Code Is Getting Cheaper, Licenses More Valuable: The Real Moat for Fintech in the AI Era

TechFlow Selected TechFlow Selected

Code Is Getting Cheaper, Licenses More Valuable: The Real Moat for Fintech in the AI Era

Code has become cheaper, yet AI is deepening the true moat for fintech.

Author: Matt Brown

Translated by TechFlow

TechFlow Intro: Matt Brown, Partner at Matrix VC, makes a counterintuitive argument: AI is making code cheaper—but the truly hard-to-replicate assets in fintech—banking licenses, underwriting data built up through credit losses, and risk models trained on real transaction volume—are becoming more valuable than ever.

“You can’t code your way to a banking license”—this line captures the entire article’s core thesis.

This is not just a fintech analysis. It’s a map of “which moats are harder” in the AI era.

Full text below:

The term “fintech” has long profited from ambiguity baked into its name.

“Fin” means volumes of emails from .gov domains, audits lasting months, compliance officers who know your SAR filing history better than you do, and weekday business trips to Charlotte or Washington, D.C. “Tech,” by contrast, evokes a sleek mobile app, a 10x improvement in user experience, and coffee chats about investing at Blue Bottle.

“Fin” and “tech” have always existed along a spectrum—but markets typically reward fintech companies that lean as far toward “tech” and as far away from “fin” as possible.

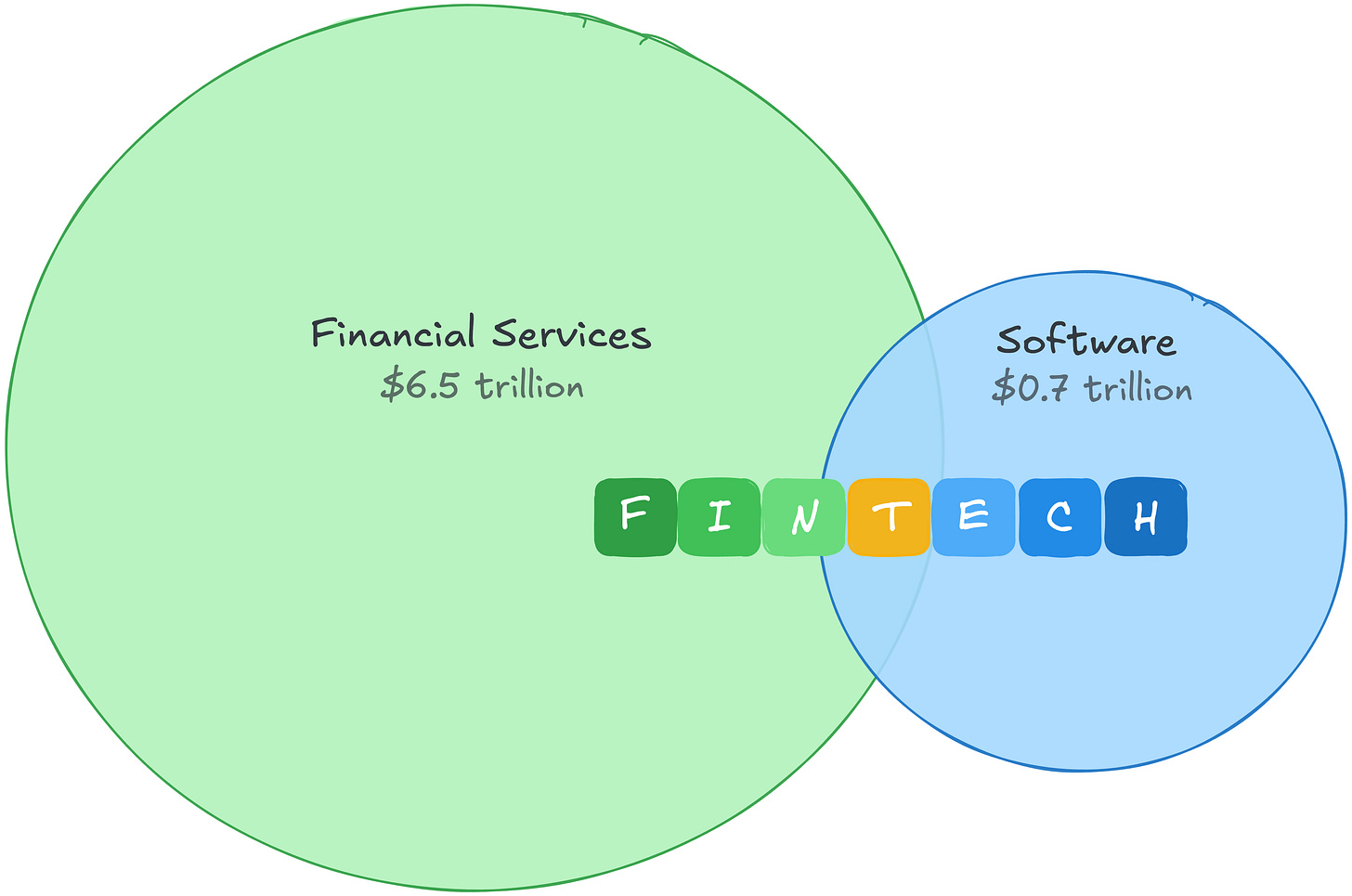

That’s understandable. In 2021, software’s gross profit pool was roughly $700 billion, commanding high multiples. Financial services’ gross profit pool was an order of magnitude larger—but valued far more conservatively. Fintech let you arbitrage both sides: financial services’ economics, paired with software-style valuation multiples.

