Ethereum Becomes a Chinese Concept Stock

TechFlow Selected TechFlow Selected

Ethereum Becomes a Chinese Concept Stock

ETH and Its Betrayal

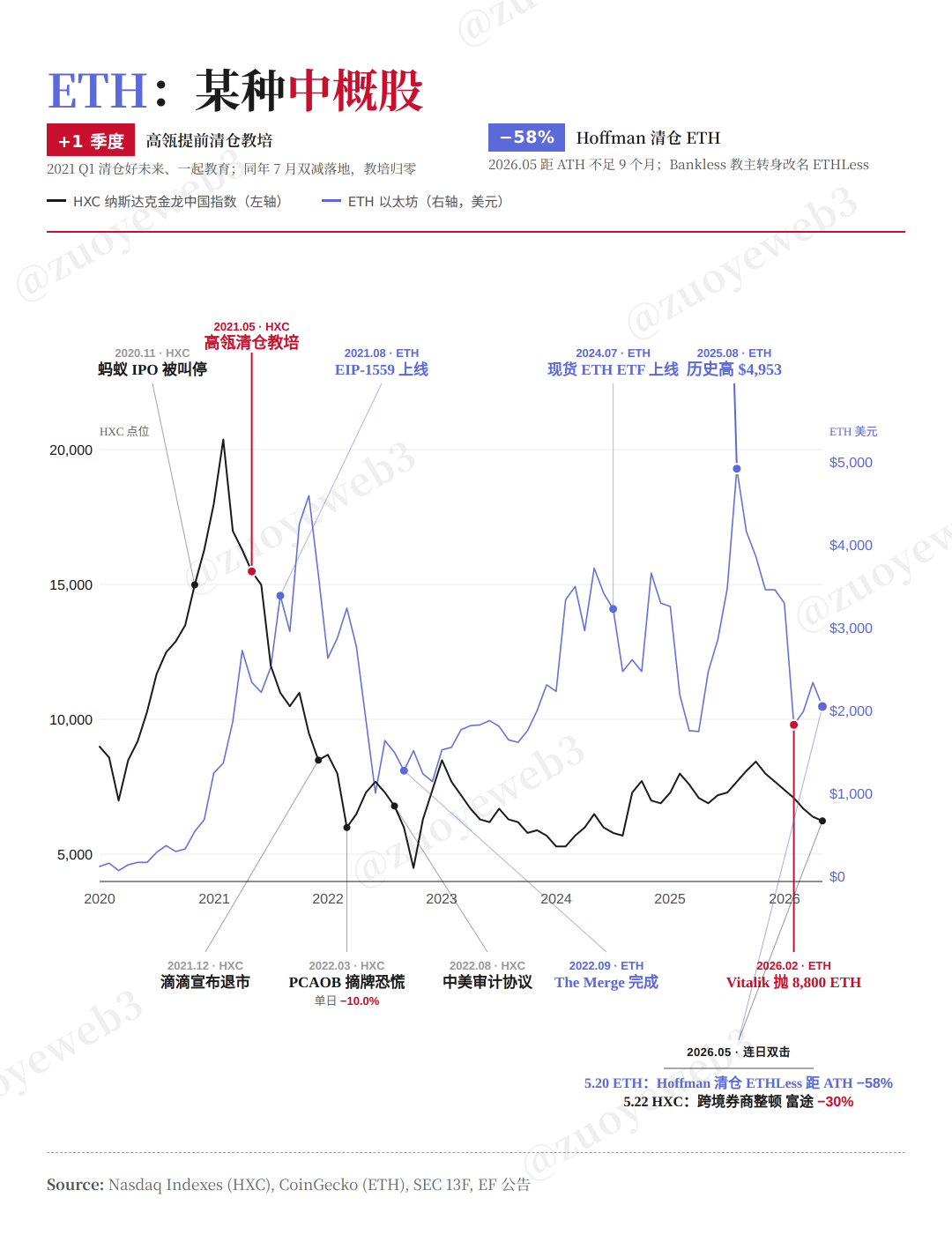

In 2023, Wanxiang, an early Ethereum investment firm, sold ETH multiple times at an average price of $2,047. In May 2026, Bankless co-founder Hoffman liquidated his entire ETH holdings—also at roughly $2,000.

Bankless has essentially functioned as Ethereum’s external communications department, championing the top-tier meme “ETH is Money.” During the 2021 bull market, enthusiasm for ETH was synonymous with unwavering bullishness on blockchain’s future.

