Bitget UEX Daily Report | Iran’s Three-Stage Negotiation Path Is Clear; DeepSeek Dramatically Cuts Input Caching Costs; Google, Microsoft, and Others to Release Earnings This Week

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Iran’s Three-Stage Negotiation Path Is Clear; DeepSeek Dramatically Cuts Input Caching Costs; Google, Microsoft, and Others to Release Earnings This Week

Overall, institutions maintain their overweight stance on the technology and AI sectors and recommend paying attention to this week’s earnings reports from tech giants to verify capital expenditure plans.

Author: Bitget

I. Key News Highlights

Federal Reserve Updates

U.S. Department of Justice Ends Criminal Investigation into Federal Reserve Office Renovation

- The U.S. Attorney’s Office for the District of Columbia has formally concluded its criminal investigation into cost overruns on the Federal Reserve’s office renovation project—a project involving billions of dollars in taxpayer funds. The termination of this probe may clear a key hurdle for Kevin Warsh, President Trump’s nominee for the next Fed Chair, ahead of his Senate confirmation.

- The Federal Reserve’s Inspector General will continue its internal review; prosecutors noted that the criminal investigation could be reopened at any time if warranted. This development alleviates governance uncertainty within the Fed and helps stabilize market expectations regarding monetary policy continuity—providing short-term support to both bond markets and risk assets.

Global Commodities

Iran Proposes Three-Stage Negotiation Framework; Middle East Risk Premium Path Becomes Clearer

- Iran has submitted a three-stage negotiation proposal to the U.S. via intermediaries: Stage One calls for an immediate end to hostilities and binding guarantees against future attacks on Iran and Lebanon; Stage Two focuses on managing the Strait of Hormuz; and nuclear discussions are reserved exclusively for Stage Three—no nuclear talks will occur unless Stages One and Two are fully concluded.

- President Trump stated that Iran may call him directly if it wishes to negotiate and expressed confidence that the war would end soon. JPMorgan notes the negotiation path is now clearly defined, shifting macro focus from geopolitical risk premiums toward residual “stagflation” risks. While nonlinear commodity supply risks remain, they have eased temporarily, reducing near-term oil price pressure.

Macroeconomic Policy

DeepSeek Slashes Input Caching Pricing Across Entire Model Suite

- DeepSeek’s official website announced that effective immediately, input cache hit pricing has been reduced to one-tenth of its original launch price. The deepseek-v4-pro model is available at a limited-time 25% discount (valid until May 5, 2026), bringing the cost of cached V4-Pro input down to RMB 0.025 per million tokens.

- Goldman Sachs highlights that V4’s hybrid attention architecture innovation dramatically reduces long-context processing costs. It expects further API price declines once Huawei’s Ascend 950 chips enter mass production. Domestic AI competition is thus expected to shift toward differentiation in programming capabilities and multimodal functionality. This move strengthens China’s AI models’ cost competitiveness, accelerates agent application deployment, and bolsters long-term demand for cloud computing and data center infrastructure.

II. Market Recap

Commodities & FX Performance

- Spot Gold: ~$4,677/oz, down ~0.62% over 24 hours. Price action reflects oil volatility and progress in negotiations; lingering stagflation concerns continue to underpin gold but upward momentum remains paused.

- Spot Silver: ~$75/oz, down ~0.96% over 24 hours, pressured by industrial demand concerns and broad-based precious metals correction.

- WTI Crude Oil: $96.20/bbl, up ~1.91% over 24 hours. Clarified negotiation pathways ease fears of supply disruption, though residual geopolitical risks persist.

- Brent Crude Oil: ~$107/bbl, up ~2% over 24 hours, with Strait of Hormuz management emerging as the focal point of Stage Two.

- U.S. Dollar Index: Gained modestly to 98.61, supported by resolution of the Fed investigation and diplomatic progress, weighing on non-U.S. assets.

Cryptocurrency Performance

- BTC: ~$78,623, up ~1.43% over 24 hours—marking two consecutive days of modest recovery.

- ETH: ~$2,367, up ~2.21% over 24 hours, broadly tracking broader market gains.

- Total Crypto Market Cap: ~$2.7 trillion, up ~1.3% over 24 hours amid improved risk sentiment.

- Liquidations: Total liquidations over 24 hours amounted to ~$153 million, with ~$119 million attributed to short positions.

