Nearly $200 million in bad debt weighs heavily; several possible scenarios for $AAVE’s future price movement

TechFlow Selected TechFlow Selected

Nearly $200 million in bad debt weighs heavily; several possible scenarios for $AAVE’s future price movement

Short-term rebound is possible, but volatility has not yet ended.

Author: David, TechFlow

Following the Kelp DAO hack, AAVE dropped from $112 to around $90—a 20% decline over 24 hours.

Meanwhile, Aave incurred $195 million in bad debt. Most holders who were long AAVE before the incident—or traders looking to capitalize on this news via derivatives—likely have one pressing question:

Has this 20% drop run its course, or is it just the beginning?

I lean toward believing that a short-term rebound remains likely and volatility has not yet subsided. The current drop reflects market sentiment—the initial pricing-in of the negative impact of the Kelp DAO incident on AAVE.

The variable that will truly determine AAVE’s price trajectory is who ultimately bears responsibility for covering the $195 million bad debt shortfall.

First, let’s quickly recap the sequence of events.

After Kelp was hacked, the attacker minted rsETH out of thin air and used it as collateral to borrow $236 million worth of real WETH from Aave. Once the funds were withdrawn, the collateral became worthless—leaving $195 million in bad debt sitting on Aave’s books.

While DeFi’s nested lending mechanics may appear complex, the core issue here is straightforward:

AAVE was an unintended victim and incurred bad debt; that debt must be covered. If it is covered, the issue is resolved; if not, the situation deteriorates further.

You might ask: What does this have to do with the AAVE token itself?

Can we simply assume that when a protocol loses trust and capital, its token gets dumped and heads toward zero—and conversely, that resolving the negative event restores the token’s price?

Sentiment is indeed a variable—but Aave’s built-in bad-debt absorption mechanism also structurally impacts AAVE’s price.