That gap in gross profit pools also reveals where the real money lies. Financial services generates the largest gross profit of any industry globally. The “fin” side of fintech isn’t just more defensive—it’s a vastly larger market.

Then AI arrived—and the arbitrage disappeared. As investors reprice “how much code is worth in a world where code keeps getting cheaper,” software valuations compress. Fintech companies, classified by the market as software firms, get caught in the same downdraft.

But the market misclassified them. A fintech company’s costs—and its moats—have never resided in its code. And against the backdrop of AI-driven cost compression, those moats appear increasingly antifragile.

A Tale of Two Cost Structures

Software once enjoyed one of history’s best business models: code was expensive to build—but once written, distribution was nearly free. The gap between “expensive to build” and “free to distribute” was pure margin. If you were a SaaS company spending 22–25% of revenue on R&D, that very expense doubled as your barrier to entry. Competitors couldn’t easily replicate something built over years and costing tens of millions of dollars.

AI compresses that gap from the top down. If code becomes both cheap to build and cheap to distribute, margins narrow. The wall blocking competitors lowers—and more players enter, eroding pricing power.

If your business *is* software, this is a real problem. But fintech’s expenses aren’t engineering expenses. Follow the money, and the distinction becomes immediately clear.

PayPal spends 9% of revenue on R&D; Block spends 12%. That’s not because engineering doesn’t matter in fintech—Stripe’s engineering capability is world-class and a genuine competitive advantage. Rather, most of the money simply doesn’t flow to engineering.

It flows to “fin.” Unlike R&D spend—which produces a product—these costs produce moats:

Credit losses buy underwriting data

Affirm spends 35% of its revenue on credit losses and funding costs—before paying a single engineer. Every bad debt loss delivers repayment data competitors cannot access. A new entrant training models on synthetic data lacks real-world benchmarks. Synthetic data alone cannot establish a reliable loss history.

Compliance spend buys regulatory permission

Wise dedicates one-third of its workforce to compliance and financial crime prevention across more than 65 regulatory jurisdictions. Money transmitter licenses across 50 U.S. states, BSA/AML compliance programs, bank charter requirements—these aren’t advantages you build. They’re permissions you continually earn. You can’t code your way to a banking license.

Transaction volume buys proprietary data

Toast’s payments segment boasts a gross margin of ~22%, far below its SaaS segment’s 70%—yet generates nearly twice the gross profit. Those costs buy merchant-level transaction data, which in turn fuels Toast Capital—now having issued over $1 billion in loans. Adyen’s risk models are trained on transaction patterns across 30+ markets.

Fintech’s low margins have always been the point

Payment companies post gross margins of 20–50%, not 80%. But low margins don’t mean weak businesses. Fintech’s low margins reflect heavy spending that compounds into durable advantage. Even costs that don’t generate advantage lie outside AI’s cost-compression crosshairs.

AI strengthens every such moat. Better models lower loss rates. Better fraud detection reduces chargebacks. Better compliance tools let smaller teams manage more licenses. AI won’t replace moats—it rewards companies that choose to build where fintech is hardest: moving money, bearing risk, owning proprietary data, and navigating regulation.

So the real thesis isn’t just “AI helps fintech.” It’s that AI shifts value away from product surface area—and toward proprietary data, risk-bearing capacity, regulatory licenses, and distribution channels embedded in real money flows. If you’re building in those areas, AI compounds in your favor. If your differentiation lives in code, AI compounds against you.

Demand-side pressures are intensifying too. Every ambient-programmed checkout flow introduces a new fraud vector. Every autonomous trading AI agent increases chargeback risk. The more that’s built atop fintech infrastructure, the more indispensable that infrastructure itself becomes.

“Fin” is the winner

This insight is already forcing savvy fintech founders to rethink their position along the “fin” vs. “tech” spectrum:

Do we bear and price risk ourselves—or pass it to partners and let them capture the margin?

Do we own regulatory relationships—or rent them from those who do?

Does every transaction refine our own risk model—or train someone else’s?

Is our ledger a source of real data—or an incomplete mirror of someone else’s ledger?

This distinction cleaves the fintech landscape in two. Companies that own regulatory relationships, absorb credit losses themselves, and accumulate transaction data are building moats that AI will deepen. Those renting “fin”—using partner banks’ licenses, BaaS providers’ ledgers, or others’ risk models wrapped in better UIs—face the exact same problem as SaaS companies. Their differentiation lives in code—and code just got cheaper.

The old arbitrage—applying software valuation multiples to financial services economics—is dead. The new arbitrage is simpler: own “fin.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News