AI Revenue to Increase 100-Fold in Five Years? Goldman Sachs Draws a $322-Billion Pie for SpaceX’s IPO

TechFlow Selected TechFlow Selected

AI Revenue to Increase 100-Fold in Five Years? Goldman Sachs Draws a $322-Billion Pie for SpaceX’s IPO

Whether Goldman Sachs’ promises will materialize will soon be subject to the market’s first round of judgment.

Author: Claude, TechFlow

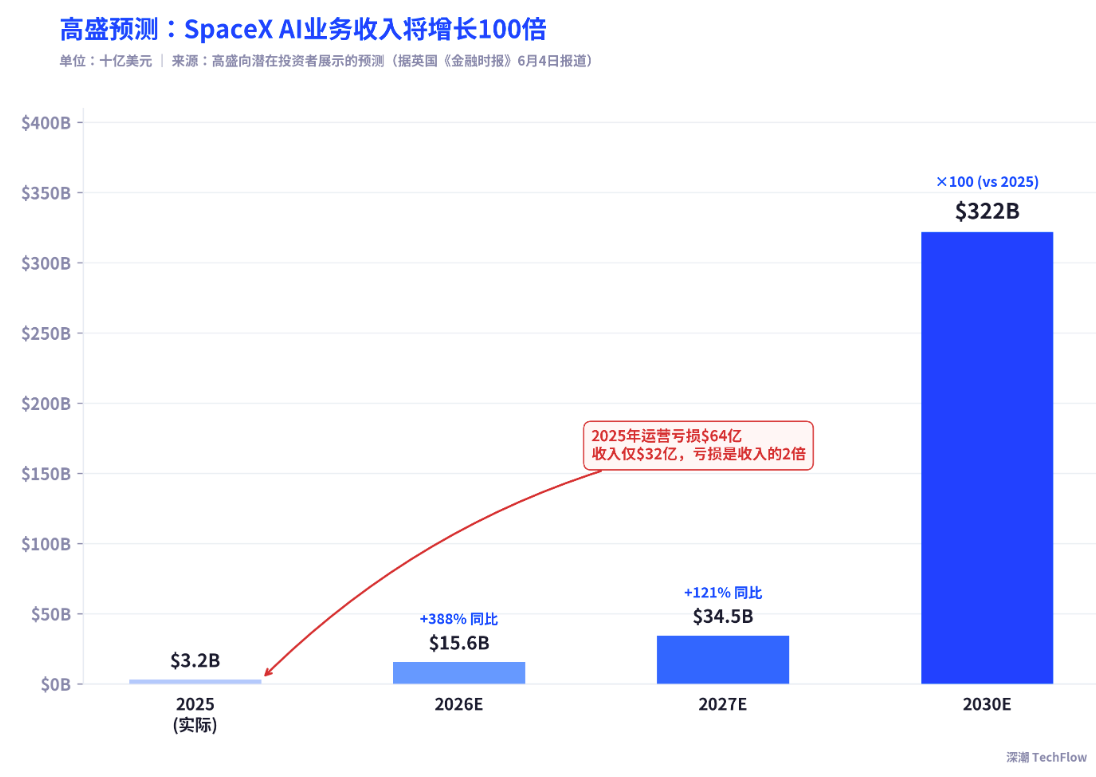

TechFlow Introduction: Goldman Sachs presented potential investors with projections indicating that SpaceX’s AI business revenue will surge from $3.2 billion in 2025 to $322 billion in 2030—a roughly 100-fold increase. These projections come from SpaceX’s lead underwriter for its IPO, even as the AI division is projected to post an operating loss of $6.4 billion in 2025. Meanwhile, Morningstar’s concurrent fair-value estimate stands at just $780 billion—less than half of the IPO’s target valuation.

SpaceX’s IPO roadshow officially launched this week, and Goldman Sachs, acting as lead underwriter, unveiled a set of staggering figures to prospective investors.