Three Scenarios That Could Impact Price

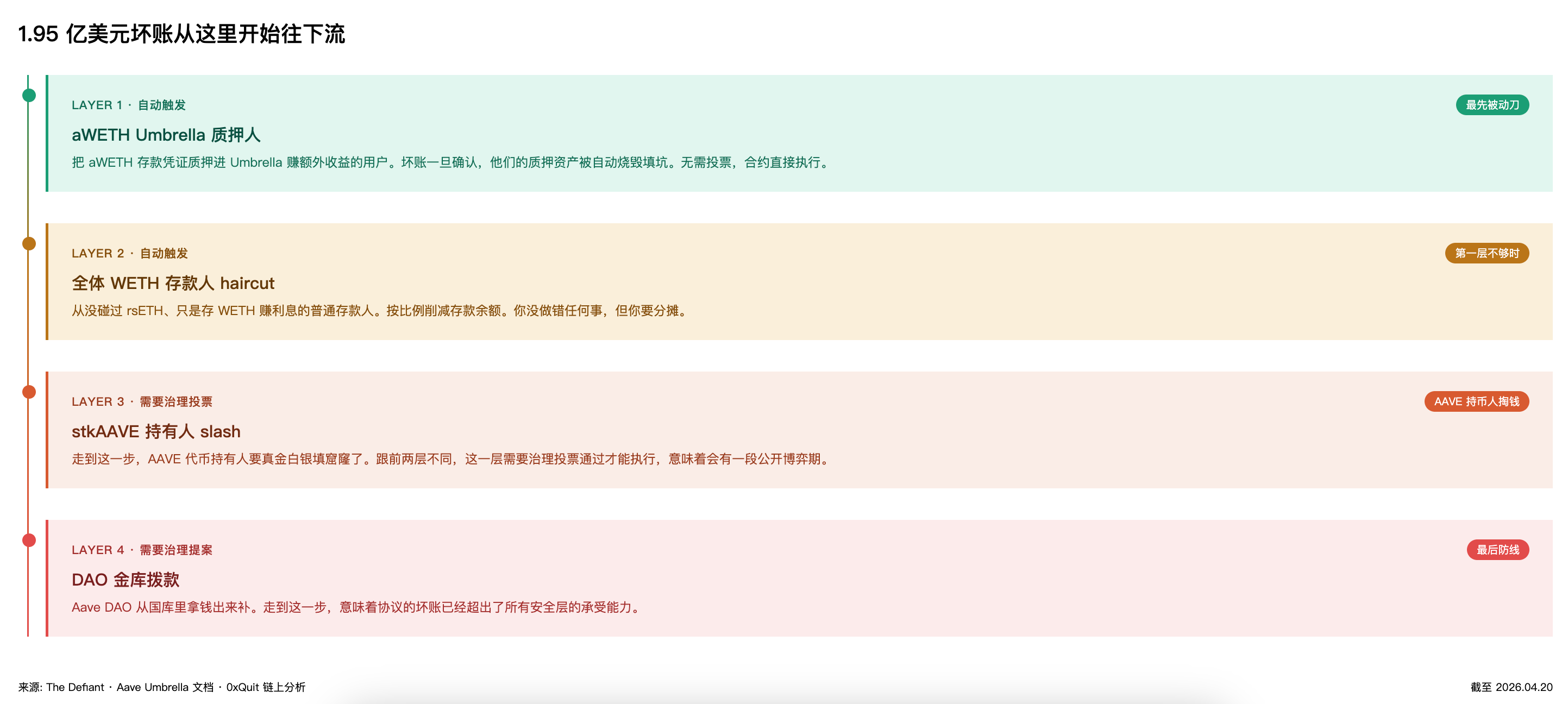

First, Aave employs an “Umbrella” bad-debt absorption mechanism, designed with layered safeguards to minimize losses from bad debt. An AI summary is shown below.

In simple terms, if bad debt exceeds the capacity of earlier layers, the protocol must tap into staked AAVE tokens to cover the shortfall—potentially triggering market sell-offs and thereby influencing AAVE’s price.

Thus, for AAVE holders and news-driven traders, the critical question is: Which layer will absorb the shortfall?

Below are my scenario-based projections.

1. Scenario One: The First Two Layers Absorb the Shortfall — AAVE Holders Bear No Direct Cost

I checked the actual size of the Umbrella staking pool: the aWETH pool holds approximately $55.8 million, while the shortfall stands at $195 million. The first layer covers less than 30%, meaning roughly $140 million will flow into the second layer.

The second layer entails proportional loss-sharing among all WETH depositors.

Although $5.4 billion has already been withdrawn by large players, Aave’s total WETH deposits remain in the multi-billion-dollar range. Covering a $140 million gap would impose a ~2–3% loss on depositors—a relatively small percentage, but deeply unfair to those who merely deposited WETH to earn interest and had no exposure to rsETH.

This is, in my view, the most probable outcome: the first two layers fully absorb the shortfall, and AAVE holders’ principal remains untouched.

That implies no direct financial loss to the AAVE token itself—the 20% drop is purely panic-driven. Once Aave officially confirms that the third layer won’t be triggered, markets should breathe a sigh of relief, opening room for price recovery.

Yet the pace of recovery hinges on whether TVL rebounds. Capital flows out easily—but returning is harder. Re-attracting funds will take time and require Aave to present a credible, verifiable risk-control improvement plan.

So even under the best-case scenario, AAVE’s price recovery will likely be gradual. A short-term rebound is possible, but medium-term performance will depend on whether TVL stabilizes and broader market conditions.

2. Scenario Two: The Shortfall Reaches the Third Layer — AAVE Holders Actually Incur Losses

If the first two layers fail to absorb the shortfall, governance voting kicks in, slashing principal from AAVE stakers.

However, I believe this scenario requires additional negative catalysts to materialize—and is therefore less likely than Scenario One.

