Artemis Report: Is Kraken, Valued at $2 Billion, Undervalued?

TechFlow Selected TechFlow Selected

Artemis Report: Is Kraken, Valued at $2 Billion, Undervalued?

The $2 billion valuation reflects only the “cryptocurrency exchange” layer, while the combination of clearing services, banking licenses, and tokenized securities remains unpriced by the market.

Author: Alex Weseley

Translation & Editing: TechFlow

TechFlow Intro: Artemis has published an in-depth research report on Payward, Kraken’s parent company. Kraken recently raised $800 million at a $20 billion valuation—then promptly shelved its IPO plans. Yet over the past five months, it has secured a Federal Reserve master account, acquired derivatives clearing infrastructure, launched the world’s largest tokenized equity product, and forged a partnership with Nasdaq. Author Alex Weseley argues that the $20 billion valuation reflects only Kraken’s identity as a “crypto exchange,” while the combined option value of its clearing capabilities, banking licenses, and tokenized securities infrastructure remains unpriced by the market.

Background

Payward, Kraken’s parent company, raised $800 million from institutions including Jane Street and Citadel Securities at a $20 billion valuation, then confidentially filed an S-1 with the SEC to go public. If successful, Payward would become the second publicly traded crypto exchange after Coinbase. However, four months later—in March 2026—it froze its IPO plans, citing “unfavorable market conditions.”

At first glance, this appears to be a failed listing attempt. But over the five months since filing the S-1, Kraken’s pace of execution has visibly accelerated:

- Became the first digital asset company to obtain a Federal Reserve master account

- Acquired Backed Finance, vertically integrating tokenized equity issuance capability

- Announced a partnership with Nasdaq to co-build a tokenized asset gateway

- Completed its $550 million acquisition of Bitnomial, securing the full suite of CFTC licenses

- Deutsche Börse purchased secondary-market equity for $200 million

For a company widely perceived as a “crypto exchange,” this density of strategic moves is extraordinary. The April 2026 Bitnomial transaction reaffirmed the $20 billion valuation (Payward official announcement). The core thesis of this article is that at $20 billion, Kraken’s return distribution is asymmetric: downside is anchored by the valuation floor of a crypto exchange; upside depends entirely on execution across clearing, tokenization, and banking licenses.

