Bitget UEX Daily Report | U.S.-Iran Two-Week Ceasefire Takes Effect; Oil Prices Plunge Over 16%; Tech Stocks, Cryptos, and Gold Rally; Apple’s Foldable Phone Set to Debut in September

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | U.S.-Iran Two-Week Ceasefire Takes Effect; Oil Prices Plunge Over 16%; Tech Stocks, Cryptos, and Gold Rally; Apple’s Foldable Phone Set to Debut in September

Overall, this round of geopolitical easing has provided the market with a clear trading window, though volatility will persist as negotiation details unfold.

I. Top News

Federal Reserve Updates

Philip Jefferson, Vice Chair of the Federal Reserve, stated that a war involving Iran would introduce uncertainty and push U.S. inflation higher in the short term; however, the central bank’s current monetary policy stance remains appropriate. Jefferson described the current interest rate level as broadly “neutral”—neither stimulating nor restraining economic activity. He added that, under this stance, employment will remain supported, and inflation is expected to gradually recede toward the 2% target as tariff-related effects fade.

Global Commodities

U.S. and Iran Accept Pakistan-Brokered Ceasefire Proposal; OPEC Output Plunges to 40-Year Low

- Pakistan’s Prime Minister confirmed the U.S.-Iran ceasefire will take effect at 3:30 a.m. local time in Iran on April 8 (8:00 a.m. Beijing time); Trump agreed to suspend bombing attacks against Iran for two weeks, contingent upon Iran reopening the Strait of Hormuz; Iran’s Supreme National Security Council approved the ceasefire and submitted a 10-point proposal, with negotiations set to begin in Islamabad on April 10.

- OPEC’s March crude oil output plunged by 7.56 million barrels per day (a 25% decline) to 22 million bpd—the steepest monthly drop in at least 40 years—primarily due to export disruptions caused by Middle East conflict.

- Market impact: The ceasefire announcement triggered an immediate oil price collapse, easing supply-chain concerns—but also highlighted the fragility of global energy supply amid geopolitical tensions. Commodity volatility is expected to remain elevated in the near term.

Macroeconomic Policy

IMF Warns of Volatility Risks from Non-Bank Capital Flows in Emerging Markets

- Chapter Two of the IMF’s Global Financial Stability Report notes that funds managed by non-bank financial investment institutions are highly sensitive to global risk sentiment and exhibit significantly greater volatility than traditional banks—increasing vulnerability in emerging markets.

- Emerging economies have increasingly relied on non-bank financing channels in recent years, making them prone to rapid capital outflows during global shocks.

- Market impact: Contrasting with current geopolitical de-escalation, this serves as a reminder for investors to remain cautious about external funding uncertainties—even as risk appetite improves—potentially reinforcing dollar safe-haven demand.

II. Market Recap

Commodities & FX Performance

- Spot Gold: Gained over 2% in Asian trading, reclaiming levels above $4,800—marking its second consecutive daily rally—supported by reduced but still elevated safe-haven demand following the ceasefire news.

- Spot Silver: Rose nearly 5%, closely tracking gold’s rebound, driven by both industrial demand and safe-haven appeal.

- WTI Crude Oil: Fell 14% to $96.98—a sharp correction fueled by the U.S.-Iran two-week ceasefire agreement and rapidly improving market expectations for Strait of Hormuz navigation resumption.

- Brent Crude Oil: Dropped 13% to $95.20, mirroring WTI’s move as geopolitical risk premiums rapidly unwound.

- U.S. Dollar Index: Declined modestly by 0.67% to 99, reflecting improved risk appetite and weaker safe-haven demand.

Cryptocurrency Performance

- BTC: Up over 4% in 24 hours, briefly breaking above $72,000. Technical analysis shows early weakness amid escalating geopolitical tension, followed by a strong rebound post-ceasefire—breaking key resistance and signaling significant improvement in market risk sentiment.