For example, if WETH deposits continue draining significantly *before* a formal bad-debt resolution is announced, fewer depositors remain to share the burden, pushing second-layer haircut ratios beyond acceptable thresholds—and forcing the mechanism to escalate further.

Or, if ETH’s price plunges sharply during this window, triggering cascading liquidation failures, the bad debt could swell beyond $195 million.

Should this occur, the nature of the event fundamentally changes.

The market has never witnessed actual slashing of stkAAVE. This risk has historically been priced in only as a theoretical clause—with near-zero weight assigned. Actual execution would force investors to reassess the tail-risk exposure inherent in holding AAVE.

Stakers would demand higher yields to compensate for the newly realized risk—or withdraw entirely, flooding the market with sell-side pressure. Price pressure would far exceed Scenario One, and recovery would take longer, because AAVE’s valuation model itself would shift.

3. Scenario Three: Even the Fourth Layer Fails to Cover the Shortfall

This is highly improbable—but not impossible. It would require multiple concurrent negative developments. Should it happen, market confidence in Aave’s entire security architecture would erode, driving sustained capital flight to competitors and permanently lowering AAVE’s valuation anchor.

Overall, I believe the shortfall will most likely be absorbed within the first two layers. My rationale: although the Umbrella staking pool is only $55.8 million, the WETH deposit pool—despite heavy withdrawals—still dwarfs the remaining $140 million shortfall.

At its current $90 price, AAVE may already reflect overly pessimistic expectations.

What Timeframes Should You Monitor?

Which signals indicate that the worst phase has passed?

I’m personally tracking three key indicators.

The first is Aave’s official bad-debt resolution announcement. Currently, discussion remains at the “exploring options” stage, with no concrete figures. Once released, the market can calculate precisely how much the first layer absorbs, how much the second layer deducts, and whether the third layer—requiring AAVE sales—must be activated.

I expect this announcement to dramatically reduce uncertainty-pricing pressure. It is the single most important catalyst.

The second is TVL stabilization. It need not rebound to Aave’s all-time high of $26.4 billion—only stop declining week-over-week. Stabilizing TVL signals the end of depositor panic withdrawals, halting further deterioration in the protocol’s revenue base, and offering meaningful guidance for the near-to-medium term.

