2025 South Korea CEX Token Listings Retrospective: Investing in New Tokens = 70% Loss?

TechFlow Selected TechFlow Selected

2025 South Korea CEX Token Listings Retrospective: Investing in New Tokens = 70% Loss?

The performance of tokens newly listed on Korean exchanges in 2025 shows no fundamental difference from Binance’s structural level.

By: c4lvin, Four Pillars

Translated by: AididiaoJP, Foresight News

Key Findings

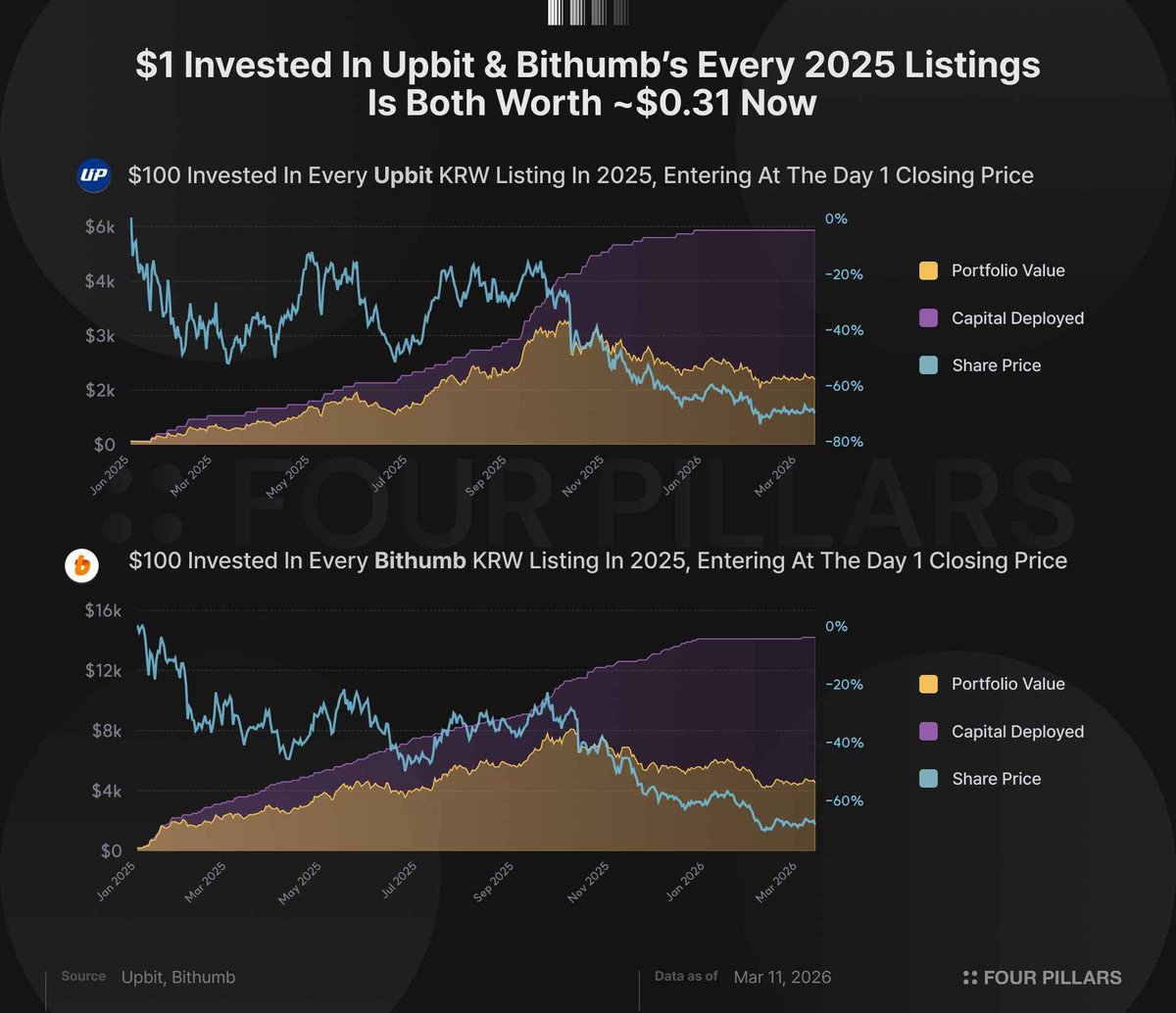

