Are the “Magnificent Seven” no longer enough? Retail investors rush to buy SpaceX shares ahead of its IPO, while Wall Street unveils the “AI Tech Decacorn”

TechFlow Selected TechFlow Selected

Are the “Magnificent Seven” no longer enough? Retail investors rush to buy SpaceX shares ahead of its IPO, while Wall Street unveils the “AI Tech Decacorn”

Even within FAB 10, benefits may not be evenly distributed—the revenue-generating effect of new members could come at the expense of corrections for veteran members.

Author: Claude, TechFlow

TechFlow Intro: On its first trading day last Friday, SpaceX attracted $117 million in net retail buying—56% of all U.S. retail stock purchases that day. Research firm Vanda has since introduced the new concept of the “FAB 10,” proposing to replace the long-established “Magnificent Seven” with ten frontier AI and tech giants—including SpaceX, OpenAI, and Anthropic. The latter two are not yet publicly listed, but market expectations point to IPOs later this year, each potentially valued at over $1 trillion.

SpaceX’s debut on the public markets is reshaping how Wall Street labels technology stocks.

According to a report released by Vanda Research last Sunday and cited by Caixin Global, SpaceX’s IPO last Friday achieved remarkable success amid strong retail investor demand, sparking renewed debate about how to define the broader technology sector. Prior to listing, this roughly $75 billion offering had already become the largest IPO on record. Priced at $135 per share, SpaceX reached an estimated valuation of approximately $1.75 trillion—placing it among the world’s top ten most valuable publicly traded companies.

On Day One, Retail Investors Accounted for 56% of Total U.S. Retail Stock Buying

Vanda’s data provides quantitative backing for the frenzy. According to the report, SpaceX drew $117 million in net retail buying on its first trading day—56% of all U.S. retail stock purchases that day.

This figure reflects only secondary-market buying activity on Day One and excludes funds deployed by retail investors through broker-led IPO allocations. Additional data shows that retail investors secured around 20% of the total $75 billion offering—above the average allocation—while hedge funds received 10% and long-term institutional investors claimed 70%.

The concentrated retail bet has further channeled capital toward a select group of mega-cap tech firms. Vanda argues that these companies not only dominate equity market performance but also drive the broader wave of technology investment.

Vanda: Replacing the “Magnificent Seven” with the “FAB 10”

It is precisely this observation that prompted Vanda to propose a new classification framework.

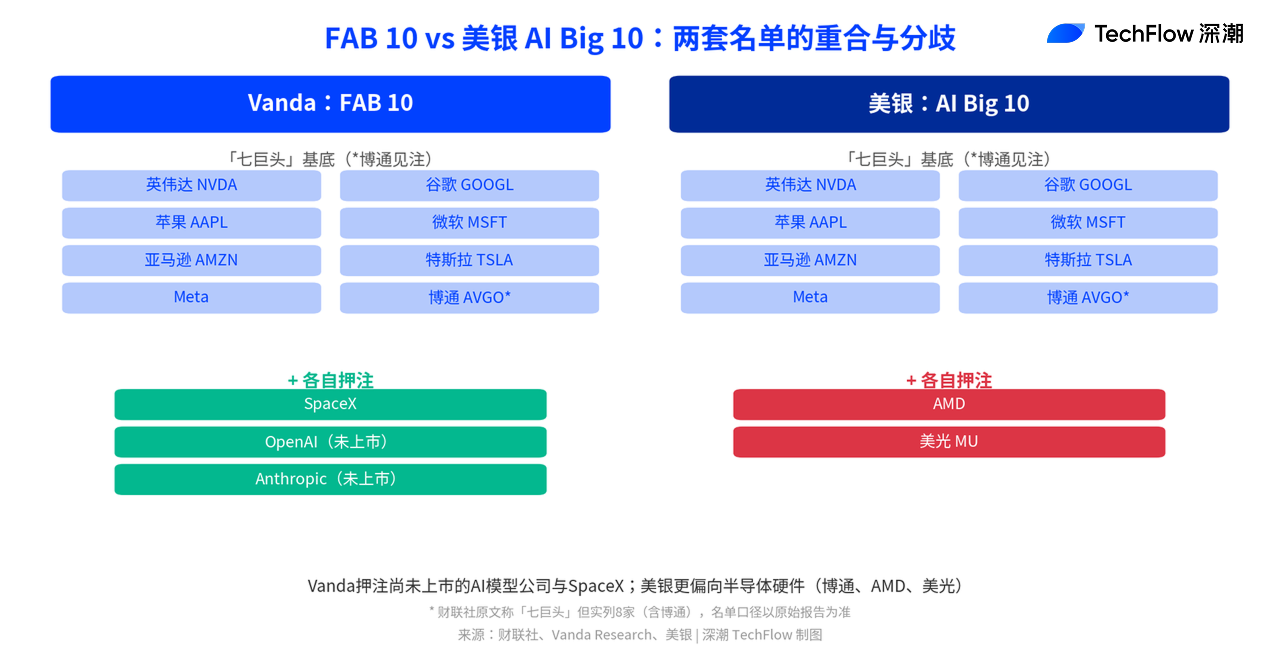

“If the market has been dominated by the ‘Magnificent Seven’ over the past few years, then last Friday may be the clearest signal yet that investors are beginning to focus on what we call the ‘FAB 10,’” Vanda wrote in its report. FAB 10 stands for “Frontier AI & Big Tech 10”—a cohort of ten frontier AI and technology giants.

Per Vanda’s definition, the FAB 10 expands the original Magnificent Seven to include SpaceX, OpenAI, and Anthropic. While the latter two remain private, market expectations anticipate their public listings later this year—with valuations potentially reaching hundreds of billions—or even over $1 trillion.

Vanda’s rationale is straightforward: collectively, these companies represent the direction of AI and technology over the next decade.

Different Interpretations of the Same Concept: BofA’s Version

Grouping mega-cap tech stocks into a new index isn’t Vanda’s exclusive domain.

Michael Hartnett, Chief Investment Strategist at Bank of America, previously proposed an “AI Big 10” basket in his *Investment Universe Guide*. Its composition differs from Vanda’s FAB 10: BofA’s version adds Broadcom, AMD, and Micron to the Magnificent Seven—tilting more heavily toward semiconductor hardware—whereas Vanda bets on pre-IPO AI model companies and SpaceX.

The divergence between the two lists reflects fundamentally different wagers on who will define the next decade—one side favors chipmakers; the other, model developers and rocket launchers.

Retail Influx into SpaceX May Drain Capital from Chip Stocks

The flip side of this new concept is capital reallocation.

Vanda analysts note that SpaceX’s surge could be siphoning funds away from other hot sectors—especially semiconductor stocks, which recently enjoyed sharp gains and may now be losing retail investor appeal. In other words, even within the FAB 10, capital distribution may not be evenly spread; the fundraising pull of new entrants could come at the expense of corrections among established members.

Analysts also caution that valuations across the broader tech sector already show signs of bubble-like behavior. SpaceX’s $1.75 trillion IPO valuation itself rests on optimistic assumptions about AI infrastructure—how long that optimism lasts remains an open question for the market to answer.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News