When Futu Becomes a Dating Corner, Overseas Identity Becomes the New Currency for China’s Middle Class

TechFlow Selected TechFlow Selected

When Futu Becomes a Dating Corner, Overseas Identity Becomes the New Currency for China’s Middle Class

Overseas identity has become a bargaining chip in matchmaking.

Author: Xiao Bing, TechFlow

On May 22, following the China Securities Regulatory Commission’s (CSRC) announcement of proposed severe penalties against three overseas brokerage firms—Futu, Tiger Brokers, and Longbridge—their stock prices plummeted.

Yet within Futu’s own app community, the tone shifted dramatically: it was no longer just a platform for stock discussions—it overnight transformed into a matchmaking hub for retail investors.

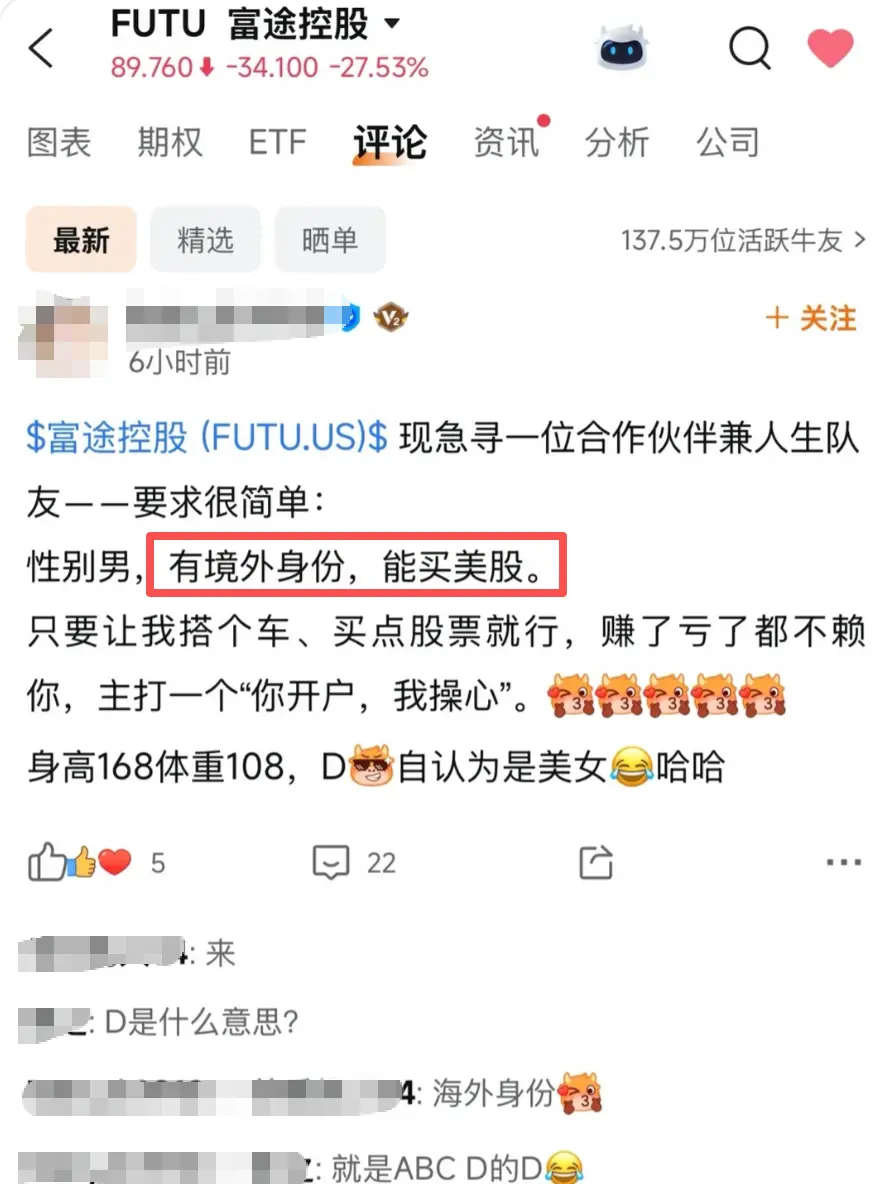

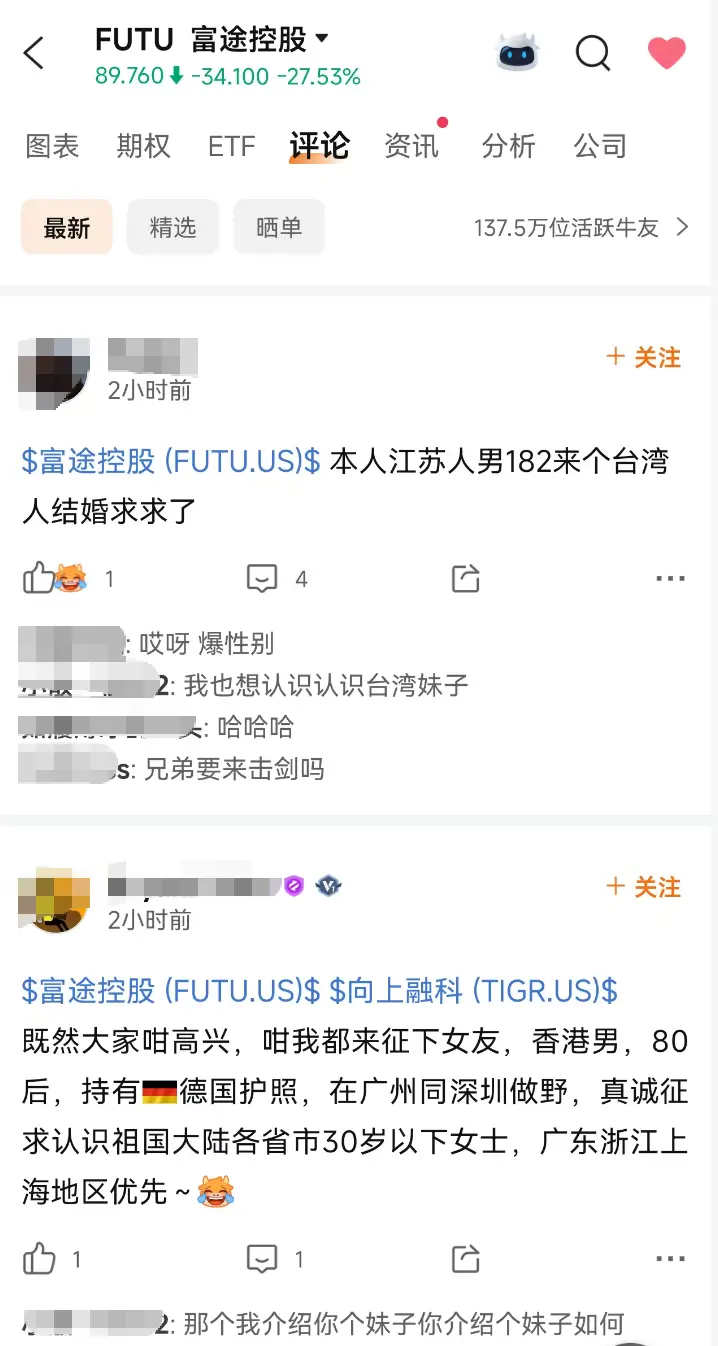

A mainland woman self-identifying as “beautiful” with a D-cup sought overseas male partners; a mainland millennial who’d achieved a 2,046% investment return declared openness to “gender-neutral” identity swaps; a Hong Kong man holding a German passport reverse-sorted potential matches, prioritizing candidates from Guangdong, Zhejiang, and Shanghai…

This is no mere joke. What you’re seeing is an emergent, implicit, securities-like marriage market forming in real time within Futu’s community. Demand-side participants, supply-side participants, pricing preferences, geographic filters—all spontaneously coalescing. It’s the most candid natural-language leak yet of the mindset of China’s middle-class investor cohort in 2026.

Regulatory Hammer Blow

On May 22, eight Chinese government departments—including the CSRC—jointly issued the Implementation Plan for Comprehensive Rectification of Illegal Cross-Border Securities, Futures, and Fund Activities. On the same day, regulators announced proposed punitive measures against the three overseas brokers: Futu Holdings faces a fine of approximately RMB 1.85 billion; Tiger Brokers, RMB 411.2 million; and Longbridge is also named. Both Futu and Tiger saw their U.S.-listed shares drop over 30% in pre-market trading.

The brokers’ responses were measured. Futu stated that, as of the end of Q1 2026, mainland Chinese funded accounts accounted for about 13% of its total funded accounts; Tiger noted that assets held by mainland Chinese clients represented roughly 10% of its group-wide global assets. Both emphasized that “all business operations outside mainland China remain normal.”