- ETH: Up over 5.55% in 24 hours, briefly surpassing $2,250. Outperformed broader markets, benefiting from broad-based sentiment recovery and synchronous momentum with Bitcoin.

- Total Crypto Market Cap: Rose ~4% in 24 hours, returning to approximately $2.53 trillion.

- Liquidations: ~$600 million liquidated in 24 hours—$431 million in short positions. Forced short covering accelerated upward price movement.

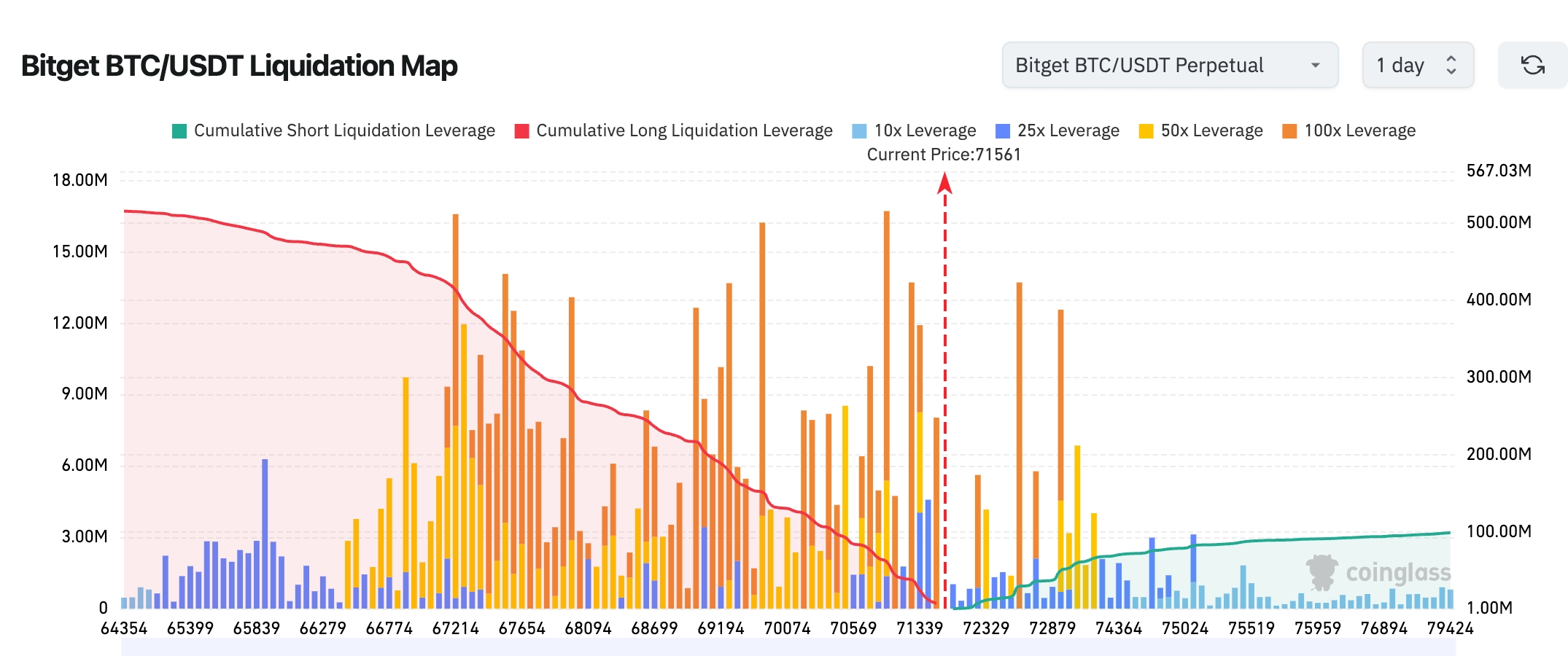

- Bitget BTC/USDT Liquidation Map: A dense cluster of long-position liquidations (red lines trending downward) lies just below the current price (~$71,561), suggesting a potential liquidity waterfall if prices fall. Short-position liquidations above are relatively dispersed but accumulating; a breakout above the $71,500–$73,000 range could trigger a short squeeze.