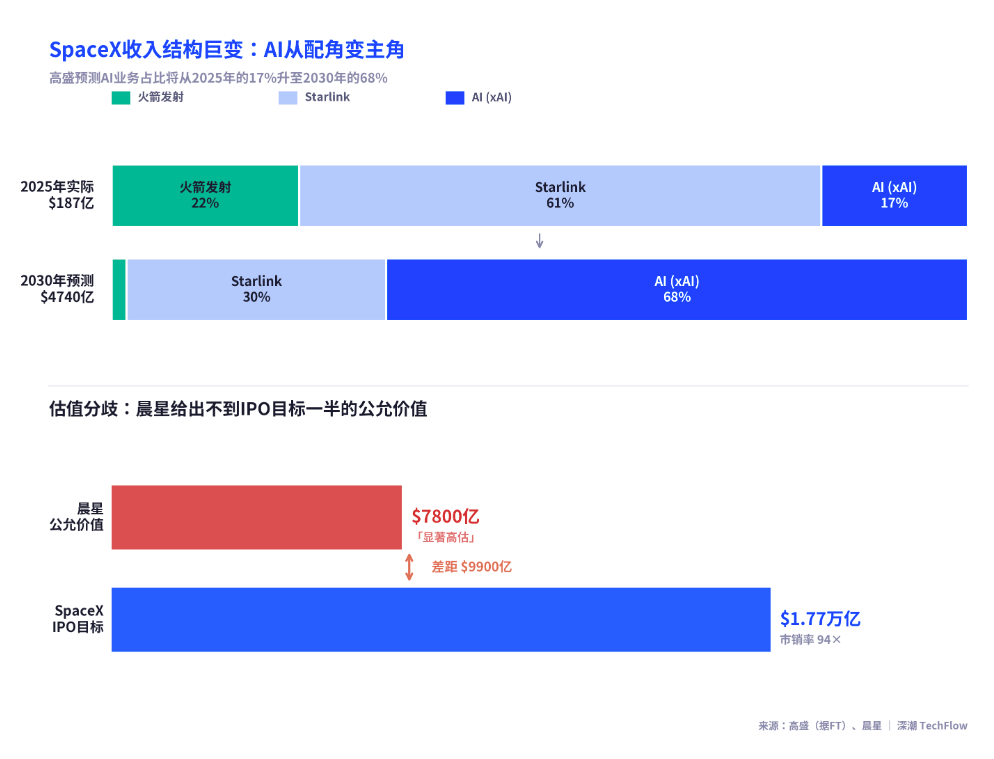

According to a Financial Times report dated June 4, Goldman Sachs forecasts that SpaceX’s AI business—i.e., the merged xAI division—will see revenue climb from $3.2 billion in 2025 to $322 billion in 2030, representing approximately 100-fold growth over five years. Goldman Sachs also projects SpaceX’s total revenue will rise from $18.7 billion in 2025 to $474 billion in 2030. These figures appear in the roadshow materials deliberately: SpaceX plans to list on the Nasdaq on June 12 at an offering price of $135 per share, targeting a $1.77 trillion valuation and raising $75 billion—potentially making it the largest IPO in history.

Yet a key issue arises: Goldman Sachs—the firm issuing these projections—is also the lead underwriter for this transaction. Meanwhile, xAI posted an operating loss of $6.4 billion in 2025 on just $3.2 billion in revenue—meaning its losses were double its revenue.

Goldman Sachs’ Growth Trajectory: From $3.2B to $322B

According to Reuters, citing informed sources, Goldman Sachs expects SpaceX’s AI business revenue to grow 388% year-on-year to $15.6 billion in 2026, reach $34.5 billion in 2027, and hit $322 billion by 2030. If realized, AI would account for 68% of SpaceX’s total 2030 revenue—far surpassing Starlink’s projected $144 billion and launch services’ $8.3 billion.

This implies Goldman Sachs is asking investors to believe that an AI division generating only $3.2 billion in revenue and posting a $6.4 billion loss in 2025 will, within five years, evolve into a business line whose revenue exceeds that of most major global tech giants today. For context, Meta’s full-year 2025 revenue is expected to be approximately $164 billion.

The cornerstone assumption behind Goldman Sachs’ forecast is the large-scale commercialization of AI infrastructure. In SpaceX’s S-1 registration statement, the total addressable market (TAM) for the xAI business is defined as $26.5 trillion—nearly equal to U.S. GDP for fiscal year 2025. This figure is significant not because it reflects a product-level market definition, but because it encompasses “all economic activity that can be replaced or augmented by AI.”

Underwriter Conflict of Interest: Goldman Sachs Is Both Referee and Player

Goldman Sachs’ role in this transaction warrants scrutiny. According to CNBC, Goldman Sachs serves as SpaceX’s lead underwriter, while Morgan Stanley, Bank of America, Citigroup, and JPMorgan Chase are also participating. As lead underwriter, Goldman Sachs’ core responsibility is to help SpaceX complete the offering under optimal terms.

