The Flip Side of the Printing Press: 84% of Polymarket’s 2.5 Million Accounts Are Losing Money

TechFlow Selected TechFlow Selected

The Flip Side of the Printing Press: 84% of Polymarket’s 2.5 Million Accounts Are Losing Money

When the World Cup drove overseas retail investors back to betting interfaces on Polymarket and Kalshi, another side of this expansion warrants closer scrutiny.

By Ada, TechFlow

With just seven days to go before the FIFA World Cup in the U.S., Canada, and Mexico, Polymarket’s single “World Cup Champion” market has already surpassed $1.6 billion in trading volume. According to a joint Q1 2026 report released by Bitget Wallet and Polymarket, the platform’s number of active wallets rose to 1.29 million, while its March 2026 trading volume hit $25.7 billion—13.5 times higher than the same period last year. Yet alongside this institutional narrative of a “money-printing machine,” another set of data—published separately by The Wall Street Journal, on-chain analysts, and academic teams from France and Canada—paints a starkly different picture: 70% to 84.1% of accounts are losing money; just 0.04% of wallets captured 70% of the platform’s profits; fewer than 2,000 accounts collectively netted nearly $500 million; the average retail user lost between $1 and $100; and the worst-performing 10% lost an average of $4,000 each.

As the World Cup draws overseas retail users back to Polymarket and Kalshi betting interfaces, the flip side of this expansion deserves closer scrutiny.

The Real Portrait of 1.29 Million Wallets: Behavioral Shifts Matter More Than Trading Volume

The report jointly released by Bitget Wallet and Polymarket on April 30 is, to date, the most comprehensive portrait of retail participants in prediction markets. Based on on-chain data from Dune Analytics, it covers all 1.29 million active wallets on Polymarket during Q1 2026.

In terms of trading volume, Polymarket’s nominal trading volume for March 2026 reached $25.7 billion—nearly 13.5 times higher than March 2025’s $1.9 billion. Yet Elden Mirzoian, Head of Growth at Polymarket, emphasized in the report: “The real transformation isn’t in volume—it’s in behavior.”