What Kraken Looks Like Today

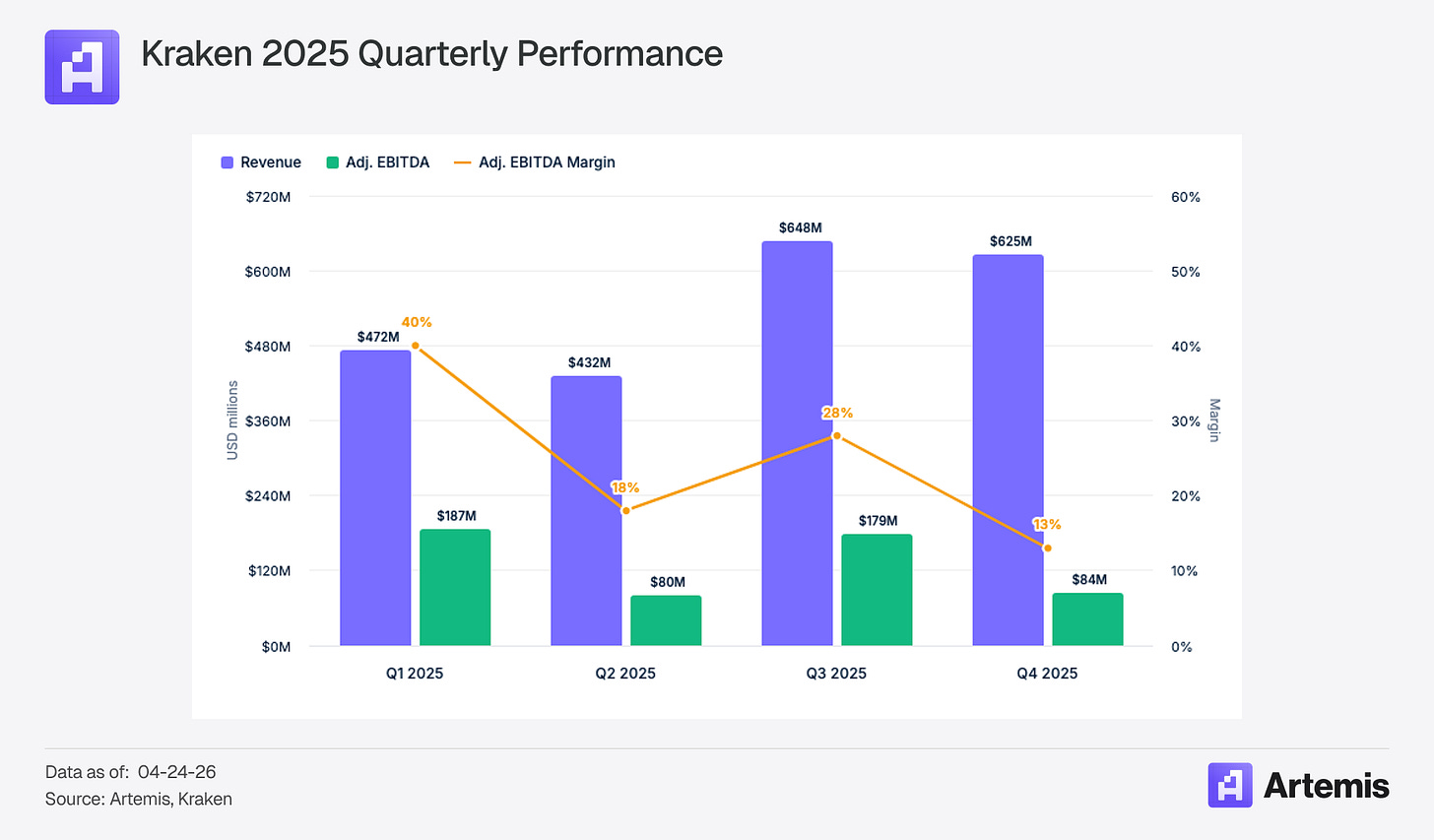

In 2025, Kraken reported $2.2 billion in adjusted revenue (+33% YoY) and $531 million in adjusted EBITDA. Operational metrics show 5.7 million active accounts (+50% YoY), $48 billion in platform assets (+11% YoY), and $2 trillion in platform trading volume (+34% YoY). Its revenue mix is more diversified than most assume: 47% from trading, and 53% from asset-related income (custody, yield, payments, financing). In most cases, Kraken’s primary revenue source is not trading. (Kraken financial data)

