USD Private Credit

TechFlow Selected TechFlow Selected

USD Private Credit

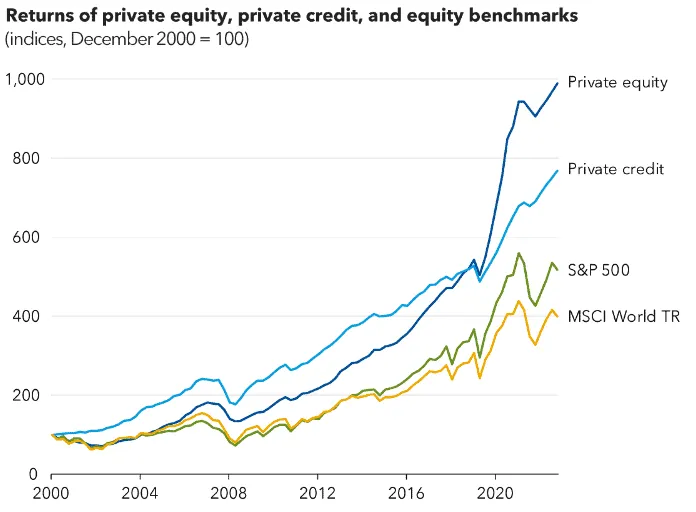

This is a market worth 2 trillion US dollars.

By: Vaidik Mandloi

Compiled by: Block unicorn

In the 1970s, Bruce Bent and Henry Brown created the first money market fund in history. The idea was extremely simple. Due to a regulation from the Great Depression era, the savings interest rate cap for U.S. banks was 4.5%. Although U.S. Treasury yields exceeded 9% at the time, the minimum investment to purchase Treasury bonds was as high as $10,000. Thus, Bent and Brown decided to pool small deposits to purchase Treasury bonds on a large scale and return the yields to investors. Today, the size of money market funds has reached approximately $8 trillion.

Stablecoins have been conducting similar operations, except this time the asset is private credit, a market worth $2 trillion where you need at least $1 million to enter. Yield-bearing stablecoins are used to pool small deposits and channel them into the credit sector.

Today, I will delve into how this happened, and how Goldfinch (the first attempt ever to conduct such operations with real capital) collapsed, resulting in $56 million of depositor funds being trapped in motorcycle loans in Kenya.

How Stablecoins Became the Money Market Funds of Private Credit

In the 1990s, U.S. banks provided about half of the debt capital to businesses and consumers, but today this ratio is about 20%. This is because after 2008, new capital rules took effect, making it too costly for banks to hold leveraged loans. Consequently, banks completely exited the middle-market lending business, and private credit funds took their place.

Apollo, Blackstone, and KKR raised capital from pension funds and insurance companies and began lending to companies abandoned by banks, charging high premiums because these borrowers had no other choice.

The market size has grown from less than $200 billion in 2008 to over $2 trillion today, and almost all of this capital comes from institutional investors writing checks of $5 million or more.

One of the main reasons private credit loans have a million-dollar minimum threshold is the difficulty of management. Every transaction requires due diligence, restructuring, and years of monitoring. Managing a fund with ten institutional Limited Partners (LPs) each contributing $50 million is far easier than managing a fund with retail investors each contributing $500, and even then, scaled investments are often difficult to profit from. Because of this, over the past decade, only pension funds and insurance companies have been able to access these yields, which typically range between 8% and 12%.

It was at this point that yield-bearing stablecoins changed the game, just as Bent and Brown opened access to Treasuries in the 1970s. Although the relevant procedures are still handled by institutions, with funds like Apollo responsible for underwriting and risk management, tokenized sub-funds can now accept deposits of any size and invest them in institutional strategies without needing to manage thousands of individual investors.

