Riding the Wave: A Survival Guide for Top Crypto Traders in 2026

TechFlow Selected TechFlow Selected

Riding the Wave: A Survival Guide for Top Crypto Traders in 2026

This manual is dedicated to everyone building their own trading system.

Author: @MondisCool

This handbook is for reference only and does not constitute investment advice.

Preface: Understanding the Trader’s Survival Principle Through Mathematical Expectation

“The truly skilled warrior wins without earning fame for wisdom or glory for valor.” — The Art of War

The story of “Single-Coin A8” dazzles like fame for wisdom; the story of “all-in reversal” thrills like glory for valor. Yet behind the dazzle and thrill lurk cold bullets of potential loss, quietly waiting. The truly skilled warrior has no illustrious reputation—among traders, those who achieve results are not those who clear the table in one shot, but those who find—and continuously refine—their own trading system amid volatile, ever-changing markets.

This handbook is dedicated to everyone building their own trading system. By deconstructing the careers and mindsets of 14 top-tier traders, our Donut team has distilled the essence of a trading system—and the methodology for building and optimizing it. Market liquidity ebbs and flows; a trading system is the sturdy vessel that carries wealth farther.

A Trading System = Solving a Math Problem

Before discussing “how to build a trading system,” let’s first address “what is a trading system?”

From an outcome perspective, a “trading system” is a methodology for steadily growing managed capital—note the emphasis on *stability*. Every profitable trading system, at its core, solves the same mathematical expectation problem:

A harsh truth: many believe they have a trading system, yet in reality possess only entry-signal judgment—or directional bias—and so on. These elements constitute only part of the final P&L, not a full “system.”

- Why do gamblers at the table eventually lose all their capital? Because the house edge always exceeds the player’s win rate.

- Why can’t “all-in” or “going all-out” be sustained? Because one failure inflicts such high losses that total returns collapse to zero.

- Why does the account shrink even when direction is correctly predicted? Because the profit-loss structure is completely mismatched.

Thus, for anyone seeking to improve trading ability, the critical question is: How can I ensure Σ (Win Rate × Avg. Profit − Loss Rate × Avg. Loss) × Frequency > 0?

- Should frequency be reduced while ensuring each trade has sufficiently high win probability?

- Or should frequency increase while ensuring losses remain fully acceptable?

- If win rate cannot be improved, how can real profitability be increased?

- …

Each trader has their own answer.

No universal, one-size-fits-all trading system exists across markets—but one commonality unites all top traders: they know (even if unstated) where “win rate” and “loss rate” originate, and how to estimate “average profit” and “average loss.” This is precisely what separates elite traders from novices and intermediates.

In summary, a trading system is a complete decision- and execution framework designed to continuously control all variables affecting mathematical expectation—and ensure the account “won’t be wiped out by any single path.”

Although most visible outcomes are profits, for traders the true focus—where time and energy go—is whether they’re consistently executing a positive-expectation system and expanding sample size—that is, prioritizing *process* over *results*.

Specifically, long-term profitable traders share these traits:

(1) Acting only when expected value is clearly positive.

“I’m a trend-focused, heavy-position trader—but I stay flat for extremely long periods. I only enter when I’m certain, targeting only major opportunities. I avoid contracts entirely during ranging markets.” — Heima

(2) Observing and waiting most of the time—not trading.

“New narrative + emergence of a leader token—only when both conditions are met do I deploy large positions. There must be a leader. In 2022, NFT and GameFi narratives drew consensus and capital.” — Qingyun

(3) Risk management is paramount.

“I set take-profit and stop-loss immediately upon entry. Since I sometimes misjudge the market, I always set stops.” — 0xMumu

(4) Avoiding “obvious” opportunities; instead, modeling the next step.

“Potential buy-side: people talking about but not buying / skeptical—this signals latent demand. Potential sell-side: those already holding + publicly bullish—these are likely seeking exit points. If everyone is bullish, it’s time to exit.” — Huanxiong

We’ll detail each trader’s story in the main text.