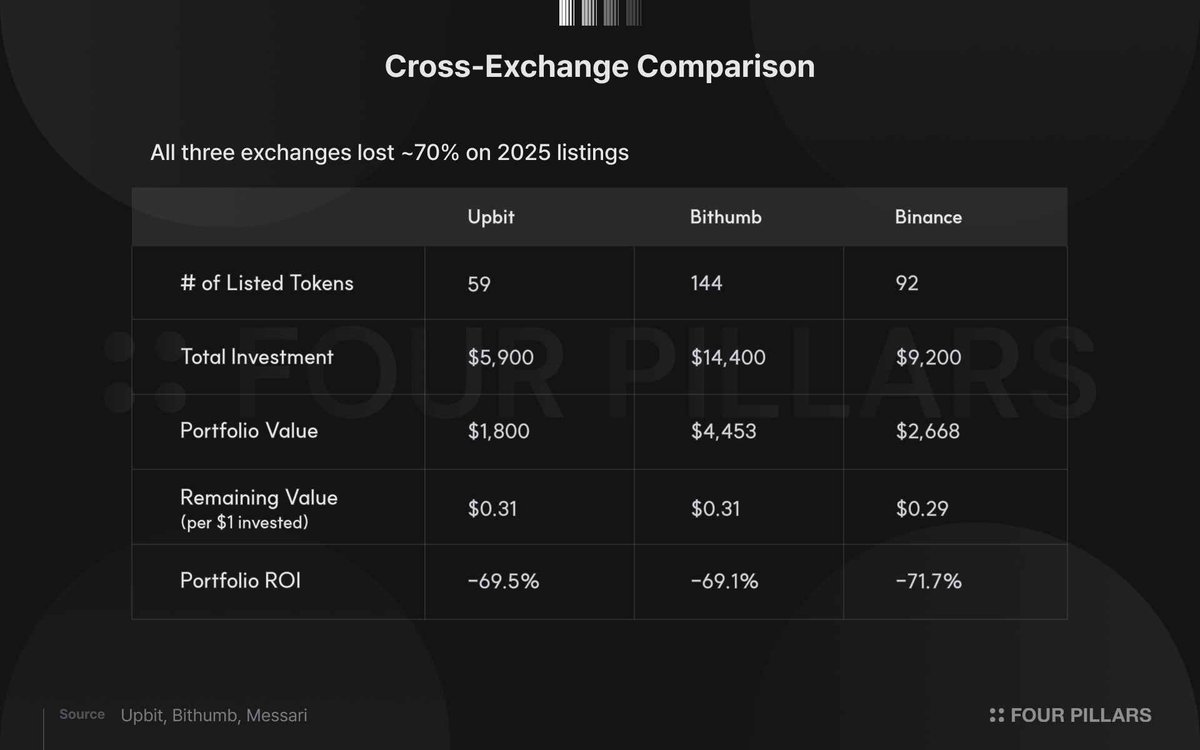

If $100 had been invested in each of the 59 tokens newly listed with KRW trading pairs on Upbit in 2025, the portfolio’s value would have declined to just 31% of the original investment (i.e., $0.31 per dollar invested) as of March 11, 2026. Bithumb—listing 144 tokens—showed an identical result of 31%, while Binance—listing 92 tokens—performed slightly worse at 29%. All three exchanges resulted in roughly a 70% loss of capital.