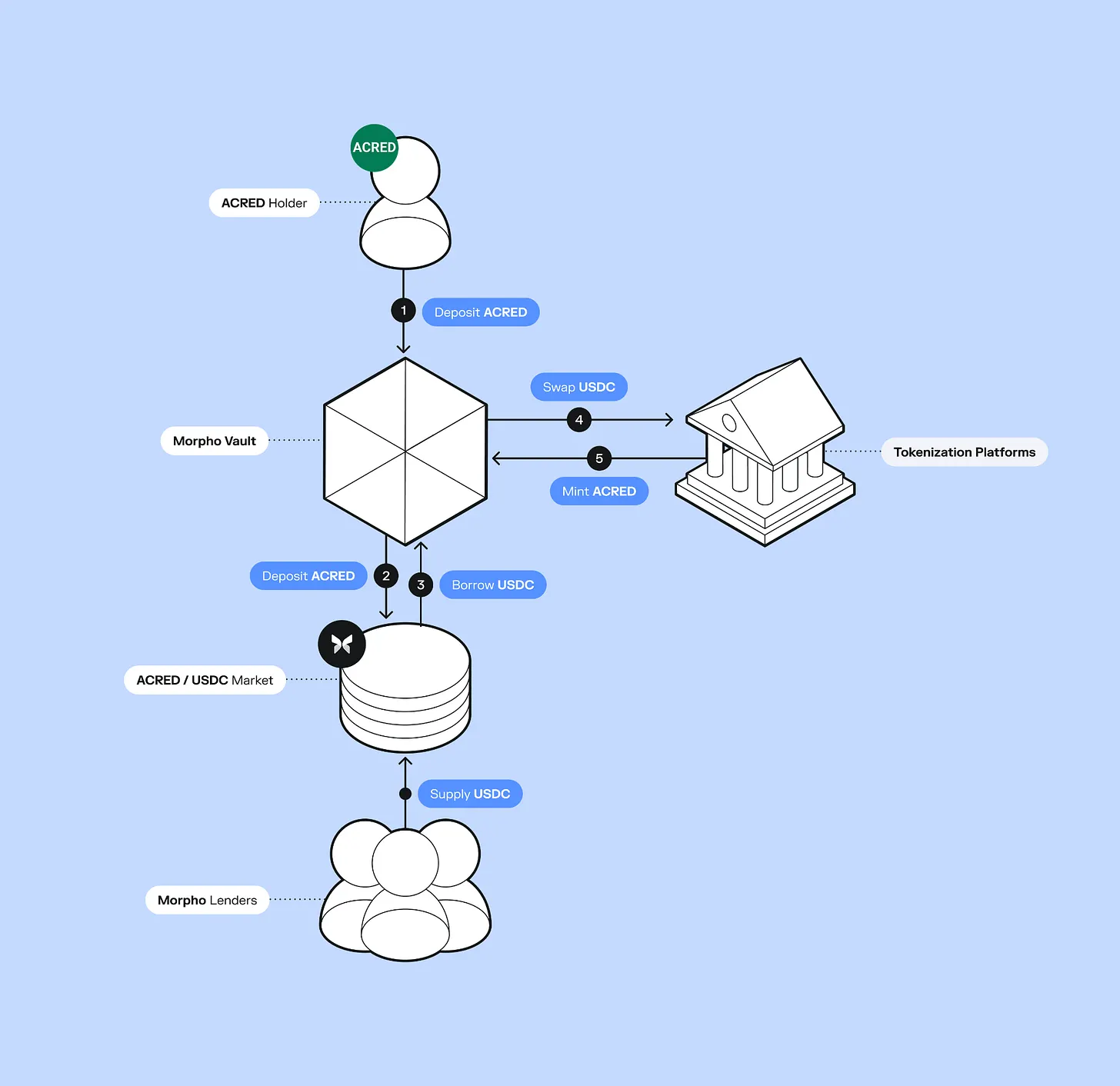

Apollo recently launched the tokenized fund ACRED, and its diversified credit fund has attracted $109 million in inflows. Investors can even deposit it as collateral on the Morpho platform to take out loans and reinvest, thereby achieving leveraged yields.

Figure has built a complete on-chain lending system, issued $2.1 billion in loans, successfully listed on Nasdaq, and launched YLDS—a yield-bearing stablecoin with a circulation of $376 million. Other protocols, such as Pyse and Glow, have gone further, tokenizing solar projects, enabling investors to invest a few hundred dollars to fund solar installations in developing countries and earn an Annual Percentage Yield (APY) from monthly electricity bills.

This does not mean the minimum investment limit for the fund itself has disappeared. The ACRED fund still requires a direct investment of $5 million. However, once the fund is tokenized, its tokens can be traded on the secondary market without minimum investment limits, and it can interact with DeFi (Decentralized Finance) systems in ways traditional fund shares cannot.

In traditional private credit, your capital is locked up for years, with redemption capped at 5% per quarter. But on-chain, capital can be flexibly combined and flows 24/7. For companies like Apollo and Figure, this enables them to access $315 billion in stablecoin capital that is actively seeking yield. By tokenizing capital, they can directly access this capital pool, opening new distribution channels without having to build retail infrastructure from scratch.