After reading all traders’ self-narratives, we hope readers’ first reaction to the next “10x in three days” story isn’t envy—but self-inquiry:

- Is this result replicable? Luck—or system?

- If executed identically multiple times, how often would it yield 10x? How often zero?

- What’s the strategy’s capital capacity? Does scaling funds tenfold still leave room for profit?

- What’s the loss if price moves against you?

We hope this becomes the starting point for readers to iterate their own trading systems.

How Trading Systems Form: Identifying Sources of “Certainty”

After conducting long-term interviews with traders across asset classes and styles, we observed a fascinating fact: the path to building a trading system shows striking consistency across individuals.

This consistency doesn’t lie in methodology, tools, or specific strategies—but in the *direction of cognitive updates* and *ways of making trade-offs*.

Nearly all interviewed traders repeatedly emphasize the same thing in different contexts: *know your edge*. Their trading systems are built atop their *actual*, most stable, most reliable source of alpha—not where the market “looks profitable.”

Further, a recurring cognitive leap emerged in our interviews: improving trading ability stems from continual recalibration of *which returns come from market gifts, and which stem from personal insight*.

This means building a trading system is essentially a “de-illusioning” process:

- Exclude偶然 gains from capability assessments.

- Remove non-reproducible luck from the system.

- Preserve only truly personal sources of certainty.

After passing the novice stage, most interviewed traders don’t advance by “learning new strategies.” Rather, the truly difficult—and decisive—phase is persisting with their nascent trading system despite short-term volatility-induced doubt.

This is profoundly counterintuitive:

- The market offers new temptations daily.

- New tools, narratives, and opportunities emerge constantly.

- Yet your task is precisely *not* to follow them.

Hence many traders describe this phase as “enlightenment”: the battle isn’t against the market—but against your own impulse to “do more.”

Another area of strong consensus: every mature trader exercises extreme restraint in judging their own return sources.

In interviews, expressions like these recurred frequently:

- “Not everyone can profit like I do.”

- “This is interesting—but not for me.”

This isn’t conservatism—it’s clarity. We believe the key to advancing a trading system lies not in expanding “what I know,” but in clearly defining “what I *don’t* know.”

The “enlightenment” process truly fights not greed for returns—but greed for cognition. Accepting that you “don’t understand” or “can’t profit from” something is what many traders accomplish moving from novice to intermediate: *active abandonment* of such domains.

This active abandonment means a trading system isn’t predefined and then executed—but continually verified, refined, and ultimately solidified through persistent execution and review.

Traders also use tools in this process—but for them, tools play strictly defined roles: tools assist judgment, helping higher-quality cognition translate into action—not replace cognition itself.

Final Words of the Preface

We must acknowledge: being a Monday-morning quarterback is easy. Predicting what happens next second—or which trading systems will succeed or fail—is infinitely harder.

Yet induction and analysis are indispensable precursors to forecasting. We summarize traders’ experiences and cognitive paths not to offer “guaranteed-win rules,” but to help Donut’s products better serve traders—as their second brain:

- In the past: helping understand yourself and the market.

- In the future: assisting continuous market participation.

Traders race against time—and befriend time.

Donut’s vision is to be the trader’s long-term companion.

[Chapter One] Arbitrage: The Mathematical Machine (9527)

On-chain arbitrage traders are the calmest, least “subjective” group we interviewed. In crypto, they may even be the most archetypal risk-averse participants—since they profit not from market beta, but from alpha arising from microstructural market inefficiencies.

Using our abstract mathematical representation of trading systems, arbitrageurs’ systems are:

- Potential arbitrage profit = spread. Price deviations of the same asset across chains, exchanges, or cross-chain bridges present exploitable opportunities. These require no subjective judgment—only observation and quantification.

- Once a spread opportunity is identified, arbitrageurs move immediately to execution—but first perform one final judgment: estimating success probability. Here, the trader’s subjective agency matters most.

In short, an arbitrage trading system identifies spreads that can be realized, and continuously improves realization probability.