Perhaps due to its pivotal role—or perhaps because eight members recently departed the Ethereum Foundation—the Ethereum founder and spiritual leader Vitalik penned a lengthy essay clarifying that the EF (Ethereum Foundation) holds only 0.16% of the total ETH supply and should not enjoy privileged status over other ecosystem participants. He also announced his gradual withdrawal from operational duties, aiming to restore Ethereum’s freedom.

Ethereum Has No Killers

ETH is Money?

Whether you believe it or not—I do.

But how exactly did this vanish? I’m referring to the market’s confidence in $ETH’s price and holders’ trust in both the Ethereum Foundation and Vitalik. Fundamentally, Ethereum is arguably at its strongest point of dominance—but why so much discontent? Is it merely about price?

If $BTC drops sharply, it’s a prime opportunity to accumulate. If $SOL plunges, its post-FTX rebound has already demonstrated its intrinsic value. If $HYPE falls, one can simply trade it tactically alongside Arthur Hayes.

Blaming Vitalik personally is convenient—but abstract founders and foundations abound across public blockchains. Solana’s Anatoly actively inserts himself into Hyperliquid’s community to latch onto the Perp DEX narrative; multiple Ripple founders have dumped $XRP en masse. And in today’s L2 era, founders are generally ego-driven TGE maestros—see Movement’s inner circle.

A closer comparison reveals that while Vitalik may be abstract and the EF possibly “inefficient,” neither bears primary responsibility for ETH’s current predicament. If they’re not the problem, then the broader environment must be.

Caption: ETH is Money?

Image source: @zuoyeweb3

The most illustrative parallel is Chinese internet companies listed overseas (“Chinese概念股” or “China概念股”). Offshore structures + U.S. dollar funds + U.S. IPOs created the wealth-generation miracle of the past two decades. Setting aside early experiments like Brilliance Auto and Chinadotcom, Sina—the first true China概念股—launched the trend in 2000.

Today’s “U.S. concept + China implementation” division of labor is precisely the legacy of that system—even Ethereum itself represents one of the final remnants of this China-to-global trajectory.

In 2014–15, Vitalik first stayed with Shen Bo before securing a $500,000 investment from Wanxiang, led by Xiao Feng. Unlike Bitcoin’s mining-based model, Ethereum’s funding unfolded in three distinct phases: IXO fundraising, PoW mining, and finally PoS staking—carrying three successive waves of participants aboard one vehicle.

Put differently, ETH was institutionally oriented from day one. I don’t mean to suggest ETH is a heavily manipulated token, nor do I dispute Vitalik’s stated desire for the EF to function merely as an ordinary node. Yet Ethereum’s ecosystem has never featured uniformly distributed, equal-status nodes—and never will.

Under such conditions, public-chain founders and foundations inherently shoulder greater responsibilities—unrelated to price. Precisely because Ethereum is fragmented among competing factions, someone must step forward with sufficient authority to curb systemic entropy.

Yet Vitalik chose first to bloat the EF—from the “infinite garden” metaphor to the “Ladder” theory—overly abstract rhetoric leaving token holders disoriented. Especially during the rsETH incident, Aave’s founder Stani effectively assumed the role of Duke Huan of Qi, upholding central authority and repelling chaos.

Even the Solana Foundation set aside past grievances to publicly endorse DeFi United—only to be met with the EF continuing its routine token sales and Vitalik maintaining silence.

Doing too much is centralization—but doing nothing, excessive restraint, is itself an abuse of dominance: deliberate self-suppression presupposes believing oneself critically important.

Thus, Vitalik’s decision to shrink the EF was misguided. The right path would be for him to retreat into “hermit mode,” entrusting the foundation to capable, pragmatic institutions focused squarely on Ethereum’s long-term future.

Beyond Bitcoin, all other public chains face concrete metrics: ecosystem growth and real-world adoption. On these fronts, the Ethereum Foundation holds no special privilege. Market enthusiasm for DeFi and ETH stems less from pure wealth effects than from nostalgic memories of past successes.

Measured by ecosystem vitality and real-world usage, Ethereum’s supposed “killers” have never succeeded. Solana frets over Hyperliquid—but Ethereum doesn’t fret over Solana, just as BTC doesn’t fret over ETH.

Yet this privilege is fading—not from external threats, but internal ones. The real question is: Who bears responsibility for ETH’s price—and who for Ethereum’s direction?

Vitalik is now all-in on privacy—but he shouldn’t “block” others from taking responsibility for price.

