$1.3 Billion Raised in Seven Weeks, Yet SpaceX’s Weight Halved: The Dilution Trap of NASA ETFs

TechFlow Selected TechFlow Selected

$1.3 Billion Raised in Seven Weeks, Yet SpaceX’s Weight Halved: The Dilution Trap of NASA ETFs

Everyone rushing into NASA wants to buy SpaceX—but what they actually end up purchasing from SpaceX is dwindling.

Author: TechFlow

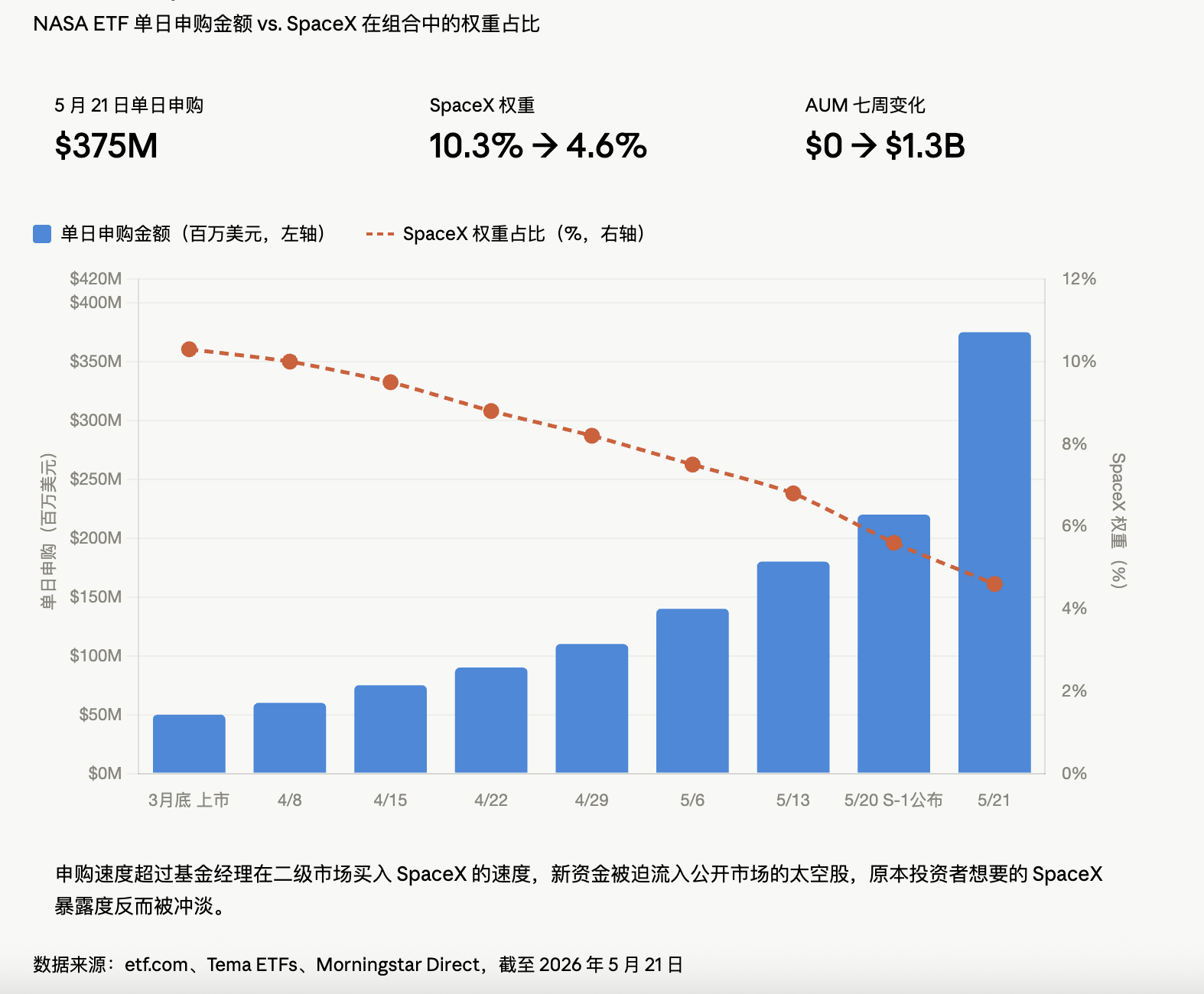

On May 20, the U.S. Securities and Exchange Commission (SEC) website published SpaceX’s S-1 registration statement. The next day, a fund with the ticker “NASA” raised $375 million in a single day, and its assets under management (AUM) tripled within a week. Just seven weeks earlier, this fund had launched.

Seven weeks later, it has become the world’s largest space-themed ETF—leaving behind UFO, a veteran fund that has been around for seven years. In those seven weeks alone, NASA raised more money than UFO has raised over its entire seven-year history.

Everyone rushing into NASA wants to buy SpaceX—but what they actually end up buying of SpaceX keeps shrinking.

Where Did the Money Go?

NASA ETF markets itself as “the only pure-space ETF in the market holding SpaceX.” As of May 21, NASA indirectly holds the economic equivalent of 232,000 shares of SpaceX common stock through a special-purpose vehicle (SPV), with a book value of $147.4 million—implying a valuation of approximately $1.51 trillion for SpaceX.