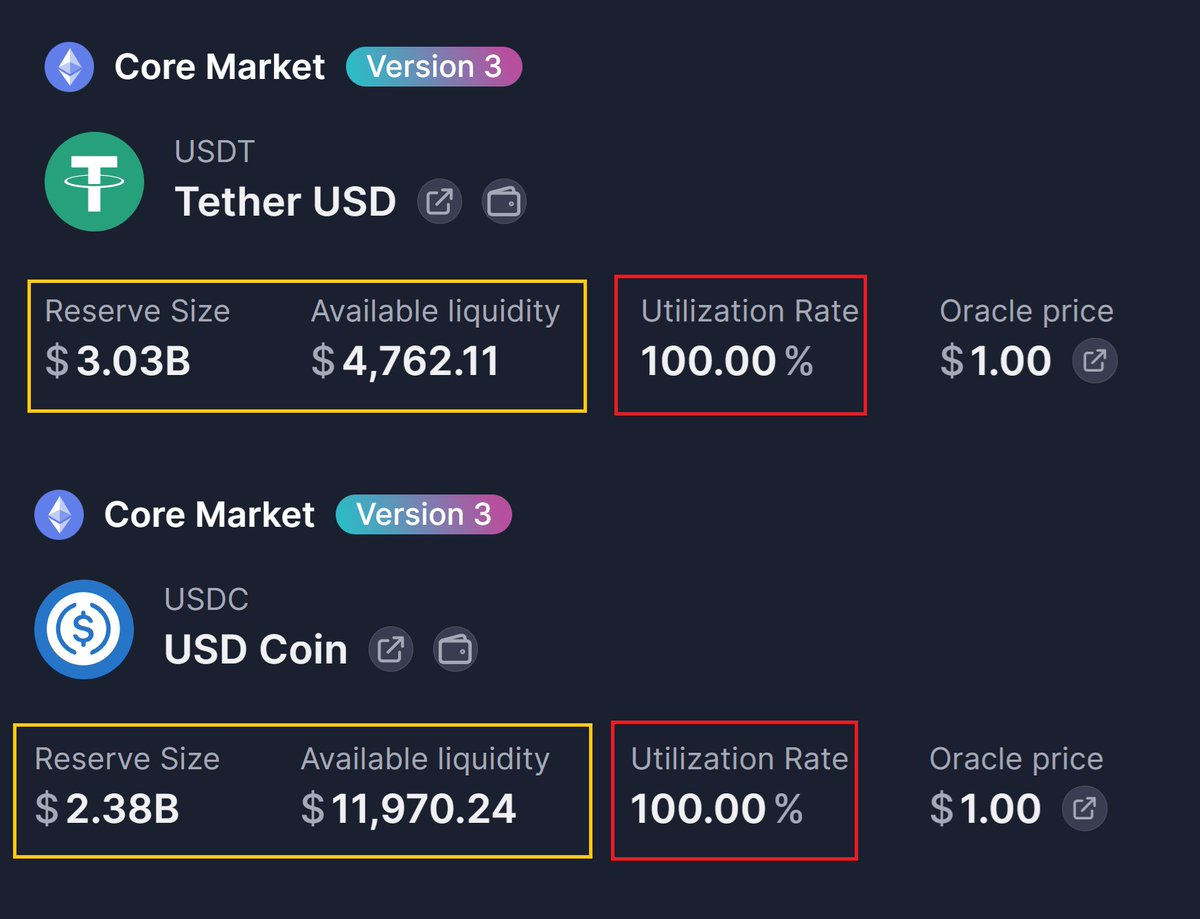

The third is core market utilization returning to normal ranges. Right now, USDT and USDC markets are at 100% utilization—meaning depositors cannot withdraw funds. A return to 60–80% utilization signals recovering liquidity and the substantive end of the bank run.

This metric is visible in real time on Aave’s frontend interface.

If two of these three signals emerge, I consider the worst phase over. Until then, any price rebound should be viewed as technical oversold correction—not a trend reversal.

Returning to the opening question: Has AAVE’s 20% drop priced in enough downside?

My view is that the current price likely incorporates some portion of the “worst-case” scenario—but confirmation of the “best-case” outcome has yet to arrive. During this interim period, price action will likely oscillate.

For those considering buying the dip: I recommend waiting for signals. Only act once you see at least two of the following: the official bad-debt resolution announcement, stabilized TVL, and normalized market utilization. By then, price may have already recovered somewhat from the bottom—but you’ll be acquiring a fundamentally clearer asset, not gambling on speculative “meme-coin” dynamics.

For derivatives traders: volatility will remain extremely high over the coming weeks. Governance voting windows, every official Aave statement, and any sharp ETH price moves will be magnified by the market.

When directional bias is unclear, volatility itself becomes the most reliable trading opportunity.

Finally, one aspect of this incident struck me most deeply: Aave’s smart contract code contained no flaws—yet $195 million in bad debt still occurred. The root cause lay elsewhere: in decisions about which collateral assets to list, their respective loan-to-value ratios, and inter-protocol integrations.

Today’s DeFi ecosystem increasingly resembles Cao Cao’s chained warships at the Battle of Red Cliffs in *Romance of the Three Kingdoms*: protocols are tightly interconnected, so a single “east wind”—a systemic shock—can ignite a chain reaction of failure.

DeFi remains exceedingly difficult for most non-professional retail users. Perhaps this lesson is hardwired into DeFi’s very foundations—and thus difficult to internalize. But the trading opportunities created by such volatility must be maximized.

Note: This article presents mechanism-based reasoning and personal judgment grounded in publicly available data. It does not constitute investment advice. Do your own research (DYOR).

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News