From Frantic Buying to Frantic Fleeing in Two Months, Energy Funds Bleed $3.2 Billion in a Single Week

TechFlow Selected TechFlow Selected

From Frantic Buying to Frantic Fleeing in Two Months, Energy Funds Bleed $3.2 Billion in a Single Week

Is bottom fishing now catching a falling knife?

Author: Claude, TechFlow

TechFlow Editor's Note: Citing EPFR data, BofA reported that for the week ended July 1, global energy funds saw a net outflow of $3.2 billion, marking the largest single-week withdrawal since July 2024 and the second largest in at least a decade. The four-week mean flipped from a record net inflow of $2.5 billion two months ago to a record net outflow of $1.8 billion. The ceasefire agreement brought Brent back to near $72, and Exxon Mobil fell 23% from its highs. The unwind of the war trade is now a fact; the bet for those entering now is whether the ceasefire will break.

Money that rushed into the energy sector during the Iran war is now withdrawing at a record pace.

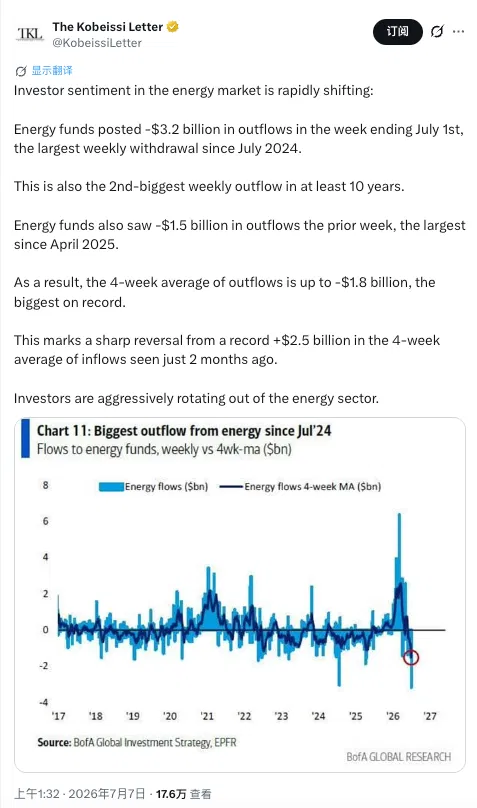

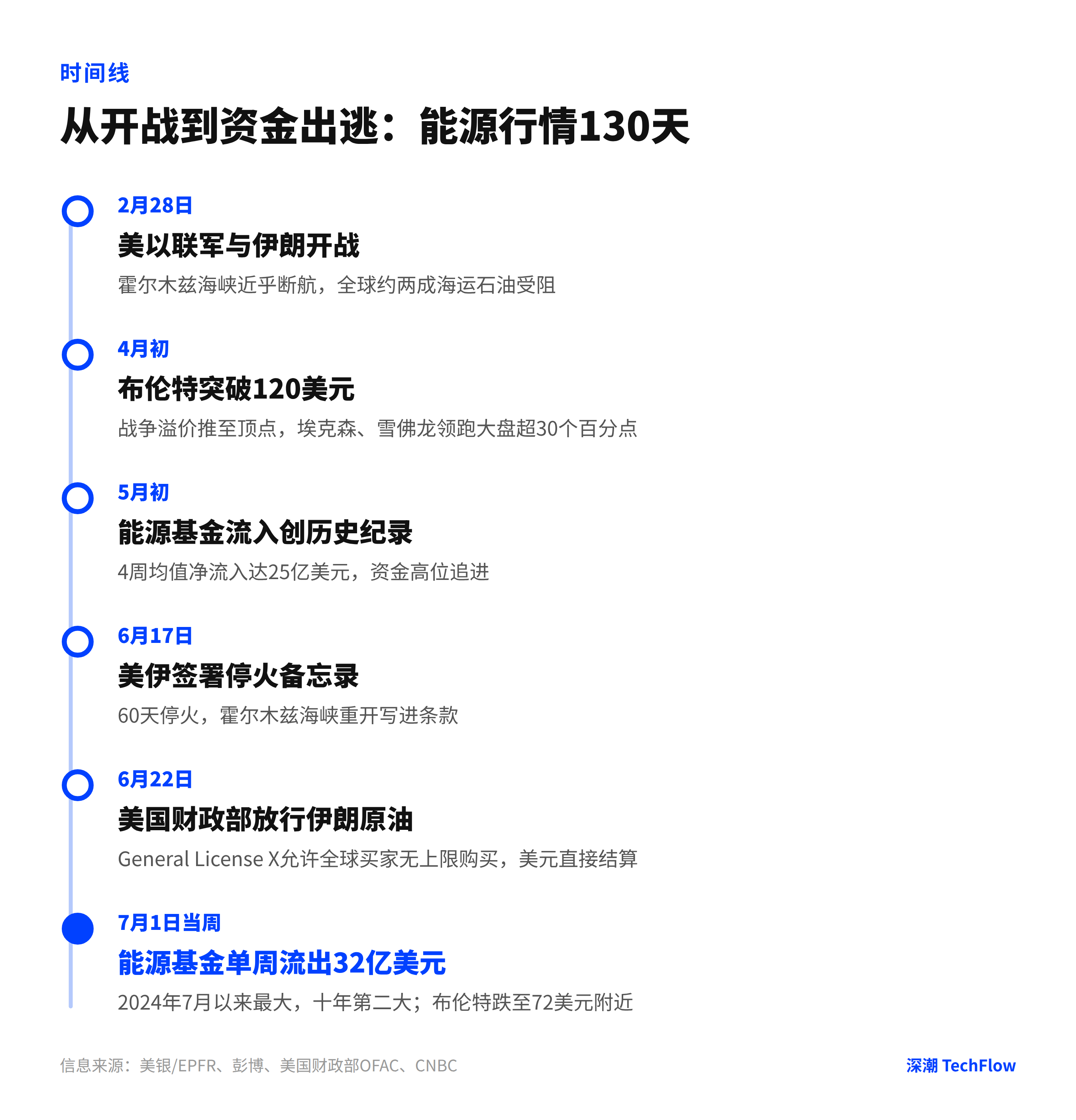

According to EPFR data cited by BofA Global Research, for the week ended July 1, global energy funds saw a net outflow of $3.2 billion, marking the largest single-week withdrawal scale since July 2024 and the second largest in at least a decade. The previous week already saw an outflow of $1.5 billion. The four-week moving average dropped to negative $1.8 billion, the lowest on record. Just two months ago, this mean was positive $2.5 billion, also a historical record. Market tracking account The Kobeissi Letter posted on July 7 that investors are "aggressively exiting the energy sector."

It took only two months to flip from record inflows to record outflows; the turning point was the ceasefire agreement in mid-June.

Energy Leads Declines, but the Entire Fund Flow Statement Shows Risk Off

Looking at energy alone underestimates the information in this statement. In the same week, US equity funds saw a net outflow of $17.2 billion, the largest since March 2026; materials funds outflowed $6.8 billion, also the highest since March; gold funds bled for the seventh consecutive week, creating the longest consecutive withdrawal record since March 2024; crypto funds outflowed $2 billion, the largest single-week withdrawal since November 2025.

Where did the money go? Investment-grade bond funds absorbed $17.2 billion in a single week, high-yield bonds saw inflows of $3.4 billion hitting a new high in over a year, money market funds took in $55 billion, and bond funds have seen net inflows for 62 consecutive weeks.

The assembled picture is comprehensive risk-off; energy is just the hardest-hit segment. Part of the selling pressure on energy funds comes from collateral selling due to overall risk reduction; if risk appetite warms up, this portion of money may flow back. Whether the funds betting on oil prices return depends on the supply landscape.

