Pricing OpenAI Pre-Market: A New Six-Month Life-or-Death Business on Hyperliquid

TechFlow Selected TechFlow Selected

Pricing OpenAI Pre-Market: A New Six-Month Life-or-Death Business on Hyperliquid

Ventuals shuts down; not all pre-IPO opportunities for star tech stocks on-chain are good deals.

Author: Kuli, TechFlow

During SpaceX’s IPO week, the pre-market price of SPCX on Hyperliquid flooded social feeds—but few paused to ask who was behind this market.

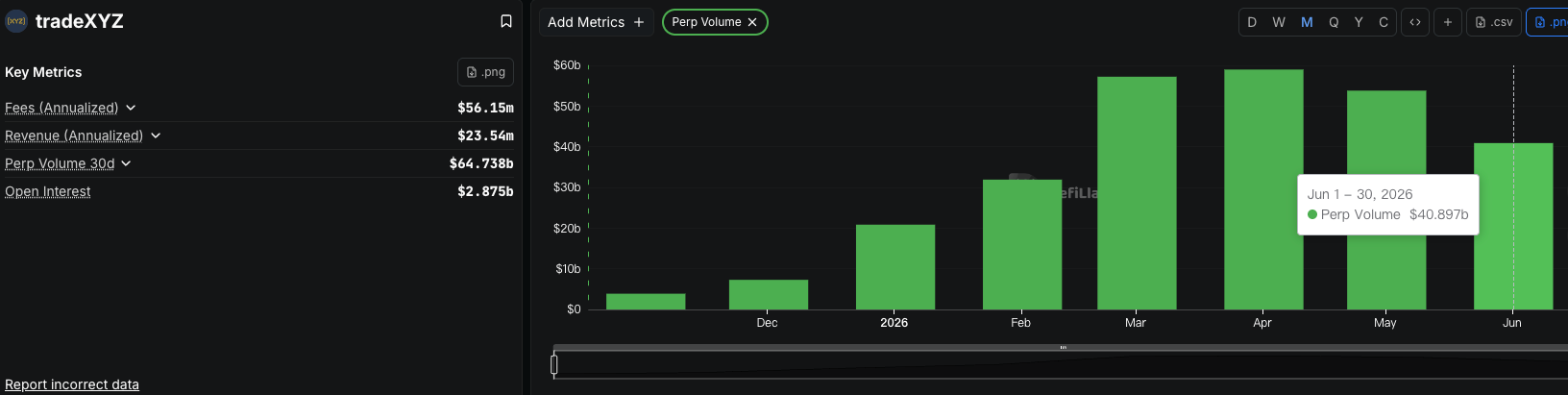

The answer is Trade.xyz—a fully anonymous team that emerged only this year. Today, it holds over 90% of all open interest in pre-market contracts on Hyperliquid. The entire wave of on-chain SpaceX pre-IPO enthusiasm was essentially driven by this single team.

Yet just three days after SpaceX rang the Nasdaq bell—on June 15—another team operating in the same space announced its shutdown.

This team was Ventuals, backed by Paradigm. It offered pre-market contracts for SpaceX—and also for OpenAI and Anthropic. Launched earlier this year, it folded just nine months after going live.

Same chain. Same HIP-3 framework. Same niche. One team turned SpaceX into the largest pre-market venue on Hyperliquid; another held OpenAI and Anthropic—the two scarcest, most coveted names in the space—yet still failed.

What merits closer scrutiny is *how* Ventuals exited. According to its official social media announcement, it didn’t collapse from losses or vanish. Instead, it stated it had been acquired, with its entire team integrated into another project within the Hyperliquid ecosystem. Users received full 1:1 principal refunds—an orderly, dignified wind-down.

But here lies the puzzle: holding OpenAI and Anthropic—the two rarest, most sought-after names in the sector—should have made Ventuals the *least* likely candidate to exit. So where did it go wrong?

Trade.xyz vs. Ventuals

The successful player today—Trade.xyz—remains fully anonymous.

Its founder revealed only a few details in an interview with Hyperliquid co-founder Jeff Yan: he bought his first Bitcoin in 2013 for $66, has since operated solely as an investor—not a builder—and says he would have left crypto entirely had he not met Jeff.

Yet this relative newcomer built Hyperliquid’s largest pre-market venue. According to Colossus, Trade.xyz has grown weekly by 38% since October last year, amassing over $130 billion in cumulative trading volume.

It started with silver, then crude oil, then the S&P 500—before finally launching SpaceX.

Its choice of SpaceX was astute.

SpaceX’s Nasdaq listing on June 12 came with a fixed IPO price and date. By listing a pre-market contract, Trade.xyz was effectively betting on an outcome whose resolution was certain and imminent—the Nasdaq would deliver the “true” price on listing day. That true price acted like an anchor, preventing the pre-market price from drifting too far. Even if interim quotes deviated, the listing-day price would pull them back into alignment.