Caption: Kraken’s 2025 Revenue Breakdown

Upside Leverage

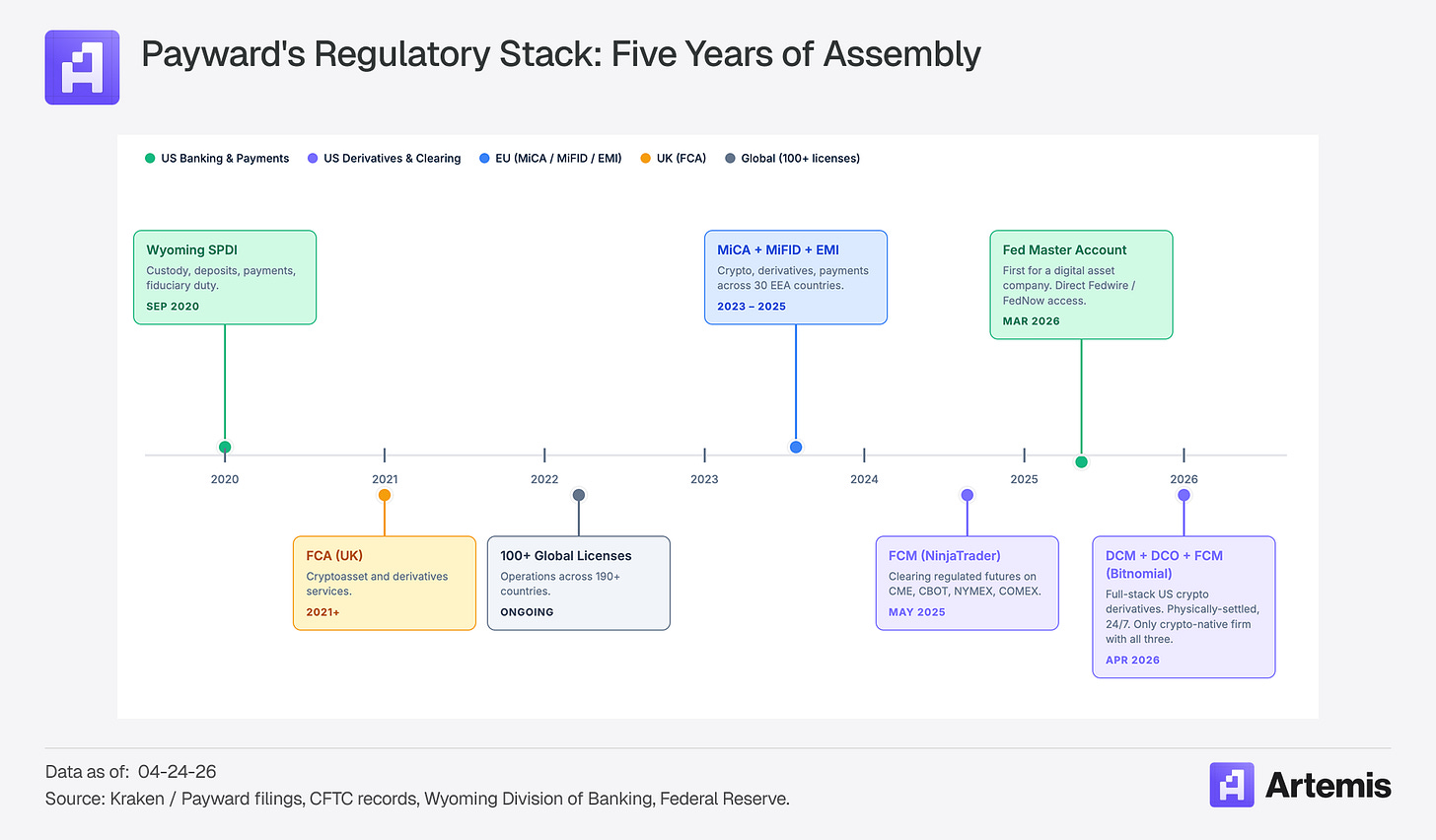

Regulatory License Portfolio

Kraken has spent over five years—and billions of dollars—building a regulatory and infrastructure stack unmatched anywhere in the crypto industry.

Caption: Kraken’s Regulatory License Matrix

The acquisition of Bitnomial is highly significant—it grants Kraken all three U.S. CFTC licenses required for crypto derivatives operations in one go: DCM (Designated Contract Market, i.e., exchange license), DCO (Derivatives Clearing Organization, i.e., clearinghouse license), and FCM (Futures Commission Merchant, i.e., broker-dealer license).

“The shape of a market is determined by its clearing infrastructure—not its front-end interface. The U.S. previously lacked clearing infrastructure built specifically for digital assets. Bitnomial spent ten years building exactly that: crypto settlement, crypto collateral, and a 7×24 continuous market. These capabilities cannot be retrofitted onto legacy systems.”

— Arjun Sethi, Co-CEO

Combined with its prior acquisition of NinjaTrader—which brings a distribution channel serving 2 million retail futures users—Kraken now owns a vertically integrated derivatives stack spanning front-end to clearing. Being the first to integrate DCM, DCO, and FCM with physical delivery, crypto-native collateral, and 7×24 markets under one roof is itself a structural moat. Clearinghouses are natural monopolies with powerful scale effects. Once institutions connect their risk management systems to Kraken’s DCO, switching costs become prohibitively high. CME dominates the futures market—not because its interface looks better—but because everyone clears there.

Other industry players are also moving toward compliant infrastructure, but via different paths. Coinbase recently received conditional approval for an OCC national trust charter, enabling uniform custody and settlement across all 50 U.S. states—a logical move for a firm already serving as custodian for most U.S. spot crypto ETFs. Kraken’s Wyoming SPDI (Special Purpose Depository Institution) charter is state-level, yet broader in scope: it permits accepting deposits, offering payment services, and operating under fiduciary duty. This distinction is critical—it allows Kraken’s roadmap to extend into bank-like products (deposit accounts, stablecoin issuance, FedNow payments), which a pure custody charter cannot support. The Federal Reserve master account secured in March 2026 serves as the foundational infrastructure layer activating these capabilities.

