BTC Liquidity Plummets 90%; Two Major Market Makers Simultaneously Exit Hyperliquid

TechFlow Selected TechFlow Selected

BTC Liquidity Plummets 90%; Two Major Market Makers Simultaneously Exit Hyperliquid

Hyperliquid Regulatory Storm: On-chain Funds Vote with Their Feet

Author: Claude, TechFlow

TechFlow Intro: On-chain data shows that Wintermute and Auros Global simultaneously withdrew substantial liquidity for major cryptocurrencies—including BTC and ETH—from Hyperliquid on May 18, totaling nearly $100 million.

Auros has fully closed its positions and withdrawn funds to Binance; Wintermute’s BTC+ETH liquidity plummeted by approximately 90%. This withdrawal occurred just three days after CME and ICE jointly pressured U.S. regulators to review Hyperliquid—suggesting market makers’ capital moves may serve as an early indicator of impending regulatory scrutiny.

Hyperliquid is undergoing a rare liquidity withdrawal event.

According to on-chain intelligence platform Hyperinsight, on May 18, two major market makers on Hyperliquid—Wintermute and Auros Global—sharply reduced their liquidity provision for major cryptocurrencies within hours, withdrawing roughly $100 million in aggregate. Multiple independent on-chain analysis accounts have cross-verified these figures via address tracking, with no significant contradictions observed so far.

The timing of this move is highly noteworthy. Just three days earlier, Bloomberg reported that CME Group and Intercontinental Exchange (ICE) were jointly lobbying the U.S. Commodity Futures Trading Commission (CFTC) and members of Congress to impose stricter regulation on Hyperliquid. The market makers’ swift exit could reflect standard compliance risk management—or it may signal the onset of a broader regulatory storm. Markets are watching closely.

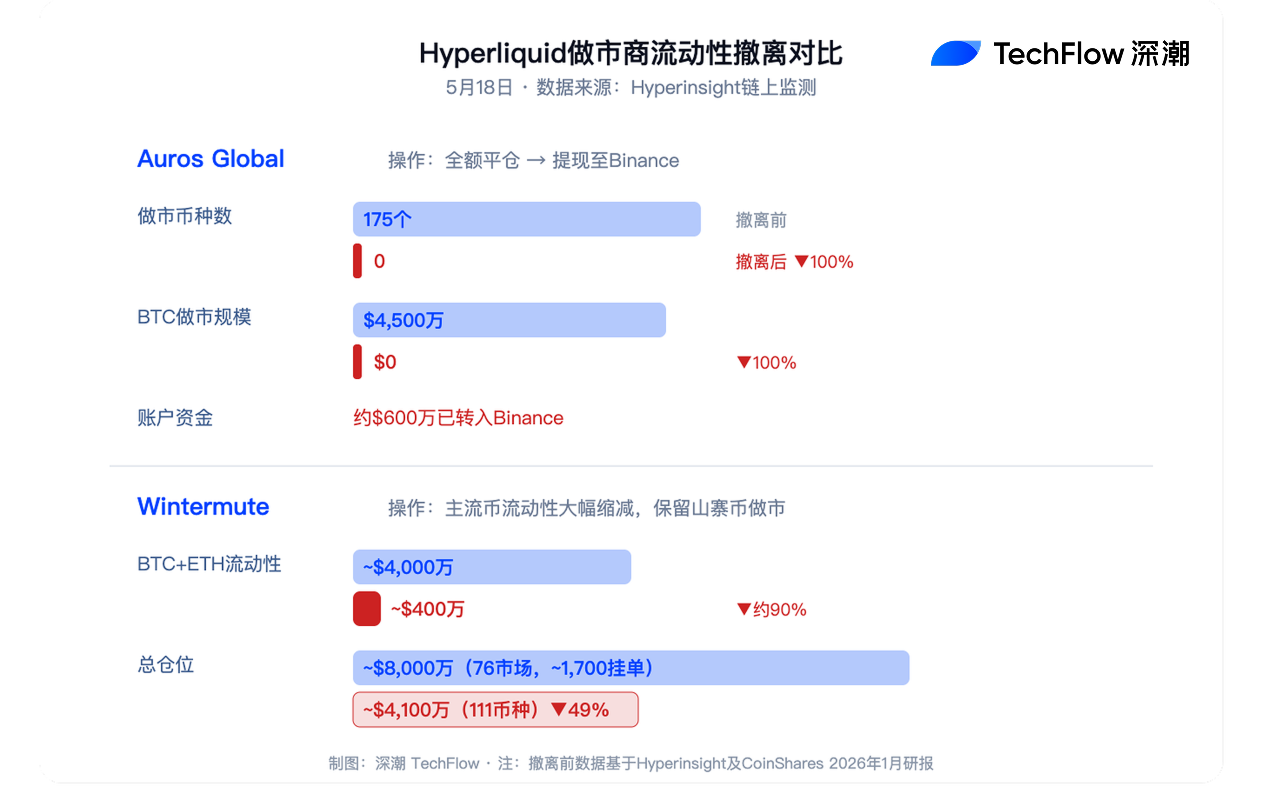

Auros Fully Closed Positions and Withdrew to Binance; Wintermute’s Liquidity Depth for Major Coins Dropped 90%

On-chain data from Hyperinsight reveals markedly different yet synchronized withdrawal paths for the two market makers.

