Bitget UEX Daily Report | Fed’s Third-in-Command Signals Policy Stability; SanDisk and Micron Lead AI Sector Gains Amid U.S. Equity Market Divergence; PCE Inflation Misses Expectations, Elevating Policy Uncertainty

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Fed’s Third-in-Command Signals Policy Stability; SanDisk and Micron Lead AI Sector Gains Amid U.S. Equity Market Divergence; PCE Inflation Misses Expectations, Elevating Policy Uncertainty

Overall, the market is transitioning from the “loose policy expectations” phase to the “data-driven verification” phase, and structural divergence will be the dominant theme for the foreseeable future.

I. Top News

Federal Reserve Updates

John Williams, President of the Federal Reserve Bank of New York: Current monetary policy stance is appropriate; inflation significantly above 2% is an indisputable fact.

- Williams stated that tariffs, energy prices, and AI-related investment are the primary drivers of current inflation. He projects inflation to fall to approximately 3.5% by end-2026 and return to the 2% target by 2028; unemployment is expected to decline to 4%.

- He emphasized that the current interest rate level is sufficient to bring inflation back on track toward its target, though significant risks remain and policy must retain flexibility.

- Market impact: Reinforces market expectations of the Fed holding rates higher for longer, dampens near-term rate-cut bets, keeps the U.S. Dollar Index strong, and places moderate pressure on risk assets.

Global Commodities

Ongoing developments involving Iran and the Strait of Hormuz test the U.S.-Iran ceasefire agreement.

- Iran expects to generate ~$40 billion annually from the Strait of Hormuz and has proposed joint toll collection with neighboring countries. Meanwhile, the Islamic Revolutionary Guard Corps (IRGC) attacked a Singapore-flagged cargo vessel near the strait, testing enforcement of the ceasefire agreement.

- Background: Earlier Middle East hostilities pushed up energy prices and consequently U.S. inflation; progress on the ceasefire had previously pulled oil prices lower, but this incident highlights the fragility of the agreement.

- Market impact: Oil prices dipped short-term, yet geopolitical uncertainty continues to underpin energy markets. Gold and other safe-haven assets faced short-term pressure due to a stronger dollar.

Macroeconomic Policy

U.S. May PCE Price Index rose YoY to 4.1%, the first time exceeding 4% since April 2023.

- Key drivers include energy price hikes stemming from Middle East conflict and the initial impact of Trump-era tariff policies. Q1 GDP final reading was revised upward to 2.1%, yet downward revisions to private domestic final purchases indicate relatively weak consumption momentum.

- Institutions forecast U.S. year-end unemployment may rise to 4.7%, with hiring becoming more cautious.

- Market impact: Sticky inflation exceeding expectations—combined with Fed officials’ commentary—has further narrowed market expectations for the number of rate cuts this year. The dollar and U.S. Treasury yields gained support.

II. Market Recap

Commodities & FX Performance

- Spot Gold: $4,021/oz, -0.14%

- Spot Silver: $57.40/oz, -0.72%

- WTI Crude: $71.70/bbl, -0.33%

- Brent Crude: $75.20/bbl, -0.4%

- U.S. Dollar Index (DXY): 101.51, -0.02%

Driver Analysis: The DXY remains near its strong level of 101.5, driven by Fed officials’ “higher-for-longer” messaging and persistent U.S. inflation data. Gold and silver retreated amid a stronger dollar and fluctuating risk sentiment, although ongoing Middle East geopolitical uncertainty still provides some safe-haven support. Oil prices edged lower amid mixed signals from U.S.-Iran ceasefire progress and the Strait of Hormuz incident, as market expectations for supply restoration rise—but the fragility of the agreement caps downside potential. In the near term, dollar movement and the Fed’s policy path remain the core variables for precious metals and energy prices. Institutions broadly believe that if inflation data continues to exceed expectations, precious metals may remain range-bound, while oil prices will hinge on actual geopolitical developments and OPEC+ dynamics.