Tokenized Equities and xStocks

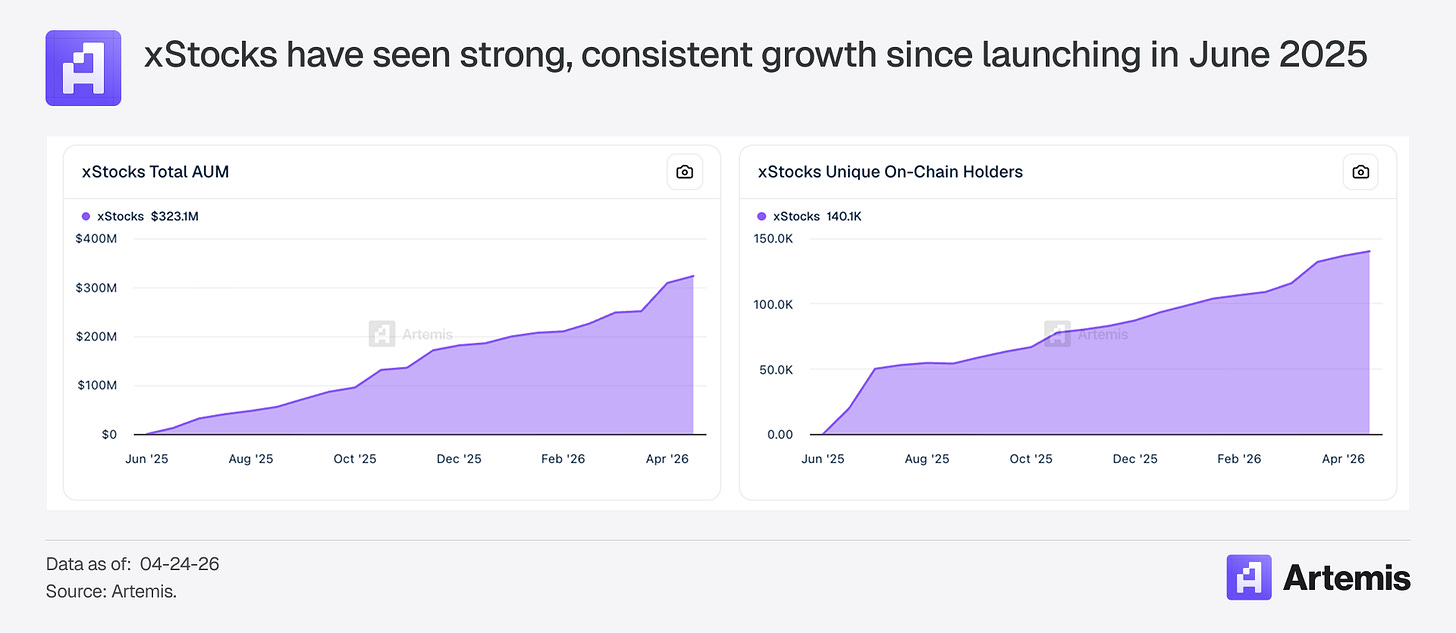

In June 2025, Kraken partnered with Backed Finance to launch xStocks, enabling 24/5 trading of tokenized U.S. equities and ETFs. Within less than a year, xStocks’ AUM surpassed $320 million, covering over 100 tokenized equities deployed across Ethereum, Solana, Ink, and Ton. xStocks is currently the world’s largest tokenized equity product.

In December 2025, Kraken announced its acquisition of Backed Finance—the Swiss issuer responsible for minting these tokens. With this, Kraken now controls the full vertical chain: issuance (Backed), trading (Kraken), settlement (Ink), and custody.

Caption: xStocks Tokenized Equity Product Architecture

This was followed by the Nasdaq partnership announcement:

“Nasdaq’s collaboration with Payward… will focus on designing an equity conversion gateway enabling issuers and investors to seamlessly move between permissioned and public blockchains.” (Nasdaq announcement)

Kraken is emerging as the owner of critical infrastructure bridging traditional securities and public blockchains. Nasdaq’s Equity Token framework is expected to go live in H1 2027, with Payward serving as the primary settlement layer. (Nasdaq has previously collaborated with Ondo, Republic, and others on tokenization initiatives; commercial terms remain undisclosed and products have yet to launch.)

