Samsung's profit this year is expected to surpass the cumulative total of the past 40 years, with Q2 potentially setting the highest single-quarter record in tech company history

TechFlow Selected TechFlow Selected

Samsung's profit this year is expected to surpass the cumulative total of the past 40 years, with Q2 potentially setting the highest single-quarter record in tech company history

This round of price hikes driven by AI memory shortages is pushing the pricing power of memory manufacturers to heights unseen in ten years.

Author: Claude, TechFlow

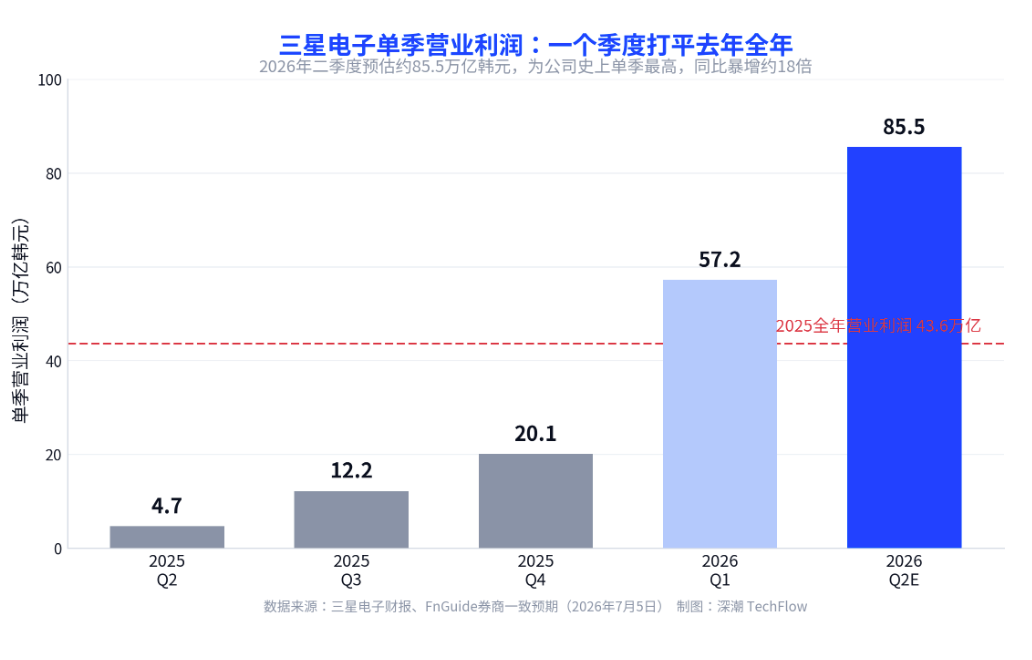

TechFlow Editor's Note: If you hold assets related to memory, AI hardware, or the semiconductor supply chain, Samsung Electronics' Q2 earnings preview on July 7 is worth watching closely. Consensus market expectations estimate its single-quarter operating profit at approximately 85.5 trillion won (about 55.9 billion USD), a surge of about 18 times year-over-year, surpassing Apple and Nvidia for the same period, setting a record for the highest single-quarter profit in the history of global tech companies. DRAM and NAND contract prices jumped 40% to 65% in one quarter, and Samsung is requesting another 20% increase for DRAM in Q3. This round of price hikes driven by AI memory shortages is pushing memory manufacturers' pricing power to heights unseen in a decade.

Samsung Electronics will disclose its 2026 Q2 earnings preview on July 7, and this preview is highly likely to break a record.

According to consensus expectations from brokerages compiled by financial data provider FnGuide, Samsung's Q2 revenue is approximately 169.4 trillion won (about 110.7 billion USD), and operating profit is approximately 85.5 trillion won (about 55.9 billion USD). This profit represents a surge of about 18 times compared to 4.7 trillion won in the same period last year, and a quarter-over-quarter increase of about 49.5% compared to 57.2 trillion won in Q1. It will become the highest single-quarter operating profit record since the company's founding, also surpassing the single-quarter operating profits of Apple and Nvidia for the same period.

Looking at the longer term, Samsung's full-year profit volume this year is even more astonishing. Multiple brokerages predict that full-year operating profit for 2026 will exceed 100 trillion won, more than double the 43.6 trillion won in 2025. Samsung's single-quarter profit of 57.2 trillion won in Q1 itself already exceeded the full year of last year. For investors focusing on semiconductor cycles, the slope of this upward trend is something unseen in the past two memory supercycles.

One Quarter Equals Full Last Year, Profits Almost Entirely from Chips

Samsung's profit structure has fundamentally shifted in this cycle.

Of the 57.2 trillion won operating profit in Q1, the DS division responsible for chip business contributed 53.7 trillion won, accounting for about 94%, a year-over-year increase of about 48 times. The operating profit margin for the chip business exceeded 70%, a level higher than the profit margins of Nvidia and TSMC for the same period. In contrast, profits from the mobile and home appliances businesses shrank by nearly 40% year-over-year, almost negligible.