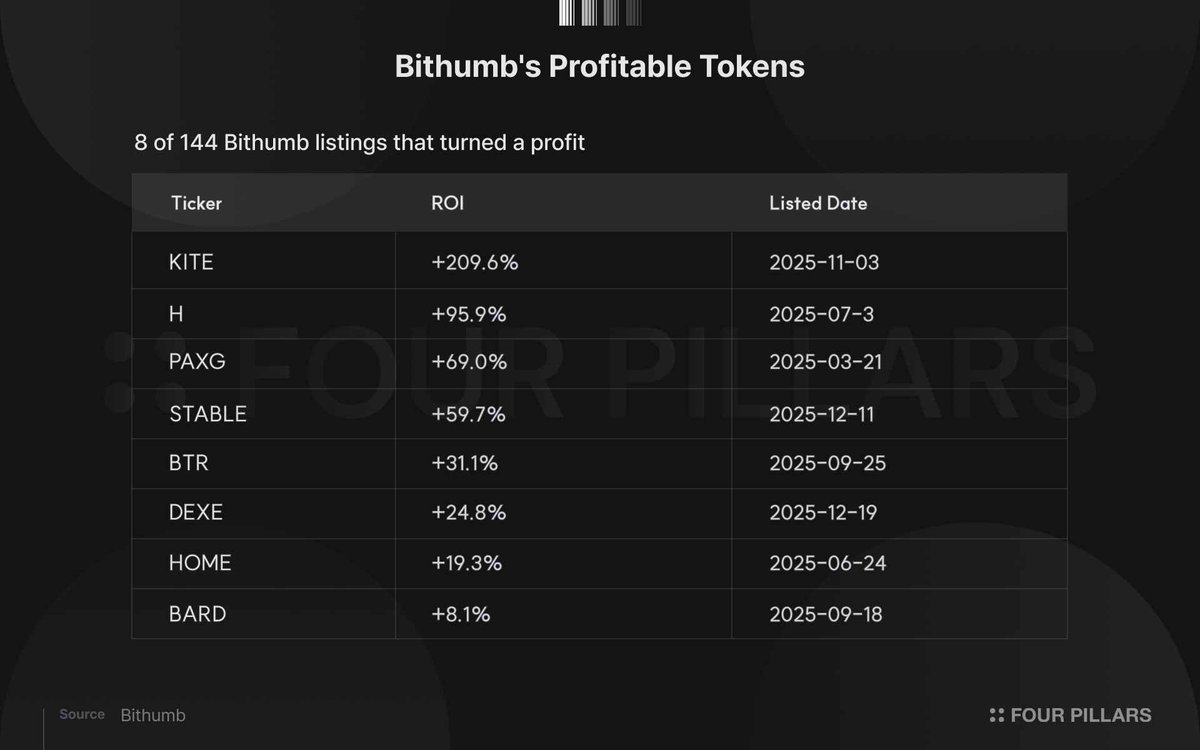

Among the 59 tokens listed on Upbit, only two ultimately generated positive returns: KITE (+232.8%) and BARD (+9.3%). Bithumb performed marginally better, with eight of its 144 tokens delivering positive returns. The median return for Upbit was –80.9%, versus –82.1% for Bithumb.