- Spot ETF Net Inflows/Outflows: BTC spot ETFs recorded net outflows of $142 million yesterday (vs. $471 million net inflows the prior day); ETH spot ETFs saw net outflows of ~$48.2 million (vs. $120 million net inflows the prior day).

- BTC Spot Flows: $3.003 billion in inflows vs. $2.819 billion in outflows—net inflow of $184 million.

U.S. Equity Index Performance

- Dow Jones Industrial Average: Down 0.18% to 46,584.46—dragged early by Trump’s ultimatum but stabilized late; overall trend remains cautious.

- S&P 500: Up 0.08% to 6,616.85—key feature: turned positive late in the session to extend gains to five consecutive days, reversing earlier losses on ceasefire optimism.

- Nasdaq Composite: Up 0.1% to 22,017.85—driven by broad-based tech sector strength; extended its winning streak to five days.

Tech Giants’ Moves

- NVIDIA (NVDA): +0.26% to $178.10—AI demand continues to provide solid support.

- Apple (AAPL): –2.07% to $253.50—despite positive news confirming its foldable iPhone launch in September, shares were weighed down by broader market volatility.

- Alphabet Class A (GOOG): +1.82% to $305.46—benefited from improved risk appetite.

- Microsoft (MSFT): –0.16% to $372.00—relatively stable performance.

- Amazon (AMZN): +0.46% to $213.77—steady e-commerce and cloud business fundamentals.

- Meta (META): +0.35% to $575.05—signs of recovery in social advertising revenue.

- Tesla (TSLA): –1.75% to $346.65—automotive sector showed clear divergence. Summary: Ceasefire-driven risk-asset rally benefited most tech giants, though Apple saw a slight intra-day pullback due to timing of news digestion.

Sector Rotation Highlights

Energy Sector led declines (dragged by oil price collapse)

- Representative stocks: Oil-related companies broadly fell 2–5%.

- Catalyst: Two-week ceasefire agreement and improving Strait of Hormuz access expectations led to rapid unwinding of geopolitical risk premium.

Tech/Semiconductor Sector staged a strong rebound

- Representative stocks: NVIDIA +0.26%, Google +2.11%.

- Catalyst: Risk sentiment recovery combined with unchanged long-term AI themes; further boosted by strong futures gains late in the session.

III. Deep-Dive Stock Analysis

1. Apple Inc. — Foldable iPhone Confirmed for September Launch

Event Summary: Apple dispelled earlier “delay panic” by confirming its first foldable iPhone (iPhone Fold) will launch in September 2026 alongside the iPhone 18 Pro/Max series. It will feature the 2nm-process A20 Pro chip, with design and pricing details gradually becoming clearer. Market concerns around supply chain or technical hurdles causing delays have been directly alleviated. Market Interpretation: Analysts widely view this as reinforcing Apple’s leadership in high-end innovation; the foldable form factor may open a new growth vector. Goldman Sachs and other investment banks maintain “Buy” ratings, emphasizing Apple’s enduring ecosystem advantage. Investment Takeaway: Short-term share price has already priced in much of the positive news; investors should monitor pre-launch supply chain validation signals. Longer term, foldables may become Apple’s next major growth engine.

2. OPEC-Linked Energy Majors

Event Summary: OPEC’s March crude output dropped sharply by 7.56 million bpd (–25%), the largest single-month decline in over 40 years—mainly due to export disruptions among key members amid Middle East conflict. With the ceasefire now in place, markets anticipate a gradual supply recovery. Market Interpretation: Firms like Goldman Sachs note short-term oil price pressure has eased, but longer-term outlook hinges on OPEC+ production plans; energy stock valuations have already partially priced in the release of geopolitical risk. Investment Takeaway: Energy stocks face near-term headwinds; investors may consider valuation-recovery opportunities, but must remain alert to pace of supply restoration.