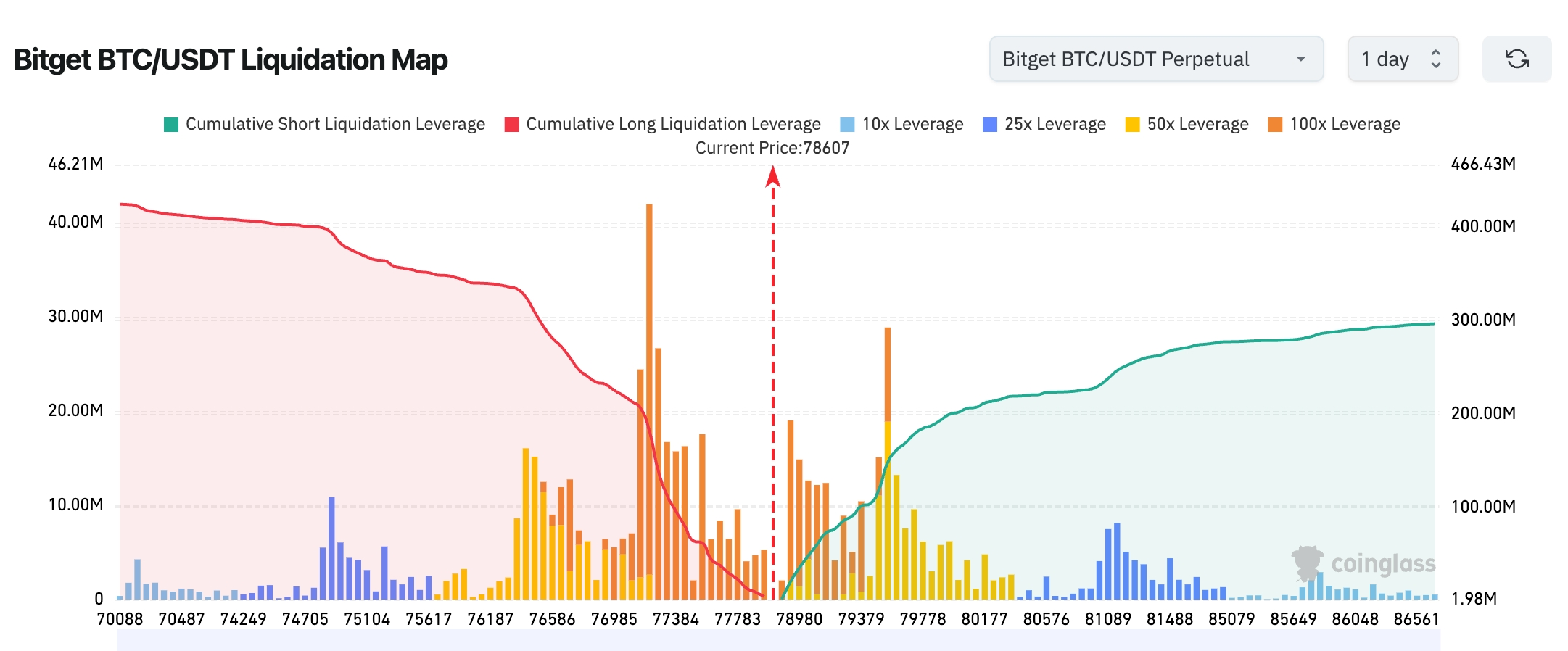

- Bitget BTC/USDT Liquidation Map: Current price sits near $78,600. A breakout above $79,000—where dense short liquidation clusters reside—could trigger cascading short squeezes and propel prices higher. However, significant long leverage remains concentrated between $77,000–$78,000; a pullback into this zone may rapidly trigger long liquidations, resulting in sharp two-way volatility.

U.S. Equity Index Performance

- Dow Jones Industrial Average: 49,230.71 points, down 0.16%, reflecting persistent weakness—energy-sensitive sectors dragged down by oil price fluctuations.

- S&P 500: 7,165.08 points, up 0.80%, hitting a new all-time high, led strongly by tech-weighted stocks.

- Nasdaq Composite: 24,836.60 points, up 1.63%, extending multi-day highs, driven notably by AI and semiconductor stocks.

Tech Giants’ Updates

As of last Friday’s close:

- NVIDIA (NVDA): Up 4.32%, hitting a new all-time high; market cap surpasses $500 billion—AI capital expenditure expectations continue to rise.

- Amazon (AMZN): Up 3.49%, buoyed by robust cloud and AI infrastructure demand.