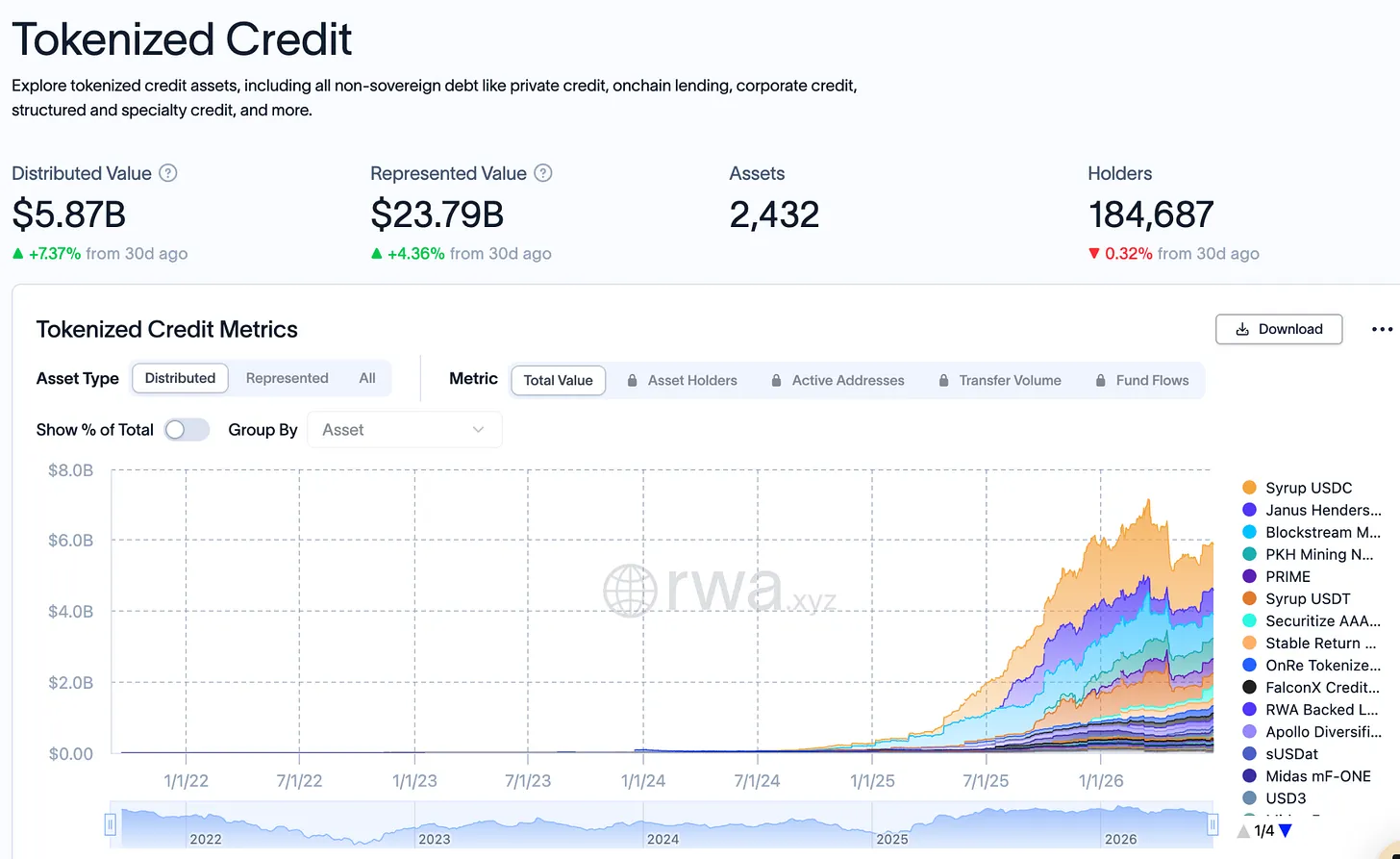

One year ago, total on-chain private credit was only $400 million; today it has reached $5.87 billion, growing 15 times within 12 months, but this still accounts for only 0.30% of the $2 trillion global private credit market. Half of all new stablecoin supply in Q1 2026 came from yield-bearing stablecoins, meaning most new stablecoin capital is now chasing active yield, not just pegging to the U.S. dollar.

Moreover, since every dollar of on-chain credit can be used as collateral and recycled through DeFi protocols, the actual financial activity it generates is multiples of the dollar amount.

Take ACRED as an example. An investor deposits $10,000 on Morpho, borrows $7,000 worth of USDC against this deposit, then uses this USDC to buy more ACRED and deposits it as collateral again. In this way, this deposit can generate over $17,000 in credit risk exposure. In contrast, in traditional private credit: the same $10,000 would sit idle in the fund for 5 years without any yield. But on-chain, this compounding effect occurs simultaneously across multiple layers, which is why the ACRED market's scale grows much faster than its underlying dollar size suggests. But this also means that once the underlying loans default, losses will ripple through every layer of the loop.

Tokenization does not mean potential risks are reduced accordingly. Typically, due to continuous capital inflows, these risks are overlooked because the new capital is sufficient to pay redemption requests. But as capital inflows slow, the gap between token promises and actual loan value begins to emerge. Investors attempt to exit, but liquidity is insufficient, or the token price decouples from its intrinsic value.