Cryptocurrency Performance

- BTC: $59,595, -2%

- ETH: $1,565, +3.25%

- Total Crypto Market Cap: $2.14 trillion, -1.4%

- 24H Liquidations: ~$887 million total, ~$691 million long liquidations

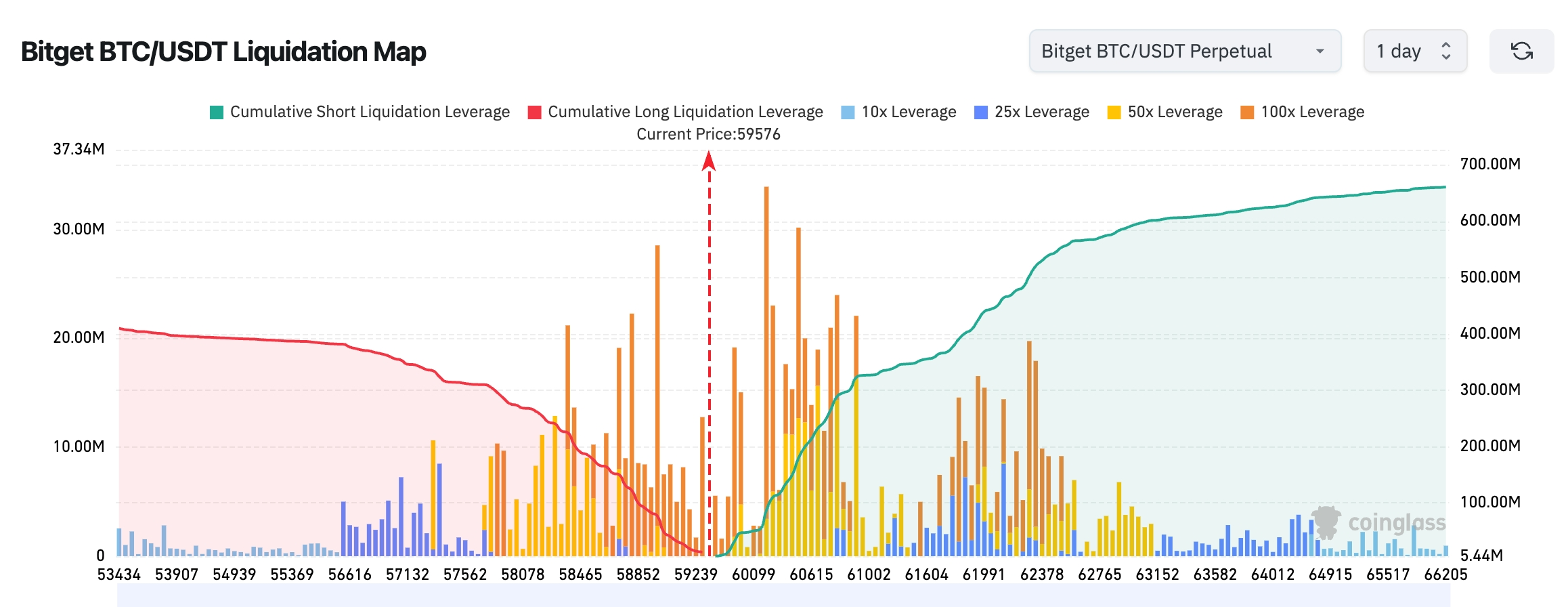

- Bitget BTC/USDT Liquidation Map: Current BTC price ~$59,576. A dense cluster of long liquidation levels lies between $58,500–$59,300; a break below key support could trigger cascading long stop-outs and accelerate downside. Cumulative short liquidation volume is notably larger in the $60,000–$62,500 range, indicating overall liquidity favors upward price attraction—but near-term focus remains on defending the $59,000 level to avoid short-dominated price action.

- Spot ETF Net Flows: BTC spot ETFs saw net outflows of $414 million yesterday and $469 million the day before, totaling $997 million in net outflows over three consecutive days.

Driver Analysis: Bitcoin broke below the $60,000 threshold and hit a recent low, primarily driven by the U.S. May PCE inflation print exceeding expectations. Markets fear the Fed may maintain higher rates for longer, weighing on risk assets broadly. Leveraged markets experienced a pronounced wave of long liquidations, with 24-hour liquidation value approaching $900 million. ETF fund flows continued their outflow trend, reflecting institutional caution amid high volatility. ETH’s relative weakness versus BTC reflects divergence. Technically, BTC’s near-term focus centers on the validity of $58,000 as support—if breached, further downside toward lower levels becomes likely; upside requires a decisive break above $62,000 to open room for recovery. Overall, macro uncertainty dominates short-term direction. Institutional views lean toward viewing the current correction as a normal pullback following elevated valuations, though heightened geopolitical and policy risks warrant close monitoring.