- Microsoft (MSFT): Up 2.13%, supported by Azure cloud growth and OpenAI collaboration prospects.

- Meta (META): Up 2.41%, accelerated by advertising performance and AI application rollout.

- Google (GOOGL): Up 1.63%, announcing plans to invest up to $40 billion in Anthropic.

- Apple (AAPL): Down 0.87%, with new CEO appointment news insufficient to offset growth concerns.

- Tesla (TSLA): Minimal movement, with rising investor interest in autonomous driving and energy business developments. Most of the “Magnificent Seven” tech giants posted gains, primarily driven by advancing AI capex visibility and easing geopolitical tensions.

Sector Momentum Observations

Semiconductor Sector: Up >3%

- Key Stocks: NVIDIA (NVDA) +4.32%, AMD +14%

- Catalysts: Sustained high expectations for AI compute and data center capex; Intel’s earnings beat and raised Q2 guidance triggered sector-wide confidence. As a critical player in data center CPUs, AMD directly benefits from spillover optimism. Though investor Bill Ackman (Burry) warns semiconductor valuations have entered overbought territory, elevated risk appetite and technically sound bullish chart patterns remain intact. This week’s tech earnings season will serve as a key test of real-world AI spending execution.

China-Listed Tech Stocks (ADR): Up 2.62%

- Key Stocks: Baidu (BIDU) +5%, XPeng (XPEV) +4%

- Catalysts: Iran’s clearly articulated three-stage negotiation framework significantly lowered geopolitical risk premiums, lifting global risk sentiment. Concurrently, DeepSeek’s sharp reduction in AI model input caching costs reinforces China’s AI technology cost competitiveness. Baidu—leader in large language models and search—benefits from accelerating domestic agent application adoption. XPeng demonstrates resilience in intelligent driving technology and overseas expansion. Chinese tech ADRs are experiencing valuation re-rating fueled by synergistic domestic and international tailwinds.

III. In-Depth Stock Analysis

1. NVIDIA (NVDA) – Market Cap Returns to $500 Billion Milestone

Event Summary: On April 24 (last Friday), NVIDIA’s share price rose 4.3% to close at $208.27, pushing its market capitalization above $500 billion once again—reclaiming its position as the world’s most valuable public company. Year-to-date gains exceed 12%. As the core supplier of AI compute, NVIDIA continues benefiting from hyperscalers’ massive capital expenditures. This week, Microsoft, Amazon, Google, and Meta will release quarterly results; their AI infrastructure spending guidance will serve as a critical catalyst for assessing NVIDIA’s medium-term demand. Market Interpretation: Multiple institutions acknowledge NVIDIA’s short-term valuation is elevated and technical indicators signal overbought conditions—but its dominant position in the AI chip market remains unassailable in the near term. Fundamentals are anchored by strong data center demand and steady Blackwell architecture rollout. Analysts have broadly raised full-year revenue forecasts, underscoring NVIDIA’s durable moat in AI training and inference markets. Investment Insight: With the AI capex validation window approaching, investors should look for phased entry opportunities amid earnings-driven volatility—paying close attention to actual capex execution by major cloud providers.

2. Google (GOOGL) – Up to $40 Billion Investment Commitment in Anthropic

Event Summary: Alphabet—the parent company of Google—announced plans to invest up to $40 billion in AI startup Anthropic. An initial $1 billion has already been committed, while the remaining $30 billion will be disbursed in tranches contingent upon Anthropic achieving specific performance milestones. The deal values Anthropic at approximately $35–38 billion and is intended to fund large-scale expansion of its computational infrastructure. Anthropic’s recent launch of Claude Code—an AI programming agent—marks a major breakthrough accelerating its commercialization. Market Interpretation: Institutions broadly view Google’s deepened strategic partnership with Anthropic as strengthening its multi-model AI portfolio in an increasingly competitive landscape—and reinforcing leadership in search, cloud services, and enterprise AI solutions. Goldman Sachs and others maintain Google Cloud as a top pick, citing this initiative’s role in countering the Microsoft-OpenAI alliance. Investment Insight: Deep ecosystem integration promises long-term growth acceleration for Google; investors should closely monitor milestone achievements and the pace of subsequent capital deployment.