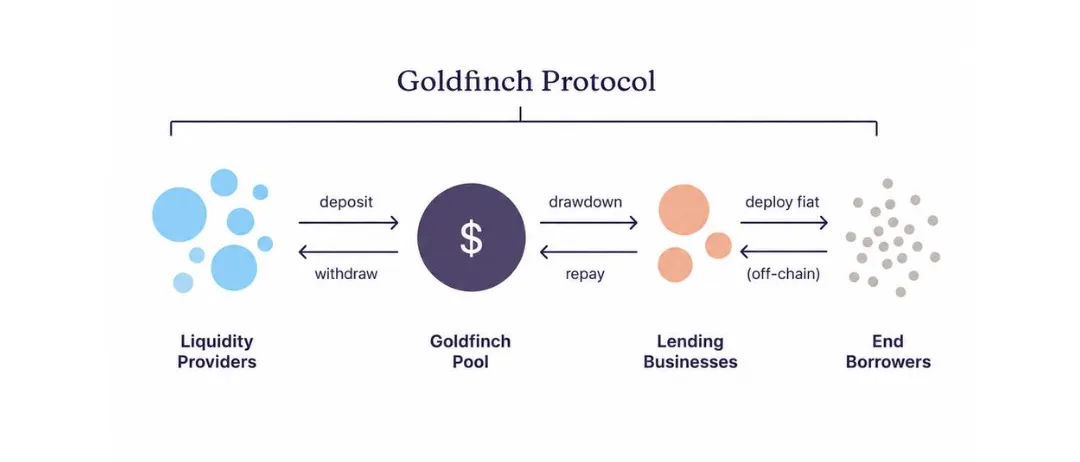

Something similar happened with Goldfinch; it was one of the first protocols launched in 2021 to put private credit on-chain, but recently it had to shut down because $56 million of depositor funds were trapped in Kenya and Nigeria.

Where Did Goldfinch Go Wrong?

Goldfinch raised $25 million from a16z in 2021 to inject crypto capital, which was yielding only 2% to 3% in DeFi lending pools at the time, into businesses across Africa and Southeast Asia. Borrowers of these businesses had to pay loan interest rates of 15% to 25% because local banks were unwilling to serve them.

The concept was to allow anyone holding USDC to deposit into the Goldfinch pool, and then smart contracts would allocate the funds to corresponding borrower accounts within seconds. But underwriting loans for a motorcycle finance company in Nairobi meant someone had to understand Kenya's transport economy and personally verify the borrower's accounts. If repayments stalled, they might even need to visit the borrower's office in person.

But on the blockchain, none of these things are possible. Once USDC is exchanged for Kenyan Shillings and put into the loan book, depositors have no way of knowing how their funds are being used, the borrower's financial status, or even whether loan terms are being fulfilled. All key information related to loan performance has left the blockchain, held in the hands of borrowers in countries most depositors have never visited.

Because of this, it was months before anyone noticed that Tugende Kenya had unauthorizedly transferred $1.9 million of its $5 million credit line to Tugende Uganda in 2022. Nearly 40% of the loans were transferred to another legal entity in another country. Meanwhile, depositors continued to receive what they believed was 10% to 12% interest, completely unaware that the principal supporting their yields had flowed to places never mentioned in the loan agreements.

If a traditional private credit institution discovered such serious defaults, it would recall the loans and force restructuring within days, but Goldfinch depositors learned of this through posts on a corporate governance forum, and their only option was to vote on a proposal that had neither legal authorization to seize assets nor legal authorization to audit remaining assets.

By 2023, Tugende had defaulted completely and vanished entirely. During its lifespan with $113.3 million, Goldfinch issued a total of 24 pools, of which only 13 were eventually fully repaid. The remaining 8 pools had a total of $53.82 million in outstanding loans, and none performed according to the original terms. Most pools are undergoing restructuring, with repayments of less than $51,000 per month per pool, meaning recovering the full $53.82 million at this rate would take 8 to 15 years.

Goldfinch assumed all the risks brought by emerging market currency volatility and limited credit history, yet had almost none of the infrastructure that traditional lending institutions have spent decades building and managing to mitigate these risks. For example, banks lending in Kenya have local offices and regulatory relationships, giving them greater negotiating leverage when transactions go wrong.

But Goldfinch channeled funds from global anonymous wallets to the same type of borrowers without any such support structure, making the information gap between lenders and borrowers larger than in traditional transactions, and leaving depositors with almost no ability to intervene when things broke down.

On-chain fund transfers account for only about 10% of the processes required for lending. The remaining 90% is underwriting and capital recovery, work that is highly localized and costly. Such underwriters need to establish a credibility baseline for the entire asset class, while the asset class itself is still struggling to fight for its right to exist. Every dollar lost in the underwriting process makes it harder for the next institutional partner to come on-chain and reduces the credibility of the entire asset class. The difficulty of credit has nothing to do with on-chain operations, and anyone building in this field without understanding this is no different from creating the next "Goldfinch" (referring to a failed case).

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News