But for mainland users already holding U.S. equities in their Futu or Tiger accounts, only one sentence truly stung:

Sell-only, no new purchases.

This means that, for the foreseeable future, if you wish to open a new U.S. stock account to buy NVIDIA, Tesla, or an S&P 500 ETF, you must first possess documentation proving non-mainland-Chinese residency.

Looking back over the past three years, overseas brokers have incrementally raised account-opening thresholds for mainland users:

- End of 2022: CSRC first publicly named these firms;

- May 2023: Their apps were removed from mainland Chinese app stores;

- Starting 2024: Only mainland residents “actually working or residing overseas” were accepted—requiring overseas utility bills, credit card statements, tax returns, etc.;

- September 2025: Threshold raised to require “proof of permanent overseas residency”;

- End of 2025: Only “non-mainland-Chinese identity documents” accepted;

- May 2026: Direct penalties imposed on the broker entities themselves.

The account-opening bar has risen—from a simple utility bill to an overseas passport or permanent residency card. This curve reflects, on its flip side, the repeated re-pricing of “identity” within the investment market.

Overseas Identity: The New Hard Currency for China’s Middle Class

For China’s domestic middle class in 2026, overseas identity has become an implicit asset class. Unlike real estate, it cannot be bought or sold; unlike stocks, it has no public quotation. Yet it possesses all the fundamental attributes of “hard currency.”

First, scarcity. In 2024, around 140,000 individuals were approved under Hong Kong’s Talent Admission Scheme—most from mainland China. That sounds like a large number, but relative to a population base of 1.4 billion, the penetration rate is less than 0.01%.

Unlike property, overseas identity does not depreciate due to population outflows, policy adjustments, or rising interest rates. At any given moment, it confers a fixed set of clearly defined rights—and delivers an exceptionally high return. It unlocks not a single stock, but an entire dimension of asset allocation: U.S. equities, overseas real estate, offshore insurance, foreign-currency deposits, and compliant access channels to crypto assets.

Most enticingly, it is non-transferable. This asset—identity—cannot be arbitraged on secondary markets like stocks. It can only be held personally—or transferred via three ancient mechanisms: marriage, childbirth, or inheritance.

Once, school-district housing spawned a full-blown gray-market ecosystem: agents, title-transfer companies, household-registration “affiliation,” sham marriages, sham divorces. Today, the overseas-identity industry is replicating it all: Hong Kong’s Quality Migrant Admission Scheme (QMAS) agencies, Portugal’s Golden Visa, Singapore’s Employment Pass (EP), Malta’s citizenship-by-investment program, and fast-track naturalization in Caribbean nations. Each product comes with a clear price list and processing timeline.

The physical form of assets has shifted—from “property deeds” to “residency cards,” and from “academic degrees” to “account-opening eligibility.”

Over the past two decades, China’s middle class used school-district housing to lock in social class; over the next decade, they’ll use overseas identity to lock in assets.

Does Studying Abroad Equal Buying Insurance?

Zooming out further, the logic behind China’s middle class purchasing overseas resources has undergone three successive redefinitions over the past twenty years.

From 2000 to 2010: Betting on overseas growth potential. Sending children abroad for education or relocating the whole family reflected an offensive strategic judgment—that opportunities overseas were greater. This was an investment, aimed at returns.

From 2010 to 2020: Geographic diversification. As domestic wealth rapidly accumulated, overseas real estate, insurance, and education entered families’ geographic risk-diversification frameworks. This was defensive—aimed at risk control.

From 2020 to today: “Buying insurance.” Overseas identity is no longer merely part of portfolio diversification—it has itself become the entry ticket. Even if it generates no direct returns, lacking it disqualifies you entirely from certain investment markets. It functions as a premium paid to hedge uncertainty—and its price rises as uncertainty intensifies.

The regulatory hammer blow on May 22 marks another sharp inflection point along this “insurance-price curve.”

When a generation realizes it has missed the window to obtain overseas identity, it transfers hope to the next. What will truly rise in price next may not be QMAS agencies—but international school placements, overseas university foundation programs, and services for low-age study-abroad parental accompaniment. “Identity insurance” cascades down through family generations.

I don’t know which path the millennial with the 2,046% return ultimately chose.

In just one year, he proved himself among the top 1% of the top 1% in U.S. equities and crypto markets—a track record that should shine as the highlight of a professional resume.

But after May 22, it became an attachment to a dating profile.

A performance curve that makes fund managers green with envy—ends up being used this way.

This is 2026.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News