U.S. Equity Index Performance

- Dow Jones Industrial Average: 51,920.62 (+0.14%)

- S&P 500: 7,357.49 (-0.01%)

- Nasdaq Composite: 25,358.60 (-0.46%)

Tech Giants Update

- NVDA: $200, -1.9%

- AAPL: $275, -6.1%

- MSFT: $357, -3.5%

- GOOGL: $344, -0.5%

- AMZN: $228, -3.0%

- META: $557, -4.5%

- TSLA: $376, -6.1%

- MU: $1,214, +15.7%

- SPCX: $150, +1.3%

Performance Summary & Driver Analysis: U.S. equities displayed pronounced sectoral divergence. Memory and chip stocks tied to AI infrastructure surged sharply (Micron, SanDisk, etc., up >15%), reflecting optimism about the sustainability of AI capital expenditures. In contrast, consumer-facing tech giants such as Apple, Microsoft, and Amazon were sold off amid product price hikes—Apple’s single-day drop of over 6% marked its largest since April 2025. Drivers diverged markedly: memory stocks benefited from robust demand for HBM and storage chips from AI data centers; large-cap tech firms raised prices due to rapidly rising memory chip costs, triggering concerns over demand elasticity and margin compression. Overall, the trend confirms AI themes remain active, yet highly valued consumer tech stocks face cost-pass-through pressures. Institutions view this divergence as likely to persist, with capital favoring AI supply-chain names offering clearer earnings visibility.

Crypto Market Stock Derivatives Overview

- 24H Total Turnover: $20.199B (-4.77%)

- Total Open Interest: $5.571B (+1.78%)

- 24H Total Liquidations: $30.9486M

- Turnover Share: 8.85%

- Open Interest Share: 5.37%

- Liquidation Share: 3.48%

Sectoral Open Interest Breakdown

- Biotech: $17.73M

- Consumer: $79.91M

- Industrial: $26.06M

- Financials: $153M

- Technology: $2.893B

3. Market Heatmap

Largest Positions / Hottest Assets:

- SPCX: $745M

- MU: $571M

- SKHX: $463M

- SNDK: $357M

- NVDA: $233M

Sectoral Momentum Observations

Memory & AI Chip Sector surged >15%, signaling sustained momentum behind AI infrastructure themes—and starkly contrasting with consumer tech stocks.

- Representative names: Micron (MU) +15.74%, SanDisk (WDC-linked) +21%+, Applied Materials (AMAT) +13%+

- Driver Analysis: Micron’s quarterly results vastly exceeded expectations and it raised full-year guidance—driven primarily by explosive demand for High Bandwidth Memory (HBM) in AI training and inference workloads. Current-generation HBM3/HBM3E chips deliver several-fold improvements in capacity and bandwidth over prior generations. NVIDIA’s Blackwell architecture GPUs require 3–8x more HBM than previous-gen GPUs, causing global HBM supply constraints to persist. As one of only a few manufacturers capable of mass-producing and designing HBM, Micron’s order visibility improved significantly and average selling prices (ASPs) rose—directly expanding gross margins and driving earnings upside. Semiconductor equipment makers like Applied Materials benefit from capital spending on advanced packaging, 3D stacking, and memory fab expansions. Storage vendors like Western Digital also rallied on surging demand for high-speed NAND flash from AI data centers. This rally stands in sharp contrast to consumer-facing tech giants (e.g., Apple and Microsoft), whose share prices fell after raising prices due to soaring memory costs—highlighting the market’s differentiated pricing of “high-ROI, non-discretionary AI capex” versus “weaker demand elasticity in consumer electronics.” Even amid May’s PCE inflation rising to 4.1% YoY and Fed official Williams’ “higher-for-longer” signal, AI-related supply chains remain viewed as non-discretionary growth avenues, drawing continuous capital into pure AI-enabling segments. Institutions opine that if hyperscaler capex guidance remains robust (historical data shows high ROI visibility for AI investments), outsized returns for memory and equipment stocks may extend through 2027—but vigilance is warranted should macro data deteriorate or geopolitical risks escalate, potentially slowing broader tech capex. Technically, the sector faces some profit-taking pressure near-term; investors are advised to monitor pullbacks for phased allocation opportunities and Q3 capacity ramp-up data validation.