Coinbase and Robinhood have both announced plans for tokenized equities—but as of April 2026, neither has launched a physically backed product. Kraken’s xStocks already boasts $323 million in AUM, 140,000 on-chain holders, and DeFi composability across multiple protocols. Kraken holds first-mover advantage—but $320 million in AUM represents more of an option value than a true moat. The Nasdaq partnership may serve as the catalyst that converts this option into durable competitive advantage.

Ink: The Tollbooth

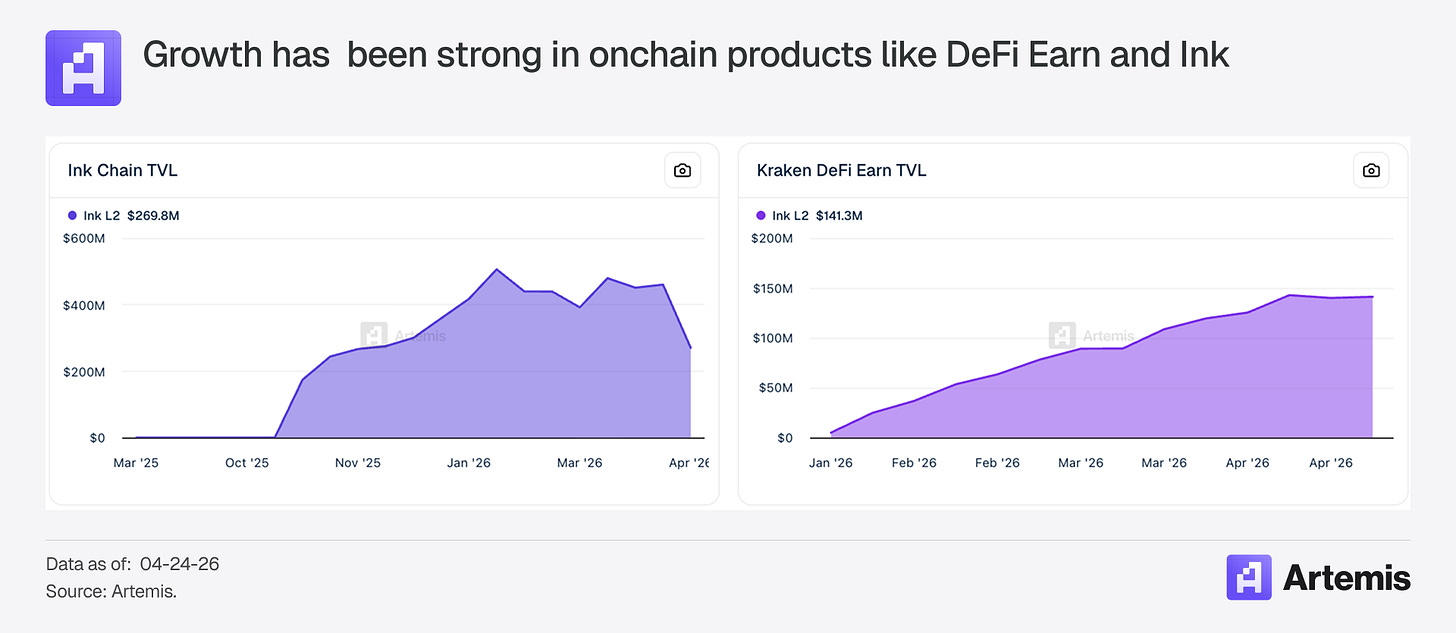

Ink is Kraken’s Ethereum L2, built on the OP Stack. It launched on mainnet in December 2024, with TVL hovering around $270 million (post-KelpDAO vulnerability incident). Application revenue surged from $500,000 in October 2025 to $5.77 million in January 2026. Kraken exclusively operates the sequencer—meaning 100% of gas fees accrue to Kraken.

Caption: Ink L2 Revenue Growth Trend

If xStocks settlement fully migrates to Ink, every tokenized equity transfer, DeFi interaction, and lending transaction will generate fees for Kraken’s sequencer. It functions like a tollbooth straddling traditional finance and onchain markets. Compared to more mature L2s, Ink remains early-stage—Coinbase’s Base generated ~$75 million in sequencer revenue in 2025, making it the largest L2 today. But Ink’s growth curve is steep, and it benefits from xStocks—a differentiated asset uniquely positioned to drive onchain activity, something no other L2 possesses.