New Narratives Await Pricing

Commodity or Productive Money?

Following approval of $rsETH and staking ETFs, DATs like BitMine are rapidly building their own staking infrastructure, while LST players like Lido double down on “productive ETH” narratives—for instance, Spark exclusively accepts Lido’s $wstETH.

Everything is being revalued. Lido isn’t as composed as it claims: with ETH persistently hovering near $2,000, scaling further yields diminishing marginal returns, while APR pressure intensifies—casting shadows even over the productive-narrative thesis.

This underscores price’s importance—or rather, who shoulders responsibility for ETH’s price. Currently, the EF refuses responsibility; Lido cannot assume it; thus, Ethereum’s entire PoS system operates in this awkward limbo.

Returning to the China概念股 analogy: after U.S. markets ceased functioning as viable exit channels, Changxin Storage pivoted to AI; DeepSeek became state-backed; aerospace and robotics concepts oscillate between A- and H-share markets. Love it or not—this is the new narrative architecture.

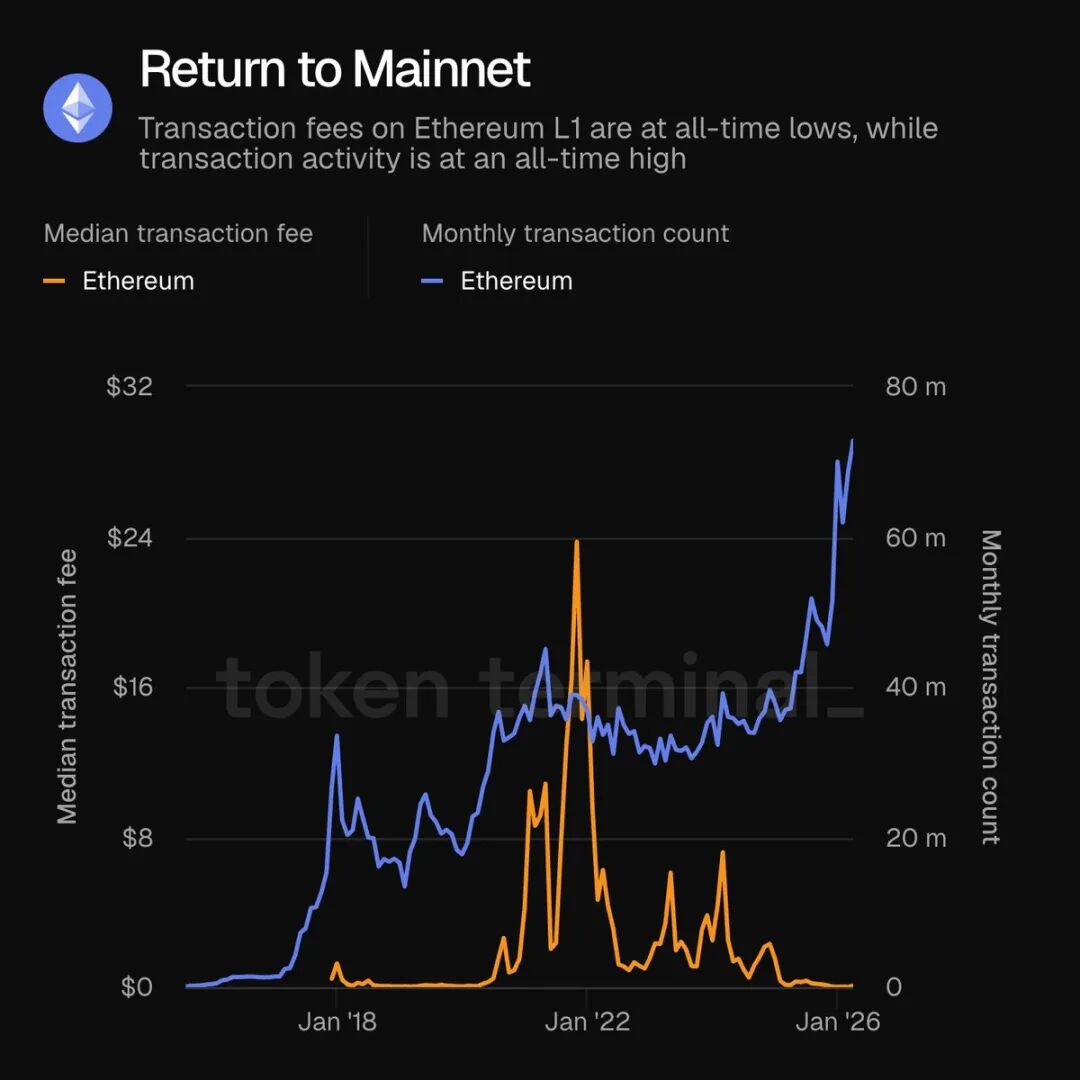

Caption: Return to Mainnet.

