Strategy Records First Net Bitcoin Sale in Four Years—Just 32 BTC Sold as a Trial?

TechFlow Selected TechFlow Selected

Strategy Records First Net Bitcoin Sale in Four Years—Just 32 BTC Sold as a Trial?

Whether this round of selling will again occur “near the bottom” depends on Bitcoin’s subsequent price movement.

Author: TechFlow

On June 1, Strategy—the world’s largest publicly listed Bitcoin holder—filed an 8-K with the U.S. Securities and Exchange Commission (SEC), disclosing that it sold 32 bitcoins between May 26 and May 31 at an average price of approximately $77,135, generating roughly $2.5 million in proceeds. The filing explicitly states that these proceeds “are expected to be used to pay dividends on preferred stock.” This marks Strategy’s first Bitcoin sale since December 2022—and analysts have characterized it as the company’s first-ever standalone disclosure of a net reduction in its Bitcoin holdings. In contrast, its December 2022 sale involved 704 bitcoins but was accompanied by a net purchase of 2,395 bitcoins, resulting in a net increase overall; the nature of this latest transaction is fundamentally different.

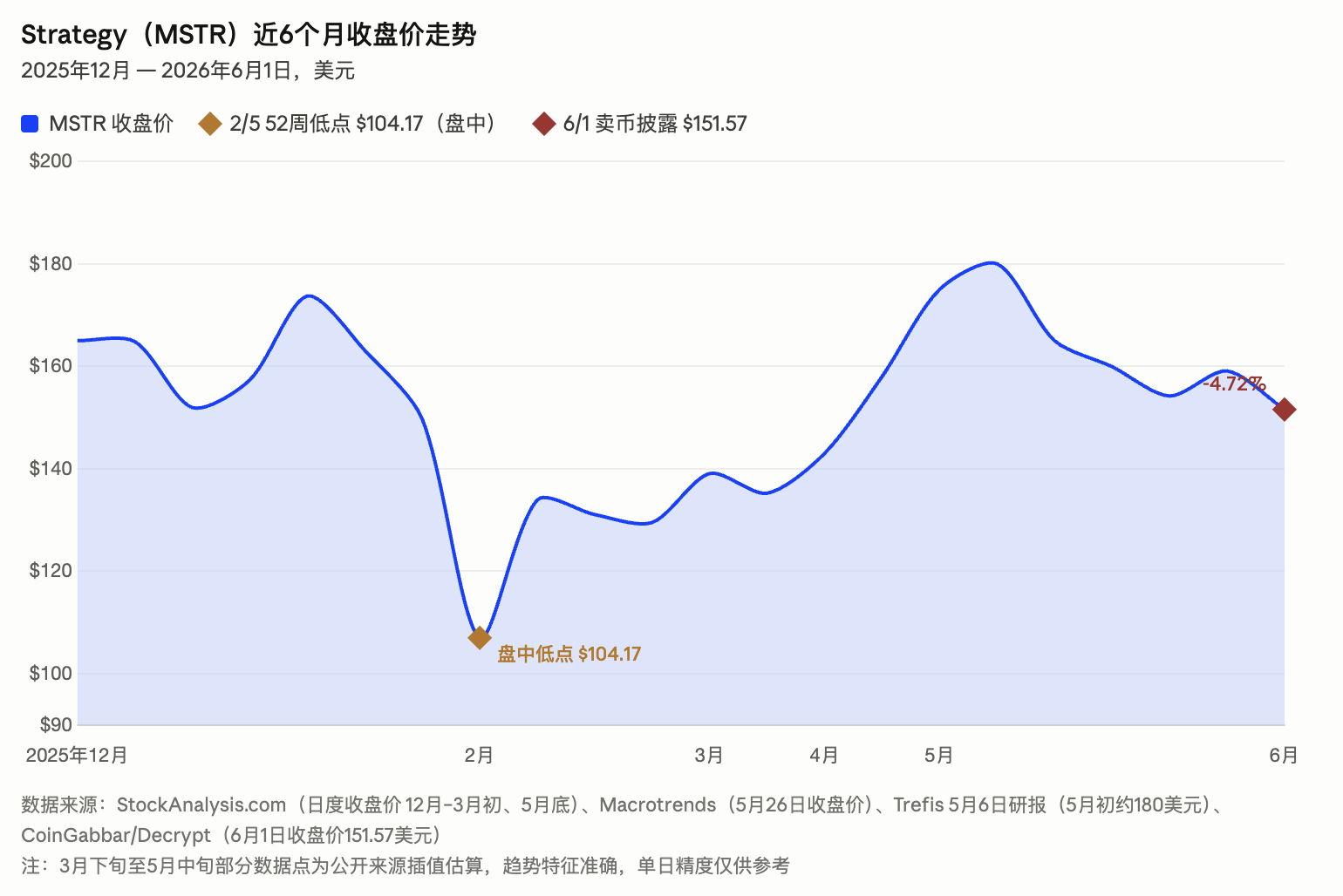

Michael Saylor, Executive Chairman, issued only one public statement that day—a post on X unrelated to the Bitcoin sale: “Our goal is to make $STRC the world’s best credit instrument.” The market reacted far more nervously than this statement suggested. MSTR’s stock price fell 4.72% to $151.57—the lowest level in 45 days—and nearly erased its year-to-date gains. Bitcoin’s price dropped below $72,000, falling roughly 2.77% in a single day. Bitcoin-tracking futures saw over $90 million liquidated within 24 hours, while broader crypto futures liquidations exceeded $600 million.