III. Deep Dive: U.S. Equity Stocks

1. Micron Technology – AI Memory Demand Drives Strong Earnings Beat

Event Summary: Micron Technology reported quarterly results with revenue and earnings substantially surpassing consensus estimates, fueled by robust demand for High Bandwidth Memory (HBM) and DRAM from AI data centers. Management raised full-year guidance, significantly easing market concerns regarding the AI capex cycle. Market Interpretation: Multiple investment banks upgraded Micron’s price targets, citing early-stage AI infrastructure build-out, a clear upward memory cycle, and tight supply supporting pricing power and margins. Some institutions highlight Micron’s industry-leading pace in HBM production ramp-up, positioning it as a core beneficiary of the AI wave. Investment Insight: Memory and storage segments within the AI theme retain portfolio allocation appeal—focus on companies with visible earnings trajectories and proven capacity expansion execution.

2. Apple – Surging Memory Chip Costs Trigger Product Price Hikes, Sparking Concerns

Event Summary: Apple announced price increases across Mac and iPad lines—up to $300—due to “unprecedented” rapid rises in storage and memory chip prices driven by AI data center demand. It also adjusted its chip strategy, skipping certain M-series iterations to prioritize AI-optimized architectures. Market Interpretation: Investors worry such hikes could dampen demand elasticity—especially against an uncertain backdrop for consumer electronics recovery. Views diverge: some see this as a necessary response to cost pressure, ultimately beneficial for margins; others warn premium pricing could accelerate user migration to Android, pressuring near-term stock performance. Investment Insight: Monitor Apple’s AI hardware rollout cadence and post-price-hike demand response; near-term volatility may present tactical buying opportunities on pullbacks.

3. Western Digital – AI Storage Demand Boosts NAND/SSD Market Share

Event Summary: Western Digital (WDC), a leading storage player, rallied sharply alongside Micron’s earnings beat—reflecting broad market recognition of its direct exposure to AI data center expansion. Market Interpretation: Institutions note exponential growth in enterprise NAND and SSD demand from AI training and inference, and view WDC’s market share leadership and product mix as well-positioned to capitalize on data center storage capacity expansion. Cautious supply-side expansion supports pricing power and margin upside. Investment Insight: Track WDC’s quarterly inventory levels and ASP trends as key indicators of AI-driven demand strength; consider WDC as a satellite position complementing core memory holdings.

4. Corning – Accelerating Demand for Data Center Interconnect Materials

Event Summary: Corning (GLW) and other data center materials suppliers benefited from accelerating AI server deployments, lifting demand for fiber optics and glass substrates. Market Interpretation: AI data centers’ need for high-speed interconnects boosted orders for Corning’s fiber solutions. Institutions regard Corning as an indispensable enabler in AI infrastructure build-out, with demand scaling linearly alongside server deployment volumes. Investment Insight: Corning serves as an indirect AI capex beneficiary—track data center capex validation signals closely.

5. BlackBerry – Edge Computing & Security Strategy, Plus NVIDIA Collaboration, Draws AI Market Attention

Event Summary: BlackBerry (BB) garnered additional attention in AI discussions thanks to its longstanding expertise in edge computing and security—particularly as AI deployment shifts from cloud to edge. Its QNX secure operating system and deepening collaboration with NVIDIA further underscore solution applicability. Market Interpretation: AI-powered security platforms like Cylance enable BlackBerry to enter the AI edge device and IoT security space, delivering real-time threat detection and protection for distributed data centers, autonomous vehicles, and industrial IoT devices. Expanded integration of its QNX secure OS with NVIDIA’s IGX Thor platform—spanning robotics, healthcare, and industrial systems—builds a unified, safety-critical edge AI platform aligned with the industry trend of shifting from centralized training to edge inference. Analysts believe that amid tightening data privacy regulations and rising cyberattacks, BlackBerry’s end-to-end security capabilities offer differentiated competitive advantages, positioning it to claim a niche across the AI infrastructure stack. While core business transformation remains challenging, growth potential in the AI security subsegment and NVIDIA partnership gains analyst recognition. Investment Insight: Consider BlackBerry as a complementary holding for AI security and edge computing themes. Key tracking points include progress on NVIDIA collaboration, contract wins in IoT/AI security markets, partner developments, and quarterly revenue contributions. Position it alongside pure AI hardware/storage stocks to diversify thematic risk, while monitoring macro rate environment impacts on valuation recovery.

IV. Project & Market Updates

1. Sharplink, an Ethereum treasury company that hadn’t purchased ETH for eight months, resumed accumulation today—receiving 5,000 ETH ($7.85M) from FalconX six hours ago. It now holds 876,000 ETH ($1.37B), with an average acquisition cost of $3,609, resulting in unrealized losses of $1.789B (-56%).

2. STRC, the perpetual preferred stock issued by Strategy, has seen its 90-day correlation with Bitcoin climb to nearly 0.70—the highest since its July 2025 launch. STRC has declined 23% this month to $76, while BTC fell nearly 20% to below $60,000, moving in tandem.

3. Once renowned for physical-keyboard phones, BlackBerry has quietly evolved into a critical software layer provider for the “physical AI” and robotics ecosystem. Its QNX software framework—dubbed the “never-crash” nervous system for autonomous machines—delivers secure, reliable, deterministic real-time operating systems for smart vehicles and warehouse robots, serving chipmakers including NVIDIA and AMD.

4. In response to a CoinDesk report stating Kraken’s parent Payward is negotiating to acquire a 15% stake in the Aave protocol for $385M—a valuation representing just 30% of AAVE’s fully diluted valuation—Aave founder Stani Kulechov posted on X: “We would never sell AAVE at a 70% discount,” and noted the CoinDesk report was inaccurately phrased.

5. Multicoin Capital released a report asserting that Hyperliquid’s native token HYPE, currently trading around $63, is severely undervalued. Under a base-case scenario, Multicoin forecasts a 2028 HYPE target price of $319, assuming Hyperliquid achieves ~$8B in annual revenue and trades at a 20x P/E multiple. Multicoin disclosed it has been actively accumulating HYPE since February and now holds it as its largest position in its liquid hedge fund.

6. TD Cowen analysts suggested that if SpaceX fails to reach a network-sharing agreement, it may accelerate its wireless ambitions via a T-Mobile acquisition. Strategically, T-Mobile’s existing partnership with Starlink aligns well. While purely speculative, this idea underscores growing competitive pressure SpaceX exerts on the telecom industry.

7. With Bitcoin trading at $59,600 and its 200-day cost-average (C200) at $75,821, the Ahr999 bottom-finding indicator reads ~0.287—deeply undervalued. The yearly low occurred on February 6, 2026, at 0.27. Historical data shows Ahr999 readings below 0.3 are extremely rare, typically appearing only during systemic panic or bear-market bottoms—such as early 2011, the 2018 bear bottom (~0.24 low), the March 2020 COVID flash crash, and the FTX collapse and ETH cascade liquidations in 2022.

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

- Fed Official Speeches: Chicago Fed President Austan Goolsbee and other officials may speak; markets will watch for updated views on inflation and policy trajectory.

Institutional Views:

Synthesizing the past 24 hours’ movements across U.S. equities, precious metals, crude oil, FX, and crypto, mainstream investment banks and strategists adopt a cautiously optimistic stance. Signals from Fed officials—including Williams’ comments on the “appropriateness of the current policy stance” and possible delay of the 2% inflation target to 2028—are interpreted as implying fewer rate cuts than previously anticipated this year, supporting both the dollar and Treasury yields. The unexpectedly high PCE inflation reading (4.1%) reinforces the “higher-for-longer” narrative, yet robust AI capex momentum provides structural support for U.S. equities—evidenced by the outperformance of memory and chip stocks. Precious metals and crypto face near-term pressure from dollar strength and volatile risk sentiment, though institutions broadly view the current pullback as having partially priced in macro uncertainty, preserving long-term allocational appeal. Some strategy reports suggest that if geopolitical tensions ease further and inflation data avoids persistent overshoots, risk assets could stage a cyclical rebound; conversely, further dollar strength could trigger broader knock-on effects. Overall, markets are transitioning from “loose-expectation” mode to “data-dependent verification,” with structural divergence set to dominate the near-term landscape.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute any investment advice. Data herein may contain unavoidable discrepancies; please rely on real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News