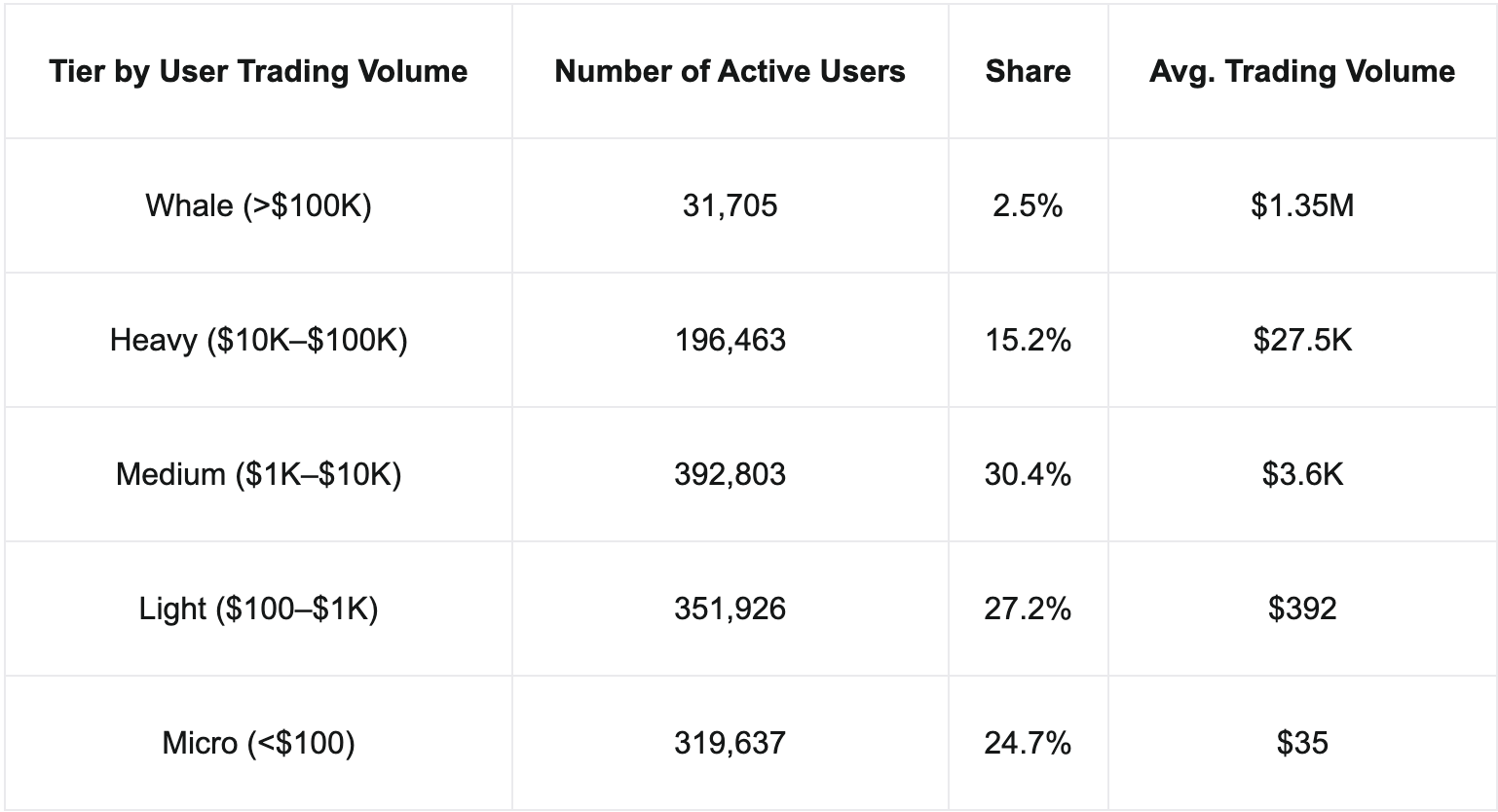

Specifically, 82.3% of users traded less than $10,000 in total across the quarter, and only 2.5% of wallets traded over $100,000 cumulatively. “Micro users” averaged just $35 per quarter; “light users” averaged only $392. The median single-trade amount fell between $2 and $3—roughly equivalent to buying a cup of coffee.

Behavioral stickiness metrics reveal a different growth structure. Quarterly active days per user rose from 2.5 to 9.9, and the average number of categories traded per user increased from 1.45 to 2.34. Polymarket COO Alvin Kan summarized: “Prediction markets are no longer about capital—they’re about sustained, repeated behavior. What we’re seeing is a behavioral shift: growth isn’t driven by larger individual bets, but by more frequent daily clicks.”

In short, this is a cohort of retail users who trade frequently, in small amounts, and across multiple categories. Sports emerged as the top category in Q1, generating $10.1 billion in volume; BTC-related event contracts attracted 593,000 users and generated $5.42 billion in volume—the largest crypto-specific entry point.

70%–84% of Wallets Are Losing Money: Three Independent Studies Point to the Same Conclusion

Beneath the surface excitement lies a highly skewed loss distribution.

Over the past six months, at least three independent studies have converged on the same conclusion: prediction markets operate as a pyramid where winners are extremely concentrated.

In December 2025, on-chain analyst DeFi Oasis analyzed 124 million trades across 1.7 million Polymarket wallet addresses and concluded that 70% of addresses realized losses, while fewer than 0.04% of wallets captured 70% of total profits—approximately $370 million.

In April 2026, on-chain researcher Andrey Sergeenkov published a larger-scale report via The Defiant, covering 2.5 million Polymarket wallets and refining methodology to better account for token splits and merges. Under this revised framework, the loss rate rose from 70% to 84.1%. That means fewer than one in every six Polymarket wallets achieved positive returns.

In May 2026, Wall Street Journal reporters Caitlin Ostroff and others published yet another analysis based on platform data—corroborating the prior two reports. Specifically, 0.1% of accounts captured 67% of total profits; fewer than 2,000 accounts netted nearly $500 million; the bottom 10% of users lost an average of $4,000 each; and the average retail user lost between $1 and $100. Kalshi itself has disclosed similar figures: for every winner on its platform, there are 2.9 losers.

An especially ironic detail emerges from Kalshi’s “mention markets”—markets betting whether a public figure will utter a specific word in a given setting. Barclays and third-party analysts conducted pricing efficiency tests on over 35,000 settled mention markets on Kalshi and found that “YES” contracts priced at 50% were only resolved favorably 40% of the time. In other words, retail users systematically overestimate the probability of such events occurring. Under the prototypical retail behavior of “buying YES at the initial price,” average losses reach 11%. In February 2026 alone, Kalshi users wagered $181 million on mention markets—including $28 million on President Trump’s State of the Union address, betting whether he would say “cartel,” “Somalia,” or “hockey.”

The Top of the Pyramid: Théo, Domer, and Automated Wallets

The faces at the pyramid’s apex form an intriguing contrast with institutional players.

The most famous is Théo, a former French bank trader. Bloomberg’s subsequent investigation revealed that the number of accounts under his control expanded from four initially identified to eleven. His cumulative profit from the 2024 U.S. election cycle totaled approximately $80–85 million—not the originally reported $48 million figure. His methodology involved commissioning private neighborhood-effect polls through civilian polling firms, deliberately sidestepping biases inherent in mainstream surveys. Polymarket CEO Shayne Coplan confirmed this in a December 2025 interview with CBS’s 60 Minutes: “Everyone said he was crazy—but he actually commissioned dozens of private polls.”

The highest-volume account in Polymarket’s history belongs to Domer (on-chain ID @ImJustKen), who has traded nearly 10,000 markets since 2007 across platforms including PredictIt and Augur. His nominal trading volume on Polymarket totals around $300 million, with net profits exceeding $2.5 million. During the week of December 22–28, 2025, he netted $100,000. In an interview with On Chain Times, Domer offered blunt advice to retail users: “You can start with $20—the worst that happens is you lose $20. No big deal.” His implication is clear: the performance gap between professionals and retail users stems not from win rates, but from disciplined capital management.