Auros Global (labeled on some on-chain explorers as Oros Global) previously provided liquidity for 175 tokens on Hyperliquid, with its BTC market-making position alone reaching approximately $45 million. As of the morning of May 18, Auros had fully closed all positions, withdrawing around $6 million to Binance. Holdings and withdrawal records associated with these addresses are publicly viewable on HypurrScan.

Wintermute’s actions were comparatively more restrained—but still aggressive. Its combined BTC and ETH liquidity dropped sharply from ~$40 million to ~$4 million—a decline of about 90%; its overall position shrank from nearly $80 million to $41 million. Wintermute continues to maintain open orders across 111 tokens, but order book depth for major cryptocurrencies has notably thinned.

The relevant wallet addresses are:

0xecb63caa47c7c4e77f60f1ce858cf28dc2b82b00

0x023a3d058020fb76cca98f01b3c48c8938a22355

For Hyperliquid—which relies entirely on on-chain order book matching—the synchronized withdrawal by these two major market makers means widened bid-ask spreads and increased slippage for BTC, ETH, and other core trading pairs, significantly raising execution costs for large orders.

CME and ICE Jointly Pressured Regulators Just Three Days Ago—Targeting Hyperliquid’s Oil Perpetuals

The timing of the market makers’ withdrawal closely coincides with an escalating regulatory contest.

On May 15, Bloomberg reported that CME Group and ICE issued warnings to the CFTC and members of Congress, asserting that Hyperliquid’s anonymous trading environment could distort global oil price benchmarks and facilitate market manipulation and sanctions evasion. Both exchanges demanded that Hyperliquid register with the CFTC—a requirement that would compel the platform to implement customer identification procedures and transaction monitoring mechanisms, directly conflicting with its current anonymous trading model.

According to CoinDesk, CME and ICE’s primary concern centers on Hyperliquid’s HIP-3 market. This mechanism enables users to gain synthetic exposure to equities and commodities via on-chain contracts. In March, Hyperliquid’s WTI crude oil perpetual contract recorded over $1.2 billion in 24-hour trading volume during a period of surging traditional-market oil prices—directly challenging traditional exchanges’ pricing authority.

In response, the Hyperliquid Policy Center issued a statement calling these concerns “unfounded” and emphasized that public blockchain transparency actually provides regulators with more effective enforcement tools. According to U.Today, the advocacy group has already met with the CFTC to explore establishing a legal framework enabling compliant participation by U.S. users.

Yet market makers’ decision logic differs from protocol-level PR statements. Both Wintermute and Auros Global are regulated institutional entities; when regulatory uncertainty rises, reducing exposure is standard risk management practice. During the October 2025 flash crash, Jasper De Maere, Wintermute’s desk strategist, told Decrypt that when hedging instruments lose reliability, market makers’ only recourse is to withdraw.

Cerebras’ Pre-IPO Hype Accelerated Wall Street’s Alertness

One catalyst behind the intensifying regulatory pressure is Hyperliquid’s unexpectedly rapid penetration into traditional finance.

On May 14, AI chipmaker Cerebras Systems listed on Nasdaq at an IPO price of $185 per share and opened at $350—up nearly 90%—making it the largest U.S. tech IPO since Uber in 2019. Weeks before listing, Hyperliquid’s Pre-IPO perpetual contracts had already begun pricing CBRS shares; on listing day, its 24-hour trading volume exceeded $280 million.

Arthur Hayes, co-founder of BitMEX, posted on X that he estimated CBRS’s opening price using Hyperliquid’s gray-market contracts. According to U.Today, daily trading volume for Cerebras’ Pre-IPO contracts on Hyperliquid briefly surpassed $230 million—while Nasdaq’s official pre-market trading volume stood at only ~$30 million. Professional traders shared screenshots on social media featuring charts from on-chain DEXs—not traditional trading terminals.

This phenomenon alerted Wall Street that Hyperliquid is no longer merely a crypto-native derivatives exchange—it is encroaching upon the core domain of traditional finance. As of May 2026, Hyperliquid commands 53% of fee revenue in the on-chain derivatives space, with open interest reaching $2.45 billion.

How the Liquidity Gap Evolves Short-Term Depends on Regulatory Timing

Currently, Wintermute continues limited market-making activity on Hyperliquid (across 111 tokens), though liquidity for major cryptocurrencies remains far below prior levels. According to a January 2026 GitHub analysis by 0xLoris, Wintermute previously maintained ~$199 million in total notional value of open orders across 76 markets on Hyperliquid. The current withdrawal implies a dramatic reduction from that figure.

For traders, short-term focus should center on evolving bid-ask spreads and slippage for BTC and ETH perpetual contracts. Hyperliquid’s on-chain order book architecture means market maker withdrawals translate more directly—and immediately—into degraded trading experience than on centralized exchanges.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News