The driving force comes from AI memory shortages and price hikes. Large tech companies continue to expand AI data centers, drawing a large amount of memory away from consumer markets like mobile phones, PCs, and game consoles, squeezing supply to the limit. Samsung memory business head Kim Jae-jun stated in the Q1 conference call that the company's demand fulfillment rate has dropped to a historic low, and customers worried about supply shortages are even placing orders early to lock in capacity for 2027. Prices jumped accordingly, with Q1 contract DRAM prices rising about 50% quarter-over-quarter.

For holders, one point to note is that this round of price hikes is a double-edged sword for Samsung. Samsung is both the biggest beneficiary of upstream price hikes and one of the biggest victims of downstream cost increases. The same price hike is recorded as profit on the chip division's books and as a loss on the mobile division's books. Samsung's mobile business has issued an internal warning that 2026 may see the first annual loss since the division's establishment, with core component costs accounting for more than 40% of the total device cost.

Behind the Q2 85 Trillion Won Expectation, There Is a Bonus Variable

The consensus expectation of 85.5 trillion won is not the upper limit; the divergence among brokerages mainly lies in the item of employee bonus accrual.

Samsung's labor and management reached an agreement last month to establish a special management performance bonus for the Semiconductor (DS) division, accrued at 10.5% of the division's operating profit, with the accrual scale for the first half estimated between 19 trillion and 25 trillion won. This accrual directly suppressed book profits. Korea Investment & Securities accordingly lowered the operating profit estimate from 95.85 trillion won to 86.05 trillion won, while Shinhan Investment lowered it from 89.86 trillion won to 82.1 trillion won.

Shinhan Investment analyst Kim Hyung-tae pointed out that excluding the impact of bonus accrual, Samsung's actual profitability is estimated to have crossed the 100 trillion won threshold. In other words, the real earning power in Q2 is higher than the book figure of 85 trillion won; the bonus accrual transferred part of the profit to employees. For investors tracking Samsung's fundamentals, when looking at the July 7 preview, it is necessary to distinguish between book profit and operating profit excluding accruals; the two may differ by over ten trillion won.

Price Hikes Continue, Samsung Requests Another 20% Increase for DRAM in Q3

The momentum of memory price hikes has not yet peaked, which determines Samsung's profit elasticity for the next two quarters.

DRAM and NAND flash contract prices jumped 40% to 65% quarter-over-quarter in Q2, and Samsung is already requesting another 20% increase for Q3 DRAM contracts. Consumer electronics manufacturers are resisting this round of price hikes, but supply remains tight, and the initiative remains in the hands of memory manufacturers like Samsung. US Micron has already verified the industry's profit strength first; its operating profit for the fiscal quarter ending in May reached 33.32 billion USD (about 51 trillion won), a year-over-year increase of about 15.4 times.

This shortage is judged by Samsung to continue until 2027 or even longer. As capacity tilts more and more towards AI infrastructure projects, consumer electronics may be the segment most impacted. For those wanting to position on the semiconductor chain, the fact that the price hike cycle has not yet ended is the main support currently, but one must also realize that prices are at historic highs; once the pace of AI data center investment slows, the risk of pullback from high prices is also significant.

Divergence Between Stock Price and Profit, What Is the Market Worried About

Profits are at a record high, yet the stock price is falling; this divergence itself is the signal that needs to be understood most currently.

Although Q2 profit expectations far exceed Apple and Nvidia, Samsung's stock price has moved in the opposite direction over the past week. As of last Friday's close at 309,500 won, it fell 4.18% within a week, dropping about 17.36% from the 52-week high of 374,500 won set on June 19. In early July, weakening US semiconductor indicators triggered a global sell-off, and the KOSPI once fell nearly 8% in a single day, dragging Samsung and SK Hynix into a deep correction.

There are two catalysts supporting a stock price rebound. One is reports that AI company Anthropic is negotiating custom hardware with Samsung, adding a new narrative beyond memory for Samsung's chip manufacturing capabilities. The second is that the momentum of price hikes in the memory market continues. The market's current hesitation stems more from concerns about the cycle peaking; investors are watching to see if this record-breaking performance can dispel peak anxiety and become a turning point for sentiment repair. SK Hynix's American Depositary Receipt (ADR) will list on NASDAQ on July 10, with an issuance scale of about 45.5 trillion won, another key event this week that will also affect the sentiment of the entire sector.

For readers holding semiconductor assets, the two dates of the 7th and 10th are worth watching. If Samsung's actual performance can confirm that profits are still climbing and the Q3 guidance given is not weak, the current stock price correction is more likely a mid-cycle adjustment rather than a top signal; conversely, if the good news is fully priced in after performance realization and the stock price continues to weaken, then be alert that the market has already started pricing in a peak for this round of memory supercycle.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News