The top-ranked account by net profit on Polymarket is “kch123,” with a PnL of $11.78 million. Another account, “GamblingIsAllYouNeed,” shows cumulative winnings of $40.2 million, cumulative payouts of $35.3 million, net profit of ~$4.9 million, and an on-chain balance of ~$14.1 million (including principal), with a win rate of 53.3%. These numbers demonstrate that long-term seven-figure net profits are achievable on Polymarket—even with win rates barely above 50%—provided position sizing remains disciplined. A more dramatic case emerged in April 2026: the account “Beachboy4” earned $6.12 million in a single day from sports contracts tied to Tottenham Hotspur and Sunderland matches—fully erasing its prior cumulative loss of $688,000.

Yet these stories remain outliers. Empirical research by Spain’s IMDEA Software Institute shows that the vast majority of high-profit wallets on Polymarket run arbitrage bots, market-making algorithms, or high-frequency trading systems. The fully public on-chain order book gives algorithmic traders a systematic advantage: quant wallets equipped with low-latency APIs and probabilistic models operate on a completely different playing field from the average retail user who casually opens a web page.

170+ Tools and Copy-Trading Bots: Retail Users Arm Themselves

Faced with this structural asymmetry, retail users are arming themselves in return.

A January 2026 Tencent News survey found over 170 tools, bots, and products built around Polymarket. Telegram-based copy-trading bots have become the most active entry point in Chinese-speaking communities.

OkBet was the first product to fully integrate Polymarket order placement and copy-trading into Telegram, charging a transparent 1% fee per transaction and managing private keys via Google Cloud KMS encryption. Polygun acquired the independent analytics tool Polymarket Analytics in early 2026, bundling “smart-money identification” and “auto-copy trading” into a single product. Kreo added daily loss caps and stop-loss rules on top of copy-trading, supporting both Polymarket and Kalshi. PolyHub (a Hubble subsidiary) focuses exclusively on identifying smart-money addresses. Others include Polycule (collaborative betting), Predictify Bot (AI-powered alerts and order management), and Bankr (AI agent integration).

Yet copy-trading bots are far from foolproof. CryptoRank and BlockTempo’s March guide highlighted three common pitfalls:

First, inflated PnL metrics. Polymarket involves multiple on-chain operations—buying, splitting, merging, and redeeming—and incorrect metric selection in tools can produce order-of-magnitude errors. Second, hedging interference from arbitrage bots. Addresses listed as “automated AI trading bots” on leaderboards often profit via cross-market arbitrage, with every trade offset by a hedge. Copy-traders replicating only one leg assume asymmetric risk exposure. Third, high win rates ≠ high expected returns. Some addresses specialize in markets with >98% win rates nearing settlement, capturing tiny spreads of $0.02. After fees, copy-traders may end up losing money.

A more fundamental physical constraint is Polymarket’s $1 minimum trade size. If the copied wallet holds $100,000 and allocates 0.5% ($500) per trade, a copy-trader with only $100 cannot allocate the proportional $0.50—below the minimum unit and therefore unexecutable.

A mature referral ecosystem has also taken shape in Chinese-speaking communities: polymarketcn.com offers step-by-step tutorials covering registration, deposits (direct via Binance/OKX), withdrawals, and arbitrage strategies—primarily targeting Chinese users unable to deposit USD directly via bank transfers.

The World Cup’s Next Stress Test

Seven days before kickoff, prediction markets face their largest event-driven traffic surge since the 2024 U.S. election. As of publication, Polymarket’s “World Cup Champion” single market had accumulated $1.6 billion in volume, with $7 million traded in the past 24 hours and $46 million in liquidity. Odds currently show Spain and France tied at ~16–17%, England at ~11–13%, and Argentina and Brazil hovering between 9–12%. Polymarket has launched over 100 specialized markets for this tournament—including 12 group-win contracts, Golden Boot markets, and appearance contracts for Messi and Yamal.

Notably, the latest two independent analyses of retail win rates on prediction markets align almost exactly with UK gambling regulator statistics on traditional sports betting published in 2024. In other words, retail users’ rate of loss on prediction markets closely mirrors that of casino patrons in traditional gambling. Polymarket’s own product page highlights: “The platform accurately predicts final outcomes one month in advance 94% of the time”—a claim rooted in the market’s function as an aggregated signal. But from the perspective of individual retail profitability, market accuracy and personal trading performance are entirely separate propositions.

Prediction markets are exceptionally accurate signal machines—a point Polymarket and Kalshi repeatedly emphasize. They are also financial arenas where 84% of users lose money—a fact equally well-supported by data. As the World Cup draws global retail users back to the table, institutions, market makers, and arbitrage bots are waiting for them.

Bernstein estimates the sector’s long-term TAM at $1 trillion. If that figure proves correct, the corresponding outflow of net funds will originate from those 84% of wallets.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News