3. U.S. Space Force “Golden Dome” Program – $3.2 Billion Contract Awarded to 12 Companies

Event Summary: On April 24, the U.S. Space Force awarded up to $3.2 billion in contracts across 20 projects to 12 companies—including SpaceX, Northrop Grumman, Lockheed Martin, and Anduril—to develop prototype space-based missile intercept systems. This forms a cornerstone of the Trump administration’s “Golden Dome” missile defense initiative, aiming to demonstrate an operationally capable integrated combat system by 2028. The program seeks to build a multi-layered missile defense network capable of countering ballistic missiles, hypersonic weapons, and drones. Market Interpretation: The defense and aerospace sector receives a substantial, tangible order boost. Institutions believe that, given unresolved geopolitical risks, continued advancement of the “Golden Dome” program will provide long-term, stable revenue streams for defense contractors. Participation by emerging firms like SpaceX also signals the Pentagon’s accelerating adoption of commercial innovation. Investment Insight: Despite clearer Middle East negotiation pathways, defense tech retains strong defensive characteristics—making it suitable for portfolio hedging. Investors should track contract execution progress and quarterly order growth among relevant firms.

IV. Cryptocurrency Project Updates

1. A dormant whale, inactive for two years, deposited 300 BTC (~$23.4 million) into Binance. These coins were originally withdrawn from Bitfinex three years ago when BTC traded at $19,329. The whale now holds ~$17.6 million in unrealized profit.

2. MicroStrategy founder Michael Saylor posted another update on the Bitcoin Tracker yesterday, captioning it: “The ₿eat Goes On.” Historically, MicroStrategy discloses its BTC purchases the day after such announcements.

3. Data: Major token unlocks scheduled this week include SUI (~$40 million), JUP, and SIGN.

4. VanEck analysts Matthew Sigel and Patrick Bush identified two historically bullish signals for Bitcoin: negative funding rates and a concentrated decline in hash rate—accompanied by cooling volatility. As U.S.-Iran tensions ease, Bitcoin’s realized volatility dropped from 56% to 41%, while the 7-day average funding rate turned negative at -1.8%, reaching its lowest level since 2023. Historically, negative funding rates correlate strongly with future gains: Since 2020, Bitcoin’s average 30-day return during negative-funding periods has been +11.5%, versus +4.5% overall—with a success rate of 77%. Funding rates below -5% generated +19.4% returns over 30 days. Additionally, hash rate has fallen to its 16th percentile over the past 30 days—the most concentrated drop since China’s mining ban in 2021. Of the past seven hash rate declines, six were followed by Bitcoin price increases within 90 days, with a median gain of +37.7%.

5. El Salvador added 8 BTC over the past 7 days and 31 BTC over the past 30 days, bringing its total holdings to 7,633.37 BTC—valued at $624 million.

6. On-chain analytics platform Arkham reported on X that the Ethereum Foundation has initiated unstaking of ~$48.9 million worth of ETH. On-chain data shows the Foundation deposited its wstETH into Lido’s unstETH contract; upon completion of the unstaking process, it will receive equivalent amounts of spot ETH.

Markets are closely monitoring the Foundation’s next move—particularly whether it will sell the newly unlocked ETH. Historically, the Foundation has periodically sold ETH to fund operations, consistently raising concerns about potential ETH selling pressure.

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

- Tech Earnings: Google, Microsoft, Meta, and Amazon all report earnings early April 30 (UTC+8). Markets will closely scrutinize AI capex commitments and cloud revenue growth.

- Federal Reserve: New developments possible on Kevin Warsh’s nomination; watch for Senate statements.

Institutional Views:

JPMorgan’s Global Market Strategy team states that although the Middle East conflict remains unresolved, the negotiation path has become markedly clearer—shifting macro focus from geopolitical risk premiums toward residual “stagflation” pressures. Within this framework, equity market divergence is expected to intensify: capital will favor structural themes less sensitive to economic cycles yet delivering consistent growth—especially AI and “security/resilience”-related investments—while commodity and pure cyclical sectors may see reduced weightings. Goldman Sachs similarly highlights DeepSeek’s AI model cost advantages, expecting them to accelerate agent application deployment and boost cloud demand. Overall, institutions maintain overweight recommendations on the tech and AI value chain, while urging investors to assess how this week’s tech earnings validate actual capex execution. Easing geopolitical risks combined with ETF inflows provide near-term support to crypto markets—but residual stagflation risks warrant caution.

Disclaimer: The above content was compiled using AI-powered search tools and verified manually prior to publication. It does not constitute investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News