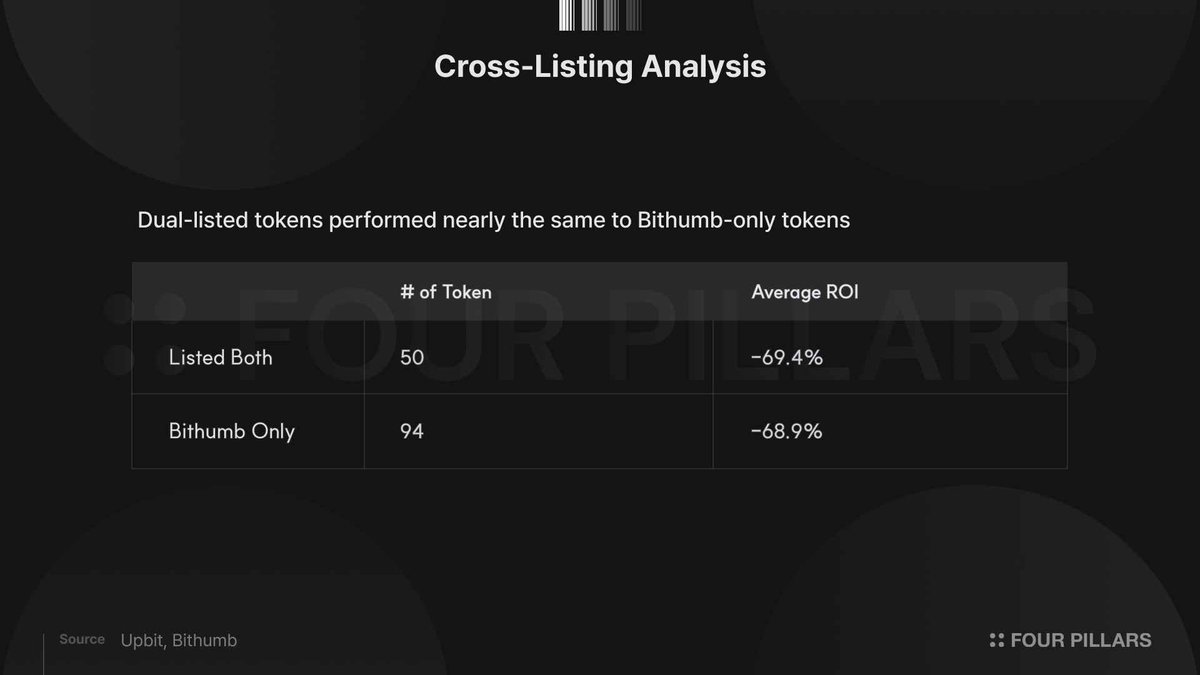

The 50 tokens listed simultaneously on both major Korean exchanges delivered an average return of –69.4%, nearly identical to the –68.9% average return of the 94 tokens listed exclusively on Bithumb. This suggests that listing on multiple mainstream exchanges offers no guarantee of improved subsequent price performance.

Research Background

This analysis was inspired by a data chart published today by Messari research analyst @Degenerate_DeFi.

Data source: @Degenerate_DeFi

The chart shows that if $100 had been invested in each of the 92 tokens newly listed on Binance in 2025, each dollar invested would be worth only $0.29 as of today—representing a cumulative loss of 71.7% across the total $9,200 investment, leaving approximately $2,600 remaining.

As the world’s largest cryptocurrency exchange by trading volume, Binance is widely perceived to apply stricter listing standards than smaller platforms and enjoys unparalleled liquidity advantages. If even Binance’s data looks this bleak, how do Korean exchanges fare? Korea’s market is retail-dominated and exhibits trading behaviors markedly distinct from global markets. Do these differences affect the performance of newly listed tokens—or will the data ultimately reveal similar patterns?

This article applies the same methodology used in the Binance analysis to systematically examine all tokens that received KRW trading pairs on Upbit and Bithumb throughout 2025.

Methodology

Scope and Selection Criteria

This study covers all tokens that launched new KRW trading pairs on Upbit and Bithumb between January 1 and December 31, 2025. Upbit added 59 tokens; Bithumb added 144. Tokens launched in 2025 but since delisted—Elixir (ELX), Strike (STRIKE), and AI16Z—are treated as total losses.

The investment simulation follows the standardized framework used by Messari in its analysis of Binance-listed tokens. We assume a $100 investment made at each token’s closing price on its first day of listing, held until today without any selling. Daily tracking of the portfolio’s cumulative value and return generates a time-series dataset.

Selecting the first-day closing price as the entry point was deliberate. On Korean exchanges, opening prices on listing day are often significantly inflated due to extreme volatility and speculative buying. Using the closing price effectively filters out this short-term noise.