The Story of #9527: From NFT to Binance Alpha Token Arbitrage

“I started with NFT arbitrage—monitoring aggregators and Blur for price discrepancies. Whenever a collection had volume and liquidity, I’d check floor prices and scalp spreads. While doing BAYC, I discovered Apechain and began chain-to-exchange token arbitrage.”

This was #9527’s origin—and the start of his arbitrage trading system. By continuously scanning floor-price differences across NFT markets, he quickly developed acute sensitivity to spread opportunities—buying low and selling high once detected.

“Apechain is obscure—its DEX has no bots, creating easy spreads vs. exchanges. I pre-position tokens and USDC on-chain and on-exchange. Once spreads exceed 0.5%, I simultaneously buy and sell. Sometimes I use lower margins (e.g., 0.3%) to squeeze competitors onto one side—then capture their opposite-side profits if the market reverses.”

From NFT to chain-to-exchange arbitrage, #9527 evolved toward game-theoretic arbitrage.

When competitors execute identical arbitrage, #9527 deliberately uses lower margins (e.g., 0.3%) for faster fills, squeezing rivals’ positions onto one side. If the market reverses, rivals get stuck, and he captures their opposite-side profits.

Note: #9527 had already accumulated initial capital (to support low-margin operations), forecast competitor capabilities, and honed execution skills during his NFT arbitrage phase—making this approach possible. New arbitrage traders should not attempt this strategy directly.

Core Competency: Transferable Arbitrage

“Token arbitrage methodology is nearly identical to NFT arbitrage—even simpler, requiring only understanding cross-chain transfers (i.e., bridges). Bridge knowledge later helped me discover cross-chain arbitrage opportunities in Binance Alpha new tokens.”

“Binance Alpha new tokens launch simultaneously across chains, causing price differences vs. BSC. Their contracts reveal supported chains and bridges—so I monitor for spreads as soon as tokens launch.”

From NFT to Binance Alpha tokens, #9527 migrated not specific tactics—but:

- Spread-discovery ability

- Quick-decision-making ability

- Risk-assessment ability

| NFT Arbitrage → Discover Apechain → Understand On-Chain Spreads ↓ Chain-to-Exchange Token Arbitrage → Understand Cross-Chain Mechanics → Discover Cross-Chain Spreads ↓ Binance Alpha Token Cross-Chain Arbitrage |

“I don’t act on every spread. I instantly calculate approximate odds based on bilateral chain spreads, bridge security, and cross-chain latency. If odds justify it, I trade—within 2 seconds.”

This is arbitrageurs’ core competency: ultra-fast odds calculation. “Alpha new-token arbitrage windows last only 2–3 hours—opportunities vanish instantly.” And increasingly automated arbitrage teams further compress profit margins.

“On-chain data is public—addresses that profit get abandoned. So I insist on reviewing data myself and making my own judgments—to learn which information is useful versus noise. Even if I miss the first bite, experience ensures I catch the second or third.”

A counterintuitive choice: in a field seemingly demanding high automation, #9527 chooses manual trading. Arbitrage windows close instantly; public on-chain addresses invite targeting and mimicry; opponents increasingly deploy deceptive anti-arbitrage tactics (fake spreads, slow-bridge traps, unilateral price manipulation); market understanding deepens only through practice… All these reasons sustain #9527’s manual approach—preserving his learning process.

In this competitive environment, #9527’s win-rate and expected-profit judgments approach muscle memory.

The Arbitrageur’s Fate: Prisoner of Market Efficiency

“Arbitrage spreads are shrinking overall—few play in crypto now; remaining players are too smart—major opportunities rarely appear.”