Per FactSet data, based on the $1.77 trillion valuation and $18.7 billion 2025 revenue, SpaceX’s price-to-sales (P/S) ratio stands at approximately 94x. By comparison, the S&P 500’s overall P/S ratio is about 3.38x; Tesla’s P/S ratio stood at roughly 16.73x at the end of 2025. In other words, SpaceX’s valuation is nearly six times that of Tesla—and nearly 28 times that of the S&P 500.

To justify such a valuation, underwriters must convince investors of explosive revenue growth. A “100-fold growth in five years” projection neatly completes that logical loop.

xAI’s Financial Reality: $6.4B Loss, $20B Burn

According to SpaceX’s S-1 filing, the xAI/AI business generated $3.2 billion in revenue in 2025—but posted an operating loss of $6.4 billion. The primary driver of this loss is massive capital expenditure on AI infrastructure: AI-related capex totaled approximately $12.7 billion in 2025, and reached $7.7 billion in Q1 2026 alone—implying an annualized run rate exceeding $30 billion.

On the revenue side, TechCrunch reports that of xAI’s $3.2 billion in 2025 revenue, “AI solutions and infrastructure revenue” amounted to roughly $465 million—including $365 million from X and Grok subscriptions and $88 million from data licensing—while advertising revenue totaled approximately $116 million. The remainder largely came from compute leasing, with Anthropic as its largest customer.

Per SpaceX’s S-1 filing, Anthropic has signed an agreement to pay $1.25 billion per month to lease xAI’s Colossus 1 supercomputing cluster in Memphis—comprising roughly 220,000 NVIDIA GPUs and consuming 300 megawatts—with the contract running through May 2029 and totaling over $40 billion. However, the agreement includes a 90-day termination clause, allowing either party to exit.

On the user-data front, as of March 2026, X platform had approximately 550 million monthly active users, of whom about 117 million used Grok AI features, and roughly 6.3 million subscribed to paid plans—including approximately 4.4 million X Premium subscribers and 1.9 million SuperGrok subscribers. Paid penetration remains below 1% of total X users.

Morningstar’s Reality Check: Fair Value at $780B—Less Than Half the IPO Target

In the same week Goldman Sachs pitched its “AI growth story” to investors, independent research firm Morningstar delivered a starkly different assessment.

According to a CNBC report dated June 3, Morningstar analyst Nicolas Owens estimates SpaceX’s fair value at $780 billion—less than half of the $1.77 trillion IPO target. Morningstar’s discounted cash flow model values SpaceX’s core businesses—launch services and Starlink—at approximately $611 billion, with the AI business contributing only around $17 billion (based on probability-weighted scenario analysis).

Owens stated outright that he does not consider Grok one of today’s leading AI labs, and noted the AI business’s future hinges on unproven technologies such as orbital data centers. Morningstar ran three scenarios for the AI business: under the most optimistic case, AI infrastructure could generate roughly $130 billion in value—but with only a 7% probability; conversely, the “stranded asset” scenario carries a 43% probability and would destroy over $81 billion in value.

Morningstar added that, in the near term, low free-float and a strong underwriter lineup may propel the stock upward—or even cause it to surge—but “long-term investors will have opportunities to buy at significantly wider margins of safety.”

The Core Market Divide: Are You Buying a Rocket Company or an AI Company?

The trillion-dollar valuation gap between Goldman Sachs and Morningstar reflects a fundamental clash of narratives.

Goldman Sachs’ narrative: SpaceX is no longer a rocket company—it is an AI infrastructure company with uniquely scalable orbital deployment capabilities. The S-1 filing reveals SpaceX has applied to launch up to one million satellite-based data center units, with initial deployments slated as early as 2028. If orbital computing becomes reality, SpaceX would possess physical infrastructure advantages no other AI company could replicate.

Morningstar’s narrative: Starlink and launch services constitute SpaceX’s core assets—and they are already fairly valued. The AI business currently suffers heavy losses, exhibits extremely low user monetization, faces intense competition from OpenAI and Anthropic, and relies on orbital data centers whose scientific and economic viability remain highly uncertain.

According to Al Jazeera, SpaceX posted a net loss of $4.9 billion in 2025 and a $4.3 billion net loss in Q1 2026—bringing cumulative losses to $41.3 billion. IG analyst Yip compared SpaceX to Tesla at its 2010 IPO: Tesla was also a loss-making company at listing, and its stock only truly took off after achieving profitability for the first time in 2013. SpaceX investors are placing a similar bet—albeit at several orders of magnitude greater scale.

SpaceX’s roadshow commenced on June 4, with pricing expected on June 11 and Nasdaq listing scheduled for June 12 under the ticker symbol SPCX. Whether Goldman Sachs’ vision materializes will soon be tested by the market’s first verdict.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News