3. Broadcom (AVGO) — Expanding AI Chip Partnerships with Google and Anthropic

Event Summary: Broadcom announced a long-term AI chip supply agreement with Alphabet (Google) and expanded its multi-billion-dollar custom TPU and AI accelerator collaboration with Anthropic. The deal runs through 2031 and includes custom TPUs and networking components for Google’s next-gen AI racks; Anthropic will gain access to ~3.5 gigawatts of next-generation TPU compute capacity starting in 2027. Combined with Q1 AI semiconductor revenue of $8.4 billion (+106% YoY), AVGO’s after-hours stock rose over 3%. Market Interpretation: Investment banks broadly welcomed the news. Goldman Sachs noted robust demand for custom AI chips, which greatly enhances visibility into Broadcom’s AI revenue stream; Jefferies and others raised price targets, citing AVGO’s technological moat in AI accelerators and networking solutions as a durable competitive advantage. AI-related revenue is projected to exceed $100 billion by 2027, further cementing its core role in hyperscaler supply chains. Investment Takeaway: Amid persistently high AI capex, Broadcom’s status as a critical supplier offers exceptional growth certainty; investors should monitor order execution in upcoming quarters. Long-term allocation remains highly attractive.

4. NVIDIA (NVDA) — AI Compute Leader Rebounds Amid Improved Risk Sentiment

Event Summary: Boosted by the U.S.-Iran ceasefire, NVDA rose nearly 3% after hours, leading a broad semiconductor rebound. As the undisputed global leader in AI GPUs and accelerators, NVIDIA continues to benefit from explosive demand growth in data centers and generative AI training; Blackwell platform shipments are progressing steadily. Market Interpretation: Analysts note that geopolitical de-escalation reduces macro uncertainty—favorable for high-valuation tech stocks. Morgan Stanley and others maintain “Buy” ratings, underscoring NVIDIA’s irreplaceable pricing power and ecosystem stickiness in the AI stack. Coupled with large hyperscaler contracts, its FY2026 guidance further reinforces market confidence in long-term AI infrastructure demand. Investment Takeaway: Short-term geopolitical factors provided a catalyst for rebound; medium-to-long-term AI trends remain the dominant driver. Investors should track supply chain stability and new platform rollout cadence—NVDA remains a core holding in any tech portfolio.

5. Oracle (ORCL) — PIMCO Considers $14 Billion Debt Financing for AI Data Center

Event Summary: PIMCO is considering providing $14 billion in debt financing to Oracle for building a large-scale data center serving OpenAI—expanding AI infrastructure capacity. Market Interpretation: Analysts view Oracle’s continued leadership in AI compute infrastructure as a key strength; if finalized, this financing would significantly accelerate cloud business growth and deepen its strategic partnership with OpenAI. Investment Takeaway: With AI capex remaining elevated, Oracle’s growth trajectory is highly certain; investors should monitor financing progress for potential positive stock catalysts.

IV. Cryptocurrency Project Updates

1. Solana-based decentralized exchange Stabble issued an emergency notice urging liquidity providers to withdraw funds immediately, citing prior employment of a North Korean national at the project. This warning appears to have been triggered by on-chain investigator ZachXBT, who disclosed that a North Korean developer had worked for years on Solana DeFi infrastructure project Elemental.

2. Onchain Lens reported that BlackRock withdrew 2,607 BTC ($177.56 million) and 28,391 ETH ($59 million) from Coinbase.

3. Strategy disclosed it has purchased BTC equivalent to 2.2× Bitcoin’s “natural supply” year-to-date, earning a 3.7% return via its BTC Yield strategy—adding 24,675 BTC, worth ~$1.7 billion at current prices.

4. Canadian-listed SOL Strategies Inc. signed an agreement to acquire assets of Darklake Labs, a Solana-native zero-knowledge technology firm, for $1.2 million—including $200,000 in cash and $1 million in common shares.