This reveals arbitrageurs’ fundamental dilemma: the arbitrage paradox.

| 1. Spread exists → attracts arbitrageurs 2. More arbitrageurs → intensified competition 3. Spread shrinks → profit declines 4. Market efficiency rises → arbitrage space vanishes |

#9527 witnessed this full cycle:

2017–2020: Blue Ocean Era

- NFT arbitrage just beginning; almost no on-chain competition

- Large spreads, lasting hours—or even >1 day

2020–2023: Red Ocean Era

- More competitors; ultra-fast execution required to capture opportunities

- Spreads narrowed; windows shortened to hours

2024+: Exhaustion Era

- “Remaining players are too smart”; industrialized quant funds entering

- Spreads razor-thin; windows shortened to minutes

Currently, #9527 is transitioning and exploring further:

- Maintaining awareness of arbitrage opportunities (“I’ll participate if big ones arise”)

- Shifting primary capital to yield farming and discretionary investing—not all-in on arbitrage

Beginner’s Guide to Spread Arbitrage

Tip 1: For traders exploring spread arbitrage, clarify the system’s prerequisites:

- Spread existence → many see only this layer

- Spread duration ≥ trader’s slowest execution path → speed is life-or-death

- Spread covers all friction costs → gas, slippage, cross-chain fees

Tip 2: Sustained arbitrage requires “capability transfer”

- From NFT to token to cross-chain, #9527 transferred not tactics—but spread discovery, rapid decision-making, risk identification, and game-theoretic thinking. These apply across markets and strategies.

Tip 3: Manual vs. automated choice hinges on whichever enhances market cognition

- In a field seemingly demanding automation, #9527 insists on manual trading—because subjective judgment, experience accumulation, and recognition of potential losses are cognitive muscles he must continually strengthen; manual is optimal for him now.

Tip 4: Evolve alongside the market

- Today’s market isn’t arbitrage’s golden age—but new opportunities always emerge. New asset classes and markets birth new arbitrage models and hunters.

[Chapter Two] P-Little General: Liquidity Sensing (Wendy, Ranran)

If arbitrage traders profit from microstructural market inefficiencies, on-chain meme traders profit from liquidity surges and withdrawals.

They hunt on the market’s front lines—monitoring hundreds of newly launched tokens daily, seeking breakout candidates below $3–5M market cap, positioning before the crowd reacts.

Their logic isn’t predicting price movement—but sensing liquidity flow, judging which narratives will resonate, and which tokens will attract capital.

This is a game of “aesthetics and taste,” a bet on liquidity, a survival battle in on-chain trenches.

Two Paths: From VC to Meme, From PvP to System

We interviewed two typical on-chain meme traders: Wendy and Ranran. Their origins differ vastly—but both found survival on-chain.

Wendy: VC’s Fundamental Mindset

“Previously worked in VC—knowledgeable on fundamentals; active on-chain and trade memecoins.”

“On-chain logic resembles VC: invest in 100 projects; one 100x winner funds all others—I’m familiar with this mindset.”

Wendy’s VC background grants her a unique lens:

- Accepts high failure rates (80–90% zero-out)

- Chases extreme reward-risk ratios (10–100x)

- Uses “portfolio thinking” for risk diversification

- Buys extremely early (<$5M market cap)

“Aligns with product logic—exposure builds taste.”

“Identify influential accounts in information streams—e.g., BOME’s artist consistently produces quality work; website aesthetics signal quality.”

Fundamentally, Wendy evaluates memes as “products,” assessing dimensions including:

- Dev background (reputation in Web2/3 communities)

- Aesthetics (website design)

- Narrative (viral potential)

- Hype (attention from influential accounts)

Ranran: PvP DNA × Candlestick Understanding

“I started with PvP—among the earliest Chinese snipers on Solana, even leading groups to profit.”

“I stopped PvP due to age—and because my thrill no longer comes from dunking on others. Mental stability arises from avoiding exhaustion, since PvP becomes unsustainable with age and unprofitable long-term.”

“Wealth accumulation demands a system. Meme markets launch hundreds of tokens daily—this trading deepens candlestick understanding.”