Ceasefire Brings Oil Prices Back to Reality, Saudi Arabia Still Cutting Prices to Grab Share

On February 28, the US-Israel coalition went to war with Iran, the Strait of Hormuz was nearly blocked, and Brent once broke through $120. On June 17, the US and Iran signed a ceasefire memorandum, with the reopening of the strait written into the terms. On June 22, the US Treasury issued "General License X," allowing global buyers to purchase Iranian crude oil without limits within 60 days and settle directly in US dollars. The two pillars of the war premium, supply disruption and sanctions, were removed one after another within two weeks.

Bad news from the supply side has not stopped. According to Bloomberg data, Persian Gulf crude exports have recovered to 75% of pre-war levels, and Saudi Arabia's Ras Tanura port has resumed loading. OPEC+ approved a production increase of 188,000 barrels/day for next month, continuing to lift production cut restrictions. Saudi Aramco slashed the official selling price of Arab Light crude for Asia in August by $11 directly, to a discount of $1.50 relative to the regional benchmark; the last two times discounts appeared were during the price wars of 2015 and 2020.

As of July 7, Brent hovered in the $72 to $73 range, approaching the lowest since late February, down about 40% from wartime highs. Citi has lowered its Q3 Brent forecast to $75 and sees the 2027 average price at $65. For bulls, there are no visible supply-side rebound catalysts in the short term; the only variable is the stability of the ceasefire itself.

Exxon Falls 23%, War Premium Evaporates Completely Within Two Weeks

The collapse in oil prices hit energy stocks directly. Exxon Mobil fell from a high of $176.41 to below $140, a drop of over 23%; Chevron retreated about 21% from a high of $214.71. In Q1, these two stocks still led the broader market by over 30 percentage points, but now most of the gains have been given back. The energy ETF leader XLE peaked on May 19 and gave back 12% within a month.

More trouble lies ahead. The Q2 earnings starting at the end of July face oil price assumptions completely different from two months ago. In Q1, Exxon swallowed about $4.6 billion combined due to derivative timing losses and Middle East physical asset losses; Chevron also had similar items of about $2.9 billion. If oil prices stay at current levels, some hedging losses will reverse, but the revenue side must face the reality of just over $70.

For those who haven't left, the main support currently is dividends and buybacks. Exxon's quarterly dividend is $1.03 and it plans to buy back $20 billion within the year; Chevron's quarterly dividend is $1.78 and it is pushing $3 to $4 billion in cost cuts. These can buffer the decline but cannot support valuations at war premium levels.

Investment Banks Still Talk $90, Opponents Say Selling Hit the Wrong Target

Institutional forecasts show clear stratification. Morgan Stanley set its Q3 Brent forecast at $90 and Q4 at $80, while maintaining overweight ratings on Exxon and Chevron. Goldman Sachs cut its Q4 forecast from $90 to $80 and sees the 2027 average price at $75. EIA expects Q3 to fall below $80 and year-end around $70. Citi is the most pessimistic. The consensus among 33 analysts surveyed by Reuters in June for the 2026 Brent average price was $90.44, implying oil prices in the second half should be higher than current prices, directly conflicting with the direction of fund flows.

Another camp believes this round of selling hit the wrong target. A 24/7 Wall St column pointed out that investors pressed the sell button on the entire energy sector, but AI data centers are creating the strongest structural power demand growth in decades; utilities, nuclear power, and distributed power companies were wrongly sold off alongside oil stocks, and opportunities may lie precisely in these collateral damage targets.

Risks are also plain to see. On July 7, a Qatari LNG carrier was hit in waters near Oman, and Brent rebounded towards $73 that day. The current ceasefire is only a 60-day memorandum, General License X will expire in late August, and US-Iran negotiations have broken down multiple times within the year.

Shorting energy earns the peace dividend, betting that the ceasefire will not break; those bottom-fishing bet on the opposite. It is recommended to keep a close eye on the next three nodes: Q2 earnings at the end of July, the ceasefire renewal window in mid-August, and the expiration of GL X in late August.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News