That’s exactly what happened. In the days before listing, SPCX traded between $154 and $172—pricing in a premium over the $135 IPO price. At market open, the price surged upward—confirming the bet.

Ventuals chose a different class of asset.

Backed by Paradigm—one of crypto’s top-tier VCs—it carried far more institutional pedigree than anonymous Trade.xyz. Its marquee assets were even bigger: OpenAI and Anthropic—the two scarcest names in the space.

Yet neither company has a near-term listing date.

External anchor prices do exist. Bloomberg reported that Anthropic recently priced employee secondary sales at a $350 billion valuation; OpenAI does similar transactions regularly. But these are closed-door valuations—secondary trades often involve only long-standing, heavily invested insiders. The assets don’t truly change hands in an open market.

Such valuations may be precise at times—but they lack a public order book where anyone can step in and correct them.

By bringing such prices on-chain as contract references, Ventuals effectively suspended the entire market on one or two off-chain price feeds. Worse, it layered on a self-reinforcing pricing mechanism.

On-chain analysts have reverse-engineered Ventuals’ pricing logic:

Its oracle price drew half from external secondary transactions and financing rounds, and half from the contract’s own moving average price. In other words, half the price referenced itself. When buy pressure pushed the price up, the moving average rose, pulling the oracle higher—and lifting the price ceiling further, enabling yet more upward momentum.

The result? Prices for OpenAI and Anthropic contracts stayed persistently near their ceilings, making sell orders and liquidations extremely difficult to execute. Charts looked steadily bullish—but in reality, prices were structurally stuck, decoupled from genuine supply-and-demand dynamics.