Ranran’s roots are in PvP—the fiercest style, purely speed-based: fastest wins. But he gradually realized PvP wasn’t a sustainable, compounding system—whether regarding time/energy or capital-management scope. Thus, he shifted to a narrative + candlestick trading system:

- First assess narrative (screen promising narrative types)

- Then examine candlesticks (select top 1–3 within the narrative)

- Use candlesticks to time entries/exits

Core Competency: “Aesthetics and Taste”

“If summarizing my biggest progress in meme trading, it’s developing better ‘taste’ for tokens—intuiting quality—resulting from intensive training.” — Wendy

Whether Wendy’s VC thinking or Ranran’s narrative assessment, both stress “aesthetics” as critical for filtering projects—and notably, “information asymmetry” was never mentioned in our interviews.

“Taste” isn’t innate—it’s trained through firsthand exposure to numerous memecoin launches. As Ranran put it:

“Hundreds of tokens launch daily—intensive learning.”

“90% of information aligns with the market—differences lie in judgment.”

“Aesthetics” can be further broken down into three dimensions:

1. Dev Assessment

“For sub-$5M tokens: assess whether devs are actively building. Same people launch and trade—so judge dev strength.” — Ranran

On-chain, dev capability determines whether a project sustains activity (marketing, operations), drives liquidity, and ultimately validates its narrative.

Key dev-assessment actions:

- Monitor key accounts

- Understand dev behavioral patterns

- Capture opportunities between “hints” and “explicit statements”

“Gas Town on Bags: saw 2–3M price anomaly—10% pump. Checked dev—significant Web2 reputation. First article: ‘I’ll look into this coin’ (hint); second: ‘bullish.’ Price surged. I bought shortly after the second article.” — Wendy

2. Narrative Assessment

“How to assess narratives: gauge impact on attention—e.g., White House announcing ‘Lolita Island’ triggers monitoring of peak discussion timing/topics.” — Ranran

“Candlesticks and narratives complement each other. Before identifying good narratives, maintain a knowledge base of hot narratives. Strong narratives attract whales—breakouts occur among 1–3 tokens sharing the same narrative. After narrative assessment, analyze candlesticks.” — Ranran

“Need broader news sources—rarely check Twitter; directly monitor valuable Twitter users. News sources—e.g., currently tracking White House updates—continuously refresh sources to ensure timeliness.” — Ranran

Narrative assessment has two layers: determining if a narrative holds (hot event + high discussion + dev capability), then assessing if capital backs it (using candlesticks to screen liquidity entering specific tokens).

Narrative assessment requires consuming vast news—so for memecoin traders spending time/energy on-chain, the essential trade-off is prioritizing information *quality* over quantity.

3. Candlestick Technicals

“Meme-market candlestick understanding starts from zero—(opponents) gamble, the market is new, players are Gen Z/millennials, passionate, spawning sniper/PvP tactics.” — Ranran

“So opponent behavior is crucial—understanding their dominant trading methods informs candlestick interpretation—e.g., current phase is PvP.” — Ranran

“My candlestick knowledge is solid—I know max loss per trade.” — Ranran

Ranran notes his clear advantage is robust candlestick fundamentals—and intense PvP experience enabled dense training on meme-market candlestick patterns, building pattern-recognition skills.

Converting Aesthetics to Profits Requires Bold Positioning

“What I profit from: money the market fears to bet—subjective, anticipatory.” — Ranran

“90% of information timing matches the market—but I position decisively once convinced.” — Ranran

Both meme traders share consistency: bold entry when others hesitate. This decisiveness isn’t blind gambling—but rooted in loss control:

- Ordinary participants “fear betting” because they don’t know potential loss magnitude—downside risk is unknown. Ranran explicitly states he estimates downside risk before each trade.

- Ordinary participants lack clarity on *why* they profit or lose—while mature-system traders like Ranran feel “market validation of my judgment is most thrilling.”

- Finally, ordinary participants suffer pain from small losses—stop-loss lines blur—while Ranran’s mindset is “trading desensitization:不怕亏 (unafraid of losses)” (but not stubbornly holding losses).

For entry timing, we abstract meme lifecycles into three phases—each requiring distinