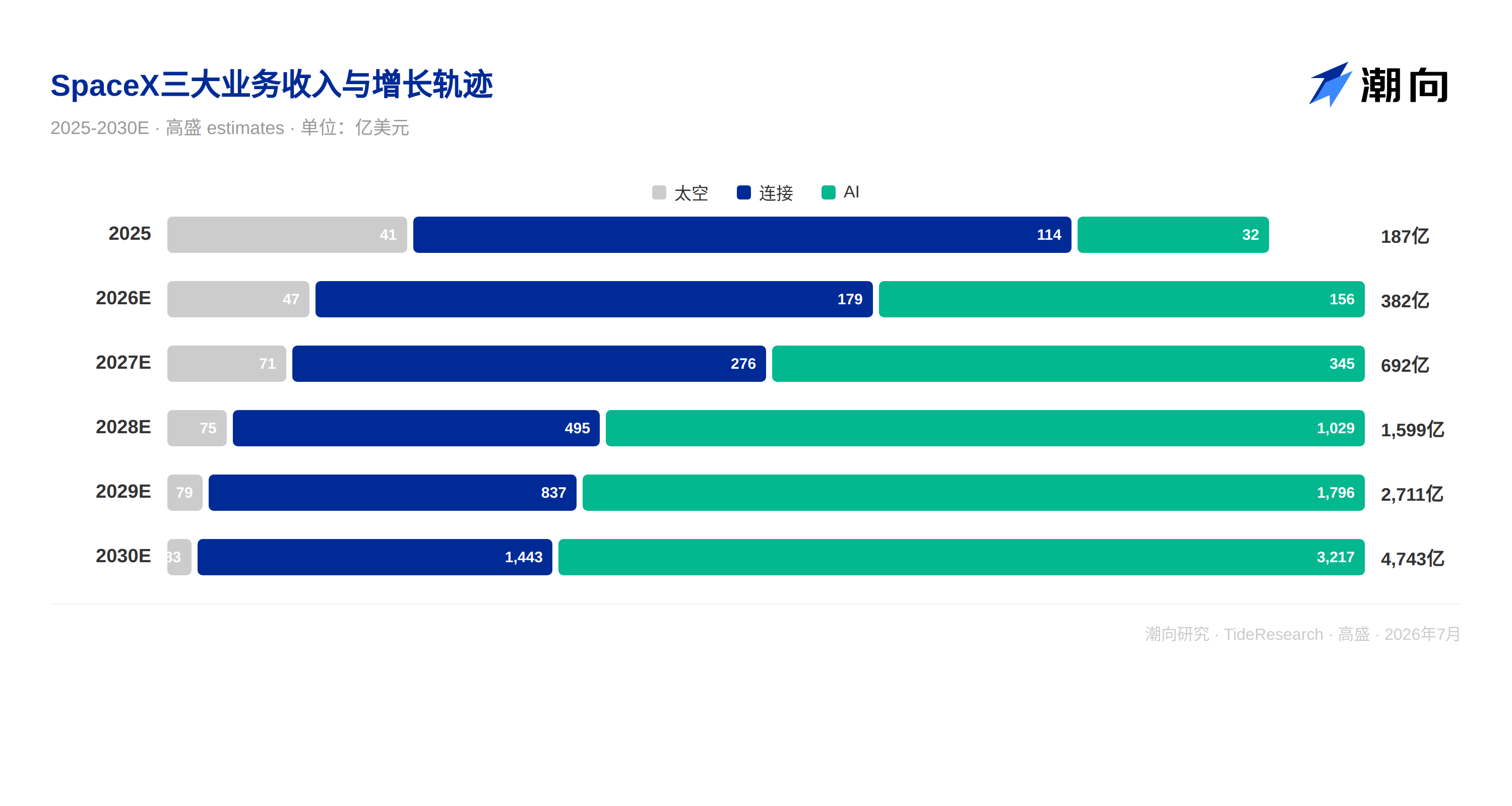

Goldman Sachs initiated coverage of SpaceX (SPCX) on July 7, giving a Buy rating with a 12-month target price of $205. Goldman Sachs pieced together the full picture of the company using three independent businesses: Space (launch and reusable), Connectivity (Starlink broadband and satellite mobile communication), and AI (computing power and X/Grok ads). Each business corresponds to a trillion-dollar level market, and SpaceX's vertical integration capability is causing chemical reactions among these three markets, using space capabilities to feed connectivity, and using connectivity to feed AI. SpaceX revenue in 2025 was $18.7 billion, estimated $38.2 billion in 2026, $69.2 billion in 2027, and surging to $159.9 billion in 2028.

The Three-Stage Jump from Launch Provider to AI Computing Power Giant

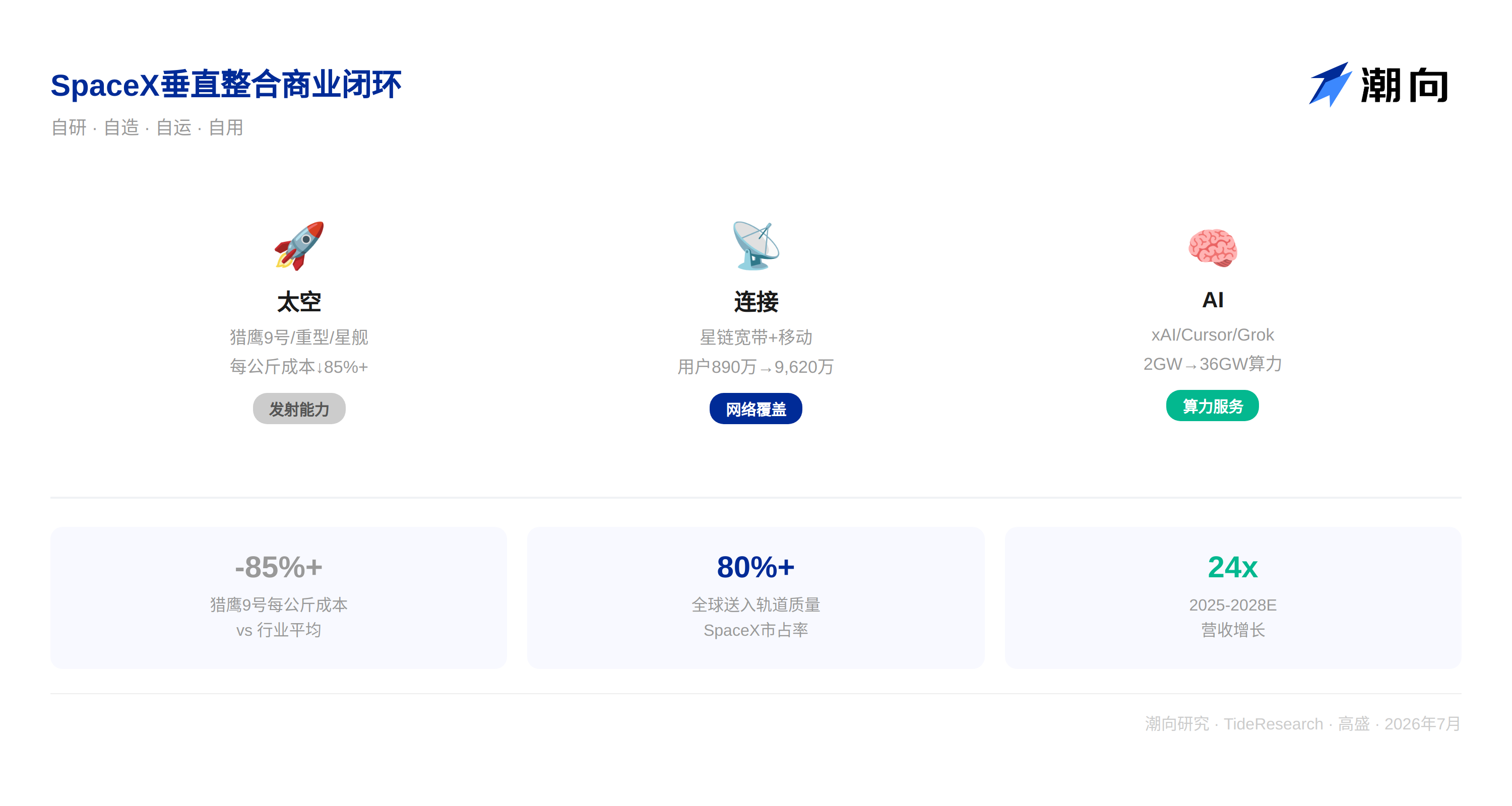

SpaceX is no longer that "company that builds rockets." Goldman Sachs defines it as a vertically integrated "Infrastructure as a Service" enterprise.

The first business is Space. Falcon 9 and Falcon Heavy rockets have executed over 658 missions, with a success rate of over 99%. Starship is moving from testing to commercial operations; Goldman Sachs expects about 100 Starship launches for connectivity business and over 9,400 for AI orbital computing deployment between 2026 and 2028. SpaceX currently accounts for over 80% of the global mass sent into orbit.

The second business is Connectivity. Starlink broadband users increased from 2.3 million in 2023 to 8.9 million by the end of 2025; Goldman Sachs expects it to reach 96.2 million in 2030, with the share of global broadband subscriptions rising from 0.7% to 6.5%. Starlink Mobile already has about 7.4 million monthly active connected devices, expected to reach 178 million connected devices in 2030.

The third business is AI. This is the biggest variable. SpaceX acquired xAI for approximately $250 billion in February 2026 and is simultaneously acquiring Cursor (AI coding tool). Goldman Sachs calculates SpaceX's AI computing power will expand from 2 gigawatts at the end of 2026 to 36 gigawatts in 2030, of which about 26 gigawatts will be orbital computing power. AI business revenue will surge from $15.6 billion in 2026 to $321.7 billion in 2030.

Goldman Sachs calculated the three businesses together: Space revenue increased from $4.1 billion in 2025 to $8.3 billion in 2030 (15% five-year CAGR); Connectivity revenue increased from $11.4 billion to $144.3 billion (69% five-year CAGR); AI revenue increased from $3.2 billion to $321.7 billion (107% five-year CAGR). Total revenue increased from $18.7 billion to $474.3 billion, growing 24 times in four years.

Vertical Integration: SpaceX's Core Moat

SpaceX's competitiveness does not come from a single business, but from vertical integration. It builds its own rockets, launches them itself, operates its own satellites, builds its own data centers, and trains its own large models.

On the space end, Falcon 9 reduced the launch cost per kilogram by over 85% from the industry average of $18,500. Starship's goal is to reduce it by another order of magnitude; Goldman Sachs calculates Starship's cost per kilogram in 2030 will be about $183, 99% lower than the industry average.

On the connectivity end, SpaceX deploys Starlink using satellites it launches itself, without needing to pay launch fees to any third party. On the AI end, SpaceX is collaborating with Tesla to advance the Terafab project, aiming to complete the design and manufacturing of AI chips internally.

This closed loop of "build it yourself, transport it yourself, use it yourself" makes SpaceX's cost structure naturally superior to any competitor.

Valuation and Risks: Assumptions Behind the $205 Target Price

Goldman Sachs priced SpaceX using a sum-of-the-parts valuation: Space business at 15x EV/Sales, Connectivity business at 24x EV/EBIT, AI business at 28x EV/EBIT, discounting each business's 2029 valuation by two years, arriving at a $205 target price. Upside scenario $295, downside scenario $95, risk-reward ratio 2 to 1.

Goldman Sachs expects SpaceX to achieve positive free cash flow only by Q4 2030, needing to issue approximately $270 billion in cumulative debt from 2026 to 2030. Regarding corporate governance, the CEO and founder holds majority voting rights, and related-party transactions (including cooperation with Tesla on developing Terafab and Macrohard) need continuous monitoring.

TechFlow Perspective

The most thought-provoking aspect of this Goldman Sachs report is what SpaceX's valuation is betting on? Among the three businesses, the direction of Space and Connectivity is relatively clear; Falcon 9 has verified reusability, and Starlink's user growth and revenue scale are supported by data. The real uncertainty lies in AI. The AI business lost $6.35 billion in 2025; Goldman Sachs expects it to turn profitable in 2028 and earn $81.3 billion in 2029. This profit leap comes from the scaled deployment of orbital computing power; starting from 2029, over 9,400 Starship launches annually will be needed to transport AI satellites. Orbital data center technology has not yet been verified; FAA launch permits are only 25 times per year (Starship base), and other launch sites are still under construction. Goldman Sachs' forecast implies the premise that technology, regulation, and manufacturing dimensions advance beyond expectations simultaneously.

Another point worth noting is the risk warning written by Goldman Sachs itself: the company CEO holds majority voting rights, the management team receives significant performance-based equity incentives, and related-party transactions are frequent (including cooperation with Tesla). Superimposed, these factors may cause the stock price to experience significant volatility.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of a third-party brokerage research report (Goldman Sachs, July 7, 2026). The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage's analysts, representing only their affiliated institution's position, not representing TechFlow Research's views, nor constituting any investment advice.

The market has risks, decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News