5. According to CME Group’s official website, CME Group announced plans to launch Avalanche (AVAX) and Sui (SUI) futures contracts on May 4, pending regulatory approval. New products include AVAX futures (contract size: 5,000 AVAX), micro-AVAX futures (500 AVAX), SUI futures (50,000 SUI), and micro-SUI futures (5,000 SUI). CME reported average daily notional volume for crypto derivatives in March was ~$8 billion—up 19% YoY. Starting May 29, all CME crypto futures and options will support 7×24 trading.

6. CryptoQuant analyst Darkfost observed that despite ongoing geopolitical tensions and their economic fallout, the risk-asset environment remains challenging—yet some investors appear increasingly inclined toward long-term Bitcoin holding. Data shows Bitcoin’s long-term holder (LTH) supply is gradually rising, delivering constructive and positive signals.

As of late November last year, the 30-day moving average of LTH supply dipped to –674,000 BTC, but has since rebounded to positive territory—averaging an increase of ~308,000 BTC. This suggests investor behavior is shifting from selling to holding; while Bitcoin’s price remains range-bound, rising long-term holdings often precede price appreciation.

V. Today’s Market Calendar

Data Release Schedule

| 04:30 | U.S. | API Crude Oil Inventories | ⭐⭐⭐ |

| 10:00 | New Zealand | Interest Rate Decision | ⭐⭐ |

| 22:30 | U.S. | EIA Crude Oil Inventories | ⭐⭐⭐⭐ |

| 00:35 (next day) | U.S. | Fed Official Goolsbee Speech | ⭐⭐⭐ |

Key Event Previews

- U.S.-Iran Negotiations Kickoff: To be held in Islamabad on April 10—focus on Strait of Hormuz access details and implementation of the 10-point plan.

- OPEC Monthly Report: Watch for updated guidance on output recovery.

Wednesday, April 8

- 04:30 API Crude Oil Inventories; 22:30 EIA Crude Oil Inventories (★★★★☆ — inventory dynamics highly sensitive amid geopolitical tensions)

- Fed Releases March FOMC Minutes (expected to reflect a wait-and-see stance amid geopolitical/oil uncertainty) (★★★★★)

- Delta Air Lines (pre-market), Constellation Brands, Applied Digital (after-market); focus on jet fuel cost pressures and consumer demand resilience

Thursday, April 9

- U.S. February Core PCE Price Index, Q4 Final Real GDP Annualized Rate, Weekly Initial Jobless Claims (week ending April 4)

Friday, April 10

- U.S. March CPI YoY & MoM (★★★★★); University of Michigan Consumer Sentiment Index (Preliminary) + 1-Year Inflation Expectations (Preliminary)

*Trading Recommendation This Week: Maintain flexible positioning; closely monitor oil (WTI/Brent), VIX, and the U.S. Dollar Index. Geopolitical headlines drive short-term sentiment; inflation data and FOMC minutes shape medium-term direction.

Institutional Views:

Leading investment banks and analysts broadly agree the U.S.-Iran two-week ceasefire marks the timely realization of the “TACO scenario,” significantly easing geopolitical risk premiums in the near term—prompting oil price corrections and rallies across risk assets. Morgan Stanley notes that restored Strait of Hormuz access will rapidly relieve energy supply pressures, allowing WTI to retrace part of its recent gains—though longer-term outlook remains tied to OPEC+ actions. Goldman Sachs emphasizes that tech and crypto sectors stand to benefit first from improved risk sentiment, with the Nasdaq and Bitcoin likely extending their five-day winning streaks. Meanwhile, the IMF report cautions emerging markets about non-bank capital flow volatility—underscoring that, even amid ceasefire optimism, markets operate under a dual logic of “geopolitical easing + macro caution.” Consensus view: Near-term tailwind for risk assets; medium-term focus shifts to Fed policy and pace of supply normalization. Investors are advised to accumulate energy stocks on oil pullbacks while maintaining allocations to tech, gold, and crypto. Overall, this round of geopolitical easing provides a clear trading window—but volatility will persist alongside negotiation details.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News