Image source: @tokenterminal

After Ethereum’s pivot toward L1-centricity, mainnet activity surged—but you don’t feel ETH’s ecosystem genuinely improving, let alone its price rising. Something is clearly wrong—yet people struggle to define it.

So what are Ethereum’s current technical narratives?

- Privacy: Everything goes ZK—decentralization’s last remaining bastion;

- AI: The dAI team is porting centralized architectures on-chain, emphasizing lightweight on-device models and agent invocation;

- L1: Fully abandoning the L2-centric paradigm—speed and revenue battles return decisively to L1.

Compared to the original “world computer” vision and smart-contract synergy, Ethereum now seeks deeper integration with reality. Beyond those three, stablecoins and RWAs add further layers—but these aren’t Ethereum’s view of the world; they’re the world’s view of Ethereum.

Subject-object inversion—or unclear positioning within the new world—means “everything can go on-chain,” yet blockchain’s heroic, future-facing zeal has faded. Still, we sense blockchain could achieve more—a contradiction, tension, and oscillation that now forms the market’s triple-layered sentiment: people want a better Ethereum, yet doubt such an Ethereum is possible.

After more than a decade of effort, Ethereum hasn’t become the “world computer”—but it *is* an open computer: any activity or idea can be experimented with and executed atop it. While Bankless promoted “ETH is Money,” Vitalik insisted “ETH is Commodity”—a digital product serving concrete functions.

On this point, no one can accuse Vitalik of dishonesty: his February 2026 sale of 8,800 ETH occurred gradually via CowSwap—not like Curve’s founder staking $CRV for stablecoins, nor like Sun Yuchen engineering $USDD to extract retail value.

Yet during the Chiang Mai dialogue in January 2026—imagining a ten-year rewind—when asked whether he’d choose blockchain or AI, Vitalik offered no definitive answer. Reality, however, is clear: more and more crypto-native teams are pivoting to AI, adeptly applying GTM methodologies.

- Hermes Agent broke through to mainstream AI developers; its founding team hails from Nous Research;

- xBubble, developed by DappOS, merges AI with intent-execution frameworks;

- OpenRouter’s founder Alex Atallah previously co-founded OpenSea.

You’ll notice crypto-native teams’ marketing prowess extends far beyond on-chain activity. Even amid the globally dominant AI wave, they consistently keep pace—operating as intermediaries entangled with stablecoins, traffic distribution, and execution layers.

Yet all this bears minimal connection to Ethereum. Though dAI and virtuals jointly proposed ERC-8183 to standardize agent-driven autonomous economic activity, this reflects reactive adaptation—not leadership.

If we treat the present as a narrative “bottoming-out” moment, the core question becomes: What is a public chain’s value in the AI era?

Claude repeatedly disrupts SaaS, security, and external agent frameworks. Imagine a surreal scenario: What if Claude launched its own chain—how would Ethereum respond?

Under PoS, asset migration costs are low—but regulatory compliance still binds Claude to human legal constraints. An unrestricted, experimental financial frontier may remain Ethereum’s most distinctive value.

Just as Mythos’ sharp attacks on Palantir’s stock triggered Qihoo 360’s counter-rally—because striking a rival sparks an arms race across oceans—so too does endless escalation ensue.

Or, in our increasingly polarized world, global connectivity remains a persistent need. Canton belongs to Wall Street—but Ethereum belongs to humanity. Like Saharan villagers without shoes: pessimists exit; optimists rejoice.

But ETH’s golden age won’t return. Wanxiang, the EF, and other institutions will keep selling—but $2,000 ETH is still ten times $200 ETH. We stand at a new starting line. All we need is a compass.

Conclusion

Fatefully similar, ETH truly mirrors the China概念股 trajectory: assets rooted in Country A, funded by Country B’s capital, and exited via Country B’s secondary markets—while Country A contributes only market access and infrastructure.

This is the best of times: fragmentation breeds new markets. Observing Country B’s dynamics, analogous assets in Country A inevitably follow similar cycles. Amid fragmentation, Countries A and B require new connection points—and Ethereum remains the optimal choice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News