The numbers look solid—at first glance. But there’s a detail most retail investors won’t notice: According to ETF.com, just one week earlier, NASA’s allocation to SpaceX stood at 10.3%. A week later, it had been diluted to 4.6%.

The inflow of new capital arrived too quickly for portfolio managers to acquire additional SpaceX shares on the secondary market. As a result, large amounts of newly raised cash were instead deployed into publicly traded space stocks—diluting investors’ actual exposure to SpaceX, the very asset they sought.

Individual investors rush in hoping to buy SpaceX—but end up with Rocket Lab, AST SpaceMobile, and a host of other names instead.

Even more subtly, the SPV’s valuation mechanism is static. Its holdings are updated only when Tema—the SPV’s operator—conducts trades. In other words, regardless of how SpaceX’s secondary-market price fluctuates, the book value of NASA’s SPV stake remains unchanged.

This design goes unnoticed in bull markets. But if SpaceX’s IPO opens below its offering price, the SPV’s valuation will react with an almost eerie delay. Worse still, this SPV is subject to a six-month lock-up following SpaceX’s official IPO. If the stock crashes at open, retail investors can flee—but the SPV cannot.

NASA charges an annual management fee of 0.87%, yet 65% of its actual one-year return stems from already-overheated names like Rocket Lab and Intuitive Machines. SpaceX? Has contributed little, if anything.

NASA, in essence, is now a thematic fund using SpaceX as bait—and filled with small-cap space stocks. The bait’s aroma matters, but the dish served up contains entirely different fish.

Valuation Inversion

Many don’t realize that several key names in this sector have already undergone a full rally.

Rocket Lab surged 357% over the past 12 months; Planet Labs soared 979%; LUNR rose 212%. ARKX gained 62% over the same period; ROKT climbed 75%. SpaceX merely ignited dry tinder that was already smoldering.

Lay these figures bare, and the problem emerges. Planet Labs rose 979% in a year—but its core business is selling satellite imagery data. Does its fundamentals justify nearly a tenfold increase in share price?

Global orbital launches totaled 102 in 2019, rising to 342 in 2025—twice the peak of the 1967 space race. Grand View Research forecasts the global aerospace industry will grow from $466 billion in 2024 to $769 billion by 2030.

But here’s the question: Why should an industry expanding from $466 billion to $769 billion translate into a 10x surge in public-market valuations?

This is the classic script of valuation inversion: fundamentals grow linearly, while stock prices rise exponentially—the gap bridged solely by “narrative premium.” And that narrative premium hinges on one thing: SpaceX’s imminent IPO.

So what, exactly, are the real buyers acquiring?

Let’s return to SpaceX itself.

In 2024, SpaceX reported $18.67 billion in revenue—up from $10.3 billion in 2023. Yet its net loss ballooned to $4.59 billion, reversing a $791 million profit in 2023.

According to CNN, the company lost nearly $5 billion last year, largely due to heavy spending by its AI division on building data centers.

In its S-1 filing, SpaceX disclosed that xAI has been merged into SpaceX—and X (formerly Twitter) is included as well. This so-called “space IPO” is, in effect, a mega-packaging of all of Elon Musk’s major assets. The filing also reveals Musk controls 85% of voting power—meaning no one can remove him unless he votes to oust himself.

A $1.75 trillion valuation for SpaceX reflects a four-in-one narrative: “space + AI + satellite internet + social media.” The broader the narrative, the more detached the price becomes from reality.

Yet the secondary market doesn’t care. What the secondary market cares about is that everyone else is rushing to get on board—so it must join, too.

After circling back, who’s really profiting the most? Not SpaceX’s retail shareholders—they haven’t even boarded yet. Nor the ETF investors flooding into NASA—because their actual SpaceX exposure continues to shrink.

The biggest winners are the ETF issuers. NASA charges a 0.87% fee—the third-highest among comparable funds. With $1.3 billion in AUM, that translates to $11 million in annual management fee revenue.

Launching an ETF is fundamentally no different from launching a token: you need a story, perfect timing, and a seemingly credible benchmark. SpaceX delivered all three.

Before the IPO

SpaceX is scheduled to list on the Nasdaq on June 12 under the ticker SPCX. A consortium of the world’s largest investment banks is leading the offering, targeting $40–80 billion in proceeds—far surpassing Saudi Aramco’s record-setting 2020 IPO.

This will be the largest IPO in human history.

If the stock opens below its offering price, all ETF investors who bought in on the SpaceX narrative will find themselves holding SPV positions still marked at “stale” valuations from months ago—unable to cut losses or exit immediately.

If the stock surges at open, those who missed the initial ETF wave will rush in, pushing the ETF’s premium higher—and further diluting SpaceX’s weight inside the fund. This creates a comical reverse flywheel: the more people buy in, the less SpaceX exposure each buyer actually gets.

After SpaceX, a lineup of industry giants awaits IPO. Each “flagship concept-stock” listing will spawn a fresh wave of ETFs—and each new ETF will replicate the same dilution game.

The industry isn’t short of new stories. What’s scarce are those willing to ask: “Did I actually buy what I thought I was buying?” An answer may emerge after June 12—but by then, those who rushed into NASA today won’t care. They’ll either be counting profits—or filing complaints.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News