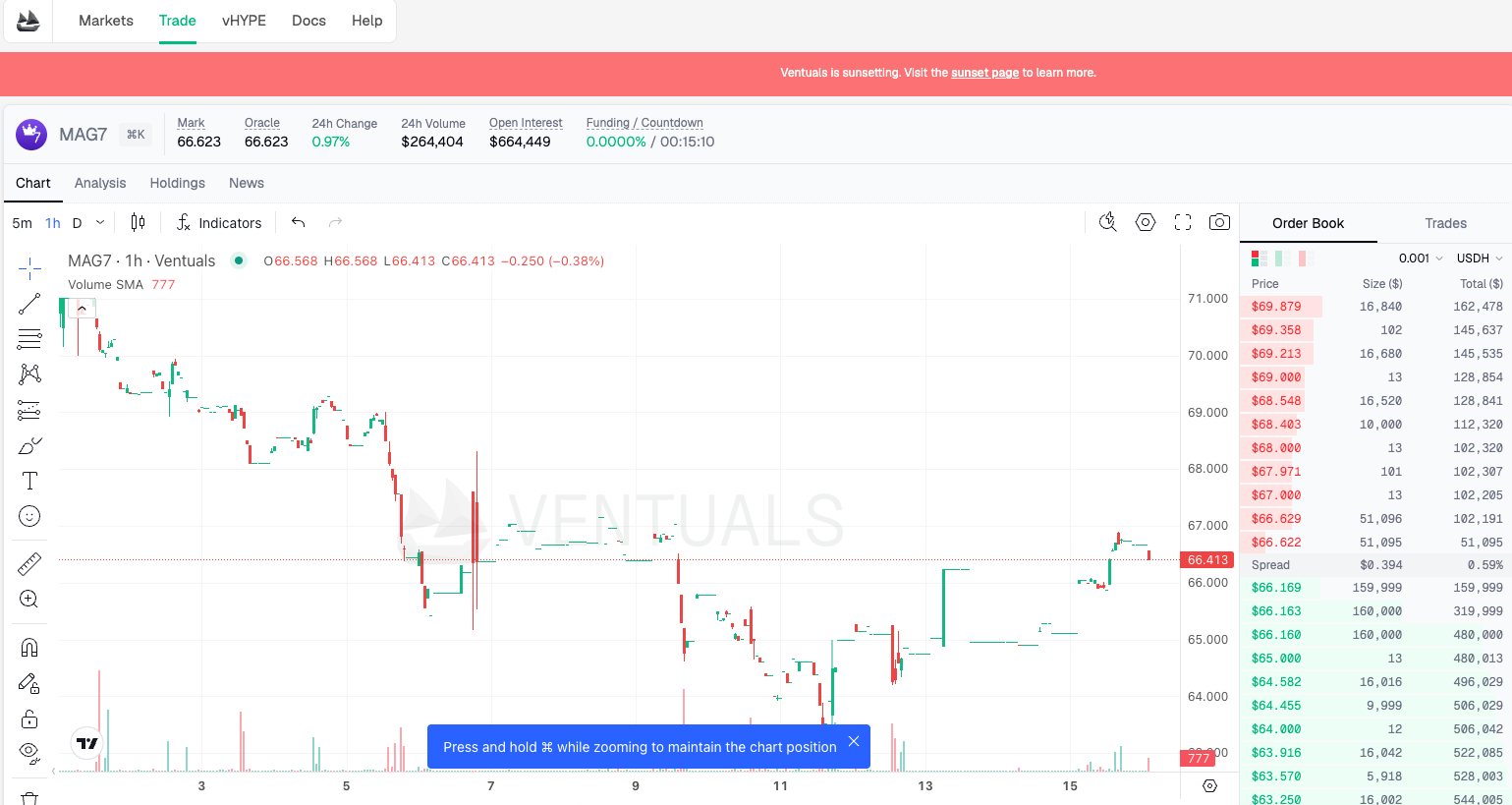

Source: MAG7 assets on Ventuals—note the fragmented candlestick chart and extended periods without trades

So this kind of pre-IPO isn’t so much the market telling you what OpenAI is worth—it’s more like a machine pushing the price up, then using that artificially inflated level as its next reference point.

Trade.xyz wagered on an asset destined for Nasdaq settlement—wrong bets were corrected by a real-world price floor. Ventuals wagered on assets existing only in private valuations—with a self-circular pricing layer added on top. Its prices floated mid-air, unmoored from any foundation.

Shutdown Reference Prices: OpenAI at $1,300, Anthropic at $1,600

When winding down, does its final quoted price hold weight?

At shutdown, Ventuals needed to set a final price to settle all outstanding positions. Its method? Freeze the 24-hour time-weighted average price. OpenAI settled at $1,341.80 per share; Anthropic at $1,618.90.

These figures are now permanently recorded in the settlement ledger—the last on-chain price tags for both companies.

As noted earlier, this price relied half on external secondary valuations and half on its own moving average—meaning it had been climbing steadily against its ceiling. In other words, $1,341.80 included a significant component lifted—not by market consensus—but by the system reinforcing its own prior output.

It’s precise to two decimal places—but not necessarily truthful.

The irony? Some people outside *did* take it seriously.

According to Bloomberg, employees of SpaceX, OpenAI, and Anthropic—as well as late-stage VCs—approached Ventuals, stating they used its platform to value their equity stakes.

This deserves unpacking.

These individuals hold real shares—so they should know better than anyone what their stock is worth. Yet primary-market valuations emerge only once a year, like toothpaste squeezed from a tube. Between funding rounds, the market goes dark—no one knows whether the price rose or fell.

Ventuals, however flawed, at least posted a number 24/7—and showed directionality.

Hence a paradoxical inversion: the very insiders who should wield the strongest pricing authority instead fixated on a number generated on a retail trading desk—seeking psychological reassurance.

That’s the core tension in pre-IPO pricing.

The scarcest assets are precisely those most starved of fair, transparent pricing. The greater the scarcity, the more eagerly people latch onto anything resembling a price—even if it’s a machine echoing itself.

Ventuals shut down, freezing those two final numbers in place. But demand for such reference points hasn’t diminished—not one bit.

Pre-IPO Pricing: A Crowded, Increasingly Institutional Field

Demand remains strong—and supply is growing, fast—and becoming more institutionalized.

In the same week Ventuals closed, Coinbase launched its own pre-market perpetual contract—its first underlying: SpaceX—targeting users outside the U.S.

Coinbase isn’t alone. Polymarket built private-company valuation prediction markets using Nasdaq data. Citi rolled out tokenized private company shares for wealth and institutional clients. Crypto-native players are doing it—and legacy investment banks are too.

This is no longer a handful of anonymous teams tinkering on Hyperliquid. Providing real-time, tradable prices for private companies is rapidly evolving into a mainstream, competitive business—one everyone wants a piece of.

For domestic readers, this demand isn’t unfamiliar. IPO lotteries require queuing; primary-market allocations flow only to institutions and high-net-worth individuals—ordinary investors can’t even reach the door. Now, platforms list prices for companies like OpenAI and SpaceX, enabling 24/7 trading. For many, this is the first time they’ve ever accessed such assets. The demand is real.

Yet Ventuals’ shutdown—along with developments over the past six months—has laid bare the fundamental vulnerability of this business.

A price isn’t meaningful just because people trade it. It requires a public, open market where anyone can step in and challenge it—continuously correcting mispricings. Switching from an anonymous team to Coinbase doesn’t magically resolve that flaw. It merely swaps one brand for a larger one—while the underlying company remains unlisted and the fair price remains absent.

Will the next entity tasked with pricing these assets do so more accurately than Ventuals? We may not know the answer until OpenAI actually rings the Nasdaq bell.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News