The Platform Vision

Management has stated its growth priorities clearly: expanding asset classes (tokenized equities, FX, futures, RWAs), enhancing asset productivity (custody, payments, yield, financing, settlement), and scaling globally via a “single global core” paired with localized entry points. (Kraken blog)

Asset productivity carries the greatest valuation impact. This model is familiar: when Charles Schwab obtained its bank charter in 2003, the market widely questioned why a discount broker needed banking authority—but net interest income later became Schwab’s largest revenue stream. Of course, analogies have limits—Schwab was already the largest U.S. discount broker at the time, managing $800 billion in client assets. Kraken manages $48 billion in platform assets and has just secured its Fed master account. A more recent and relevant benchmark is SoFi: net interest income grew from $252 million in 2021 to $2.2 billion in 2025—but SoFi’s market cap sits near $23 billion. Markets recognize the bank economics model—but do not readily assign growth premiums. Kraken’s differentiation must therefore stem from its crypto-native foundation.

Early signs are already visible. Instant USD withdrawals (7×24×365, 1.5% fee capped at $50) are likely running on FedNow. The Kraken app has been downloaded over 450,000 times across 130 countries (The Block). Its unified wallet already enables cross-margining across spot, margin, and futures within crypto assets. The next logical step is extending cross-margining to crypto + xStocks + NinjaTrader futures—an exceptionally differentiated product, for which Kraken’s license portfolio provides the optimal foundation.

Stablecoins: The Biggest Gap

Stablecoins remain Kraken’s largest relative gap versus competitors. Coinbase’s USDC revenue-sharing agreement is projected to contribute ~$1.35 billion in 2025—high-margin, highly recurring revenue. Kraken lacks an equivalent income stream. USDG—the alliance stablecoin co-launched by Robinhood, Paxos, Galaxy, and Kraken—has a $1.95 billion market cap, dwarfed by USDC’s ~$76 billion. Kraken also maintains a distribution partnership with Circle and plans to issue a MiCA-compliant stablecoin from Ireland. Whether Kraken can close this gap—via scaling USDG, issuing a U.S.-domiciled stablecoin under its SPDI once the GENIUS Act passes, or through alternative routes—represents a key strategic question.

Valuation

Kraken does not fit neatly into any single category. It spans crypto exchanges, futures clearing, tokenized securities, banking, and L2 infrastructure.