Data Collection

All price data were retrieved directly via the public REST APIs of the respective exchanges. For Upbit, we used the daily OHLCV endpoint to collect full daily candlestick data from each token’s listing date through March 11, 2026, cross-verified against real-time ticker data (/v1/ticker). For Bithumb, we employed the 24-hour OHLCV endpoint for the same period. To simplify modeling, this study does not account for USD/KRW exchange rate fluctuations.

Overall Performance

The chart below visually presents the simulation results. Subsequent sections provide detailed interpretation and analysis.

Comparison Across Three Exchanges

Performance comparison of newly listed tokens across the three exchanges in 2025:

All three exchanges recorded losses of approximately 70%. Upbit (–69.5%) and Bithumb (–69.1%) performed nearly identically, while Binance (–71.7%) showed only a marginal difference. Regardless of exchange choice, investors who bought newly listed tokens on their first day lost about 70% of their initial capital on average.

Return Distribution Characteristics

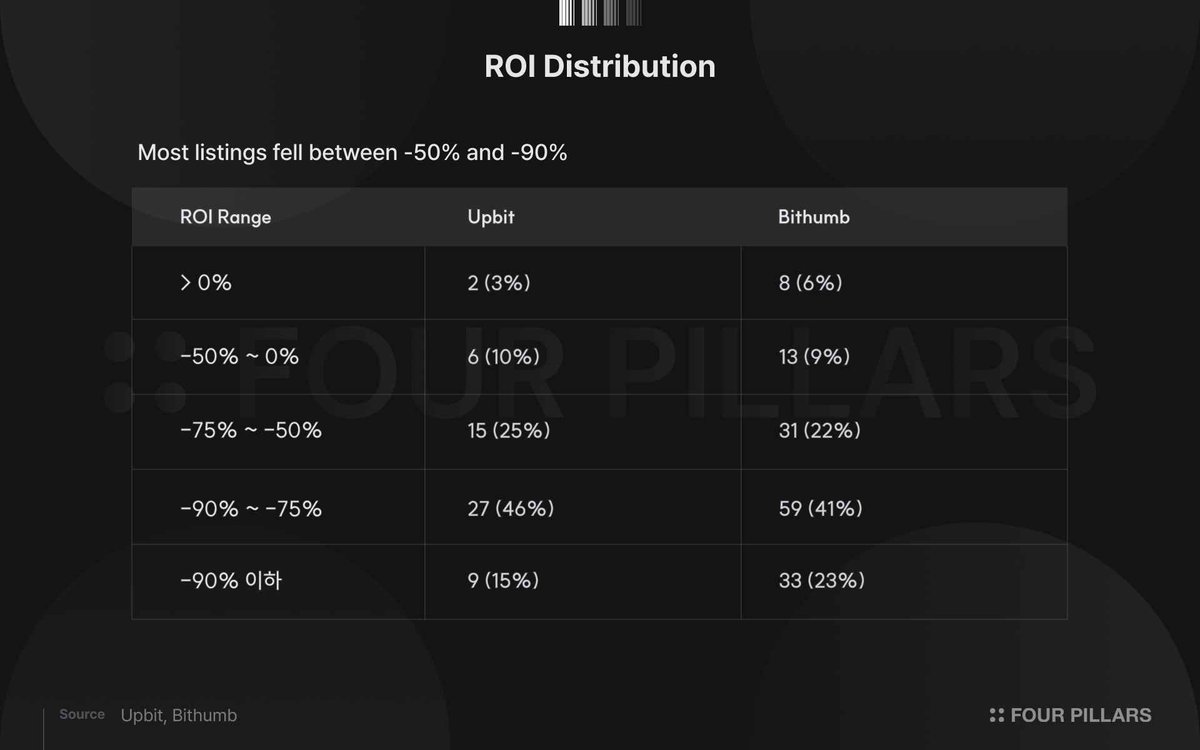

The overall mean alone fails to capture variation in individual token performance. Below is a detailed breakdown of token returns by range:

Over 40% of tokens on both exchanges fell into the –75% to –90% loss range. On Upbit, 46% landed in this band, with another nine tokens (15%) suffering extreme losses exceeding 90%. Only two tokens posted positive returns: Kite (KITE, +232.8%) and Lombard (BARD, +9.3%).