32 Bitcoins Sold Above Cost; Concurrently Issued 800,000 Shares of Common Stock

In its 8-K filed on June 1, Strategy disclosed that it sold 32 bitcoins in tranches between May 26 and May 31 at an average execution price of approximately $77,135, generating about $2.5 million in proceeds. As of May 31, Strategy still held 843,706 bitcoins, with an average acquisition cost of roughly $75,699. While the sale price remained slightly above its average cost basis, it was approximately 25% below Bitcoin’s early-2026 peak near $97,939.

During the same period, Strategy also sold 801,944 shares of common stock, raising approximately $128.3 million. Part of these proceeds was used to fill the cash shortfall created by its prior discounted repurchase of $1.5 billion in convertible notes. Within this week, Strategy executed three capital-market actions simultaneously—selling Bitcoin, issuing new common shares, and repurchasing convertible notes—effectively reorganizing its capital structure and rebuilding its cash buffer.

Analysts Maintain Target Prices: 32 Bitcoins Are Trivial—but the Market Clearly Disagrees

Since launching its Bitcoin accumulation strategy in August 2020, Saylor has repeatedly pledged publicly to “never sell Bitcoin.” On the evening of May 31—the day the Bitcoin sale concluded—he posted his customary “orange dot chart” on X, a visual signal long interpreted by the market as foreshadowing an upcoming Bitcoin purchase announcement the following week.

No such purchase announcement arrived on June 1. Instead, the market received the SEC’s 8-K filing revealing the Bitcoin sale. Shortly after U.S. equity markets opened, Saylor posted on X: “Our goal is to make $STRC the world’s best credit instrument.” This tweet made no mention of the Bitcoin sale and offered no explanation for Strategy’s first net reduction in Bitcoin holdings in over four years. Neither did Strategy’s official account issue any separate statement clarifying the sale—the entire event materialized solely through the SEC filing. Some investors interpreted this approach as an attempt to “downplay” the significance of the transaction.

Wall Street analysts’ assessments of this sale are highly consistent: from a volume perspective, it is immaterial. Yet the market’s actual reaction was markedly more anxious.

Lance Vitanza, Managing Director at TD Cowen, maintained his “Buy” rating and $400 price target for MSTR. He stated plainly that headlines suggesting Strategy has materially reduced its Bitcoin position are misleading, emphasizing that 32 bitcoins represent just 0.0038% of the company’s total Bitcoin holdings of 843,700. Economically, he noted, the amount is trivial. Vitanza added that TD Cowen’s internal models had already anticipated small-scale, tactical Bitcoin sales and required no adjustment to core assumptions.

Mark Palmer, Managing Director at Benchmark, reached a similar conclusion: “We do not expect Strategy to rely on Bitcoin sales as the primary source of funds to pay dividends on STRC and other perpetual preferred shares.”

The quantity—32 bitcoins—was never the issue. The real concern lies in the underlying cash-flow pressure it reveals.

The $100 Par-Value Threshold for STRC: A Fixed Monthly Cash Commitment of $100 Million

Understanding this Bitcoin sale hinges on Strategy’s STRC (Variable Rate Series A Perpetual Stretch Preferred Stock). This perpetual preferred stock is Strategy’s flagship financing instrument over the past year, with a total size of approximately $10.48 billion and a sustained annual dividend rate of 11.5% for four consecutive months. Based on current scale and rate, monthly dividend payments amount to roughly $100 million—constituting a fixed, recurring cash obligation that Strategy must continuously meet.

The STRC’s structural design directly links Bitcoin purchases to dividend payments: when the STRC’s market price trades above its $100 par value, Strategy can continuously raise capital via its ATM (at-the-market) program, part of which may be deployed to buy Bitcoin; when the STRC’s market price falls below $100 par, Strategy loses the ability to raise new capital through equity issuance and must instead draw upon existing cash reserves to fund dividends.

During the final week of May, the STRC traded below its $100 par value. Strategy currently holds approximately $900 million in USD cash. Following its discounted repurchase of $1.5 billion in face-value convertible notes in May, its cash buffer has noticeably narrowed. Against this backdrop, Strategy’s decision to sell 32 bitcoins to cover the month’s STRC dividend represents a passive fulfillment of a structural cash-flow obligation.

Fundamental Differences From the 2022 Sale—and How Much Buffer Remains

Strategy’s only prior publicly disclosed Bitcoin sale occurred in December 2022, when it sold 704 bitcoins for approximately $11.8 million—but simultaneously net-purchased 2,395 bitcoins, resulting in a net increase in holdings. At the time, the company officially labeled the sale as “tax-loss harvesting,” intended to offset capital gains on other assets; it was not, in essence, a de-risking or de-positioning move.

The key distinction between this sale and the 2022 episode is that this marks Strategy’s first-ever net reduction in Bitcoin holdings disclosed via a standalone 8-K filing—and explicitly designated for funding preferred-stock dividends, rather than for tax optimization. In an early-May interview, Saylor himself remarked that selling some Bitcoin before year-end “is not impossible”—a comment that now appears prescient.

Rajiv Sawhney, Head of International Portfolio Management at Wave Digital Assets, told Sherwood News that the sustainability of the STRC model depends on two factors: investor demand for STRC and the health of Strategy’s “debt-to-Bitcoin” ratio. Citing industry analysis, he noted that the company still retains a buffer of roughly $10–15 billion before reaching an uncomfortable threshold on that ratio—but that “this buffer has been significantly eroded over the past two months.”

CoinDesk observed in its analysis that some market participants have drawn comparisons between this sale and Strategy’s 2022 sale, which occurred near the bottom of the crypto bear market (when Bitcoin traded around $16,800), shortly before the onset of a prolonged bull run. Whether this latest sale again coincides with a “near-bottom” moment will depend on Bitcoin’s subsequent price trajectory. Currently, BTC’s price is about 25% below its early-2026 peak of ~$97,939 and remains nearly 20% above its February low of $59,930.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News