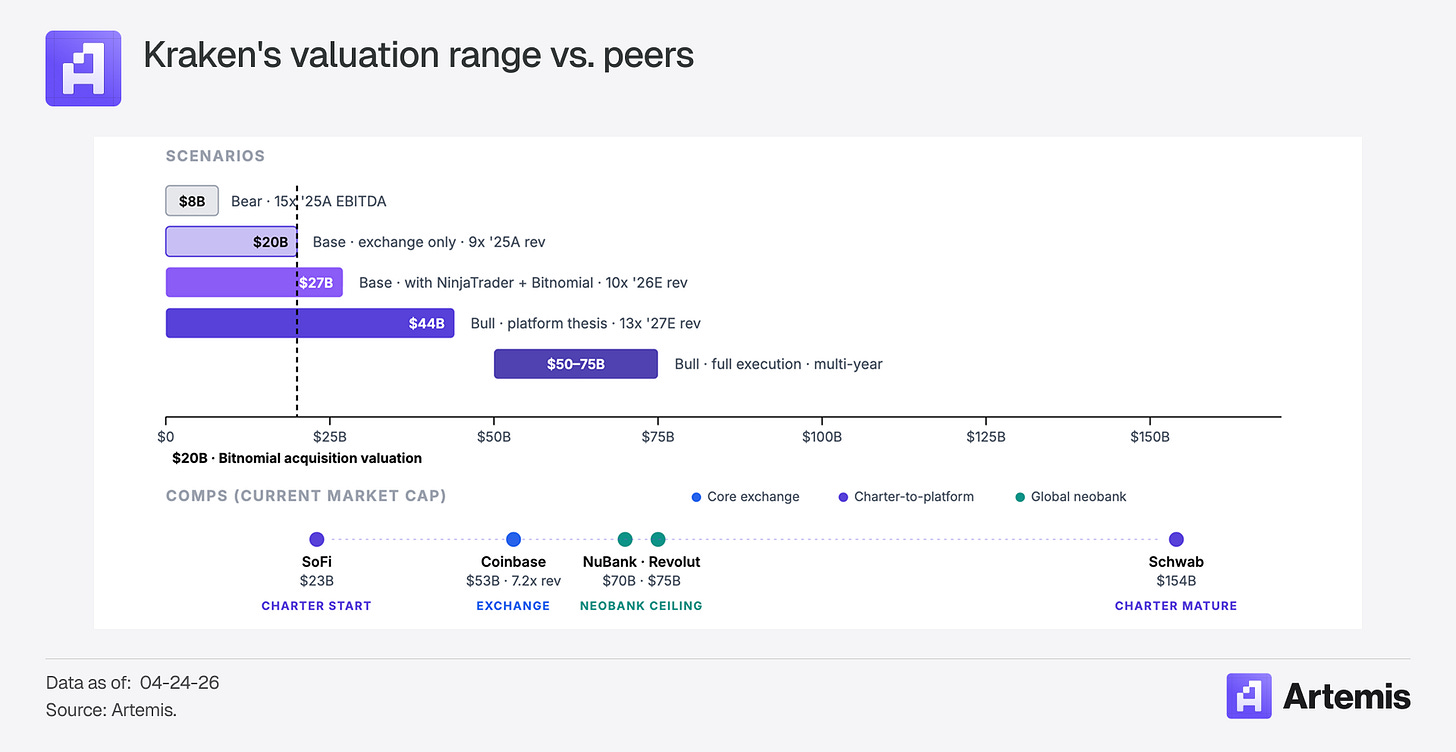

The $20 billion valuation is roughly fair for the parts of Kraken the market can verify today: a cyclical exchange valued at 8–9x revenue, plus a maturing derivatives business. Institutional investors in the November 2025 funding round priced what they could see. What remains underpriced is the forward-looking outcome distribution. Downside is anchored to the exchange valuation floor: even if the platform vision never materializes, the base case implies an enterprise value of $20–27 billion. Upside hinges on the execution of three independent—but unproven—catalysts: scaling Bitnomial’s clearing operations, launching xStocks in the U.S., and rolling out banking products on its Fed master account. Betting at this price isn’t about betting that the market misjudges today’s Kraken—but rather, betting that the outcome distribution starting from $20 billion is asymmetric: downside is bounded, upside is open-ended.

Caption: Kraken Valuation Scenario Analysis

Risks

Crypto cyclicality is the largest short-term risk. Revenue swung from $696 million in 2023 to $2.2 billion in 2025. Staking rewards, margin interest, and custody fees are all highly correlated with crypto prices. Regardless of how one parses the 47/53 revenue split, Kraken’s income is fundamentally crypto beta.

U.S. xStocks regulatory approval is the largest catalyst—and the largest uncertainty. xStocks has meaning without the U.S. market—but insufficient impact to shift the investment thesis.

Regulatory moats erode over time. As crypto regulation clarifies, more firms will secure more licenses. Kraken’s advantage lies in combination and first-mover status—not permanence.

Institutional entrants are inevitable. If tokenized equities achieve broad adoption, BlackRock, JPMorgan, Fidelity, and Goldman Sachs will enter with larger balance sheets, deeper client relationships, and ready-made distribution networks.

If Things Go Well

- U.S. xStocks launch: Step-function jump in trading volume, user count, and narrative momentum

- Banking products on Fed master account: Non-cyclical, recurring revenue

- Cross-asset cross-margining product: Attracting institutional capital currently without a home

- Bitnomial clearing infrastructure: Large-scale physically settled crypto derivatives

- Stablecoin issuance under SPDI: Direct net interest income

- NinjaTrader cross-selling: 10% conversion of 2 million futures traders = 200,000 high-value accounts

Kraken is the first crypto-native company to secure the full suite of U.S. clearing licenses—and it holds the world’s largest tokenized equity product. Whether this advantage compounds or gets eroded by competition will determine whether Kraken is merely a $20 billion exchange—or something far greater. No other company simultaneously holds clearing licenses, tokenized equities, banking charters, and a Federal Reserve master account. Any single component can be replicated. But the combination—built first—is precisely the bet embedded in this investment.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News