Bithumb’s return distribution is more dispersed. It hosts more profitable tokens—eight in total—but also saw 33 tokens lose over 90%. This dispersion partly reflects Bithumb’s larger sample size (144 tokens), but also indicates its listing strategy covers a broader spectrum of project types compared to Upbit.

Median returns reveal a starker reality: –80.9% for Upbit and –82.1% for Bithumb—both lower than their respective averages. This implies that a few relatively resilient tokens lifted the overall average, while the typical performance of newly listed tokens is far worse than the headline figures suggest.

Impact of Listing Timing on Performance

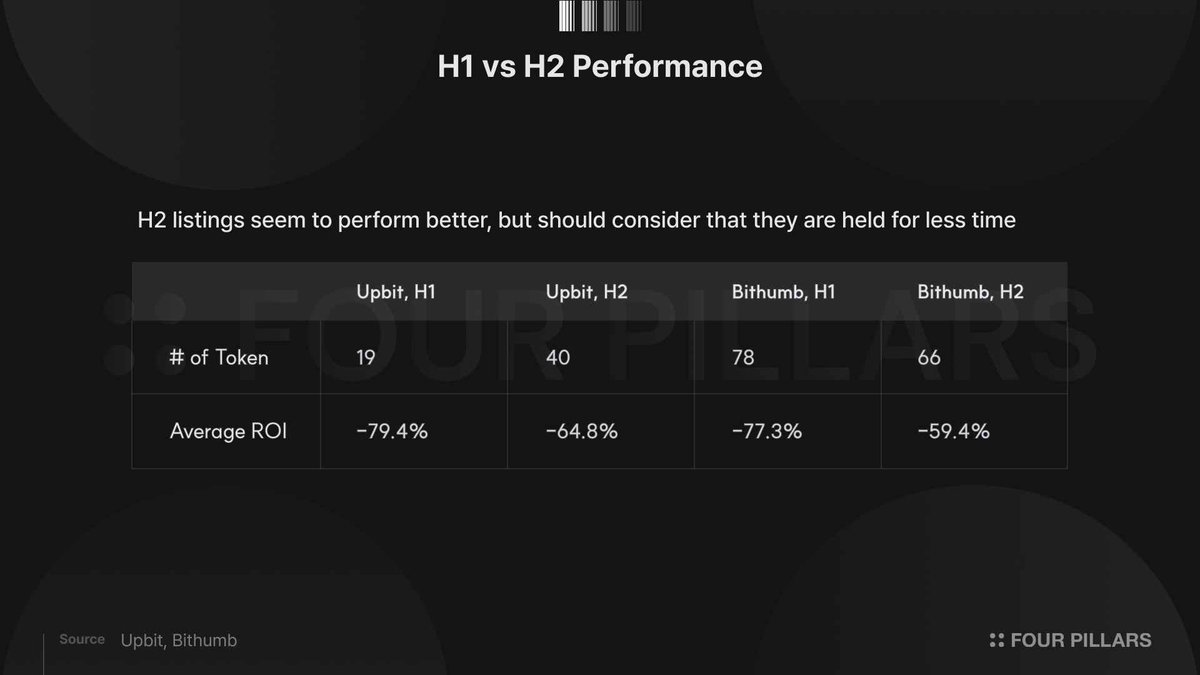

To assess whether listing timing affects subsequent performance, we split the data into two periods: H1 (January–June) and H2 (July–December).

The data show that tokens listed in H2 outperformed those listed in H1 on both exchanges. This aligns intuitively: tokens launched early in the year endured longer downward price trajectories. Given the overall bearish trend in crypto markets during 2025, the longer the holding period, the higher the probability of accumulating larger losses.

Notably, the performance gap between the two halves is substantial. On Bithumb, H1-listed tokens returned –77.3%, versus –59.4% for H2-listed tokens—a 18-percentage-point difference difficult to attribute solely to time. Possible explanations include stronger fundamentals among H2 listings or increased market rationality following lessons learned in H1.

The Paradox of Choice

Relationship Between Listing Volume and Performance

In 2025, Upbit added 59 new KRW trading pairs, while Bithumb added 144—more than double Upbit’s count and significantly exceeding Binance’s 92. Upbit is renowned among Korean exchanges for its strictest listing standards. Yet despite this stark disparity in listing volume, portfolio returns across the two exchanges are virtually identical: –69.5% for Upbit and –69.1% for Bithumb.

Analysis of Cross-Listed Tokens

To probe deeper, we further compared tokens listed on both exchanges versus those listed only on Bithumb. Data show that 50 tokens were listed simultaneously on Upbit and Bithumb.

Intuitively, projects achieving dual listings on major exchanges should enjoy greater industry recognition. Yet the average return of these 50 tokens (–69.4%) is virtually indistinguishable from the –68.9% average return of the 94 tokens listed solely on Bithumb.

This finding points to two conclusions:

First, multi-exchange listing offers no assurance of superior future price performance.

Second, the price surge on listing day is a structural phenomenon—not contingent on how much attention a project receives.

Whether a token enjoys the “prestige” of an Upbit listing or quietly debuts on Bithumb, first-day buyers experience essentially identical losses.

Analysis of the Few Survivors

Among Upbit’s 59 newly listed tokens, only KITE (+232.8%) and BARD (+9.3%) achieved positive returns. Just eight tokens limited losses to under 50%.

Bithumb’s eight profitable tokens form a more diverse cohort.

KITE’s +209.6% gain stands out as a clear outlier. However, given it has only been listed for four months, interpreting this as sustainable long-term performance remains premature. Similarly, STABLE and DEXE—each tracked for only three months—warrant cautious interpretation.

More instructive is the case of PAXG. As a token pegged 1:1 to spot gold prices, its +69.0% gain was driven entirely by gold’s steady appreciation in 2025—a macro trend wholly unrelated to cryptocurrency fundamentals. In other words, the most reliable path to profit on Bithumb turned out to be avoiding crypto projects altogether.

Conclusion

This study concludes that the performance of newly listed tokens on Korean exchanges in 2025 shows no essential structural difference from Binance’s. Despite Korea’s retail-dominated market structure, differing exchange listing strategies, and distinct regulatory environments, the average first-day buyer across all three exchanges suffered losses converging around 70%.

We argue the core insight revealed by this data is that the root cause lies not in any exchange’s listing criteria nor in the quality of individual tokens, but rather in the inherent structural dynamics of the listing event itself. When a token launches on a major exchange, concentrated retail demand inflates its price on day one. Over time, prices naturally revert, resulting in losses for first-day buyers. The convergence in performance between tokens listed on both exchanges and those listed on only one further confirms that these losses stem not from specific exchanges or tokens, but from the structural nature of the listing event.

It bears noting that this study measures performance under a single, specific strategy: buying at the first-day closing price and holding until today. Alternative strategies—such as short-term trading exploiting post-listing volatility or entering only after significant price corrections—could yield markedly different outcomes. However, such strategies demand extremely precise timing and diverge sharply from the behavior of most retail investors.

The 2025 data deliver a clear message: buying a token solely because it has newly listed on a major exchange is a systematically losing strategy—regardless of which exchange is chosen. This phenomenon is not unique to Korea; it is a global structural issue. The problem is not that exchanges select low-quality projects, but that the listing event itself creates a dynamic of concentrated demand—one persistently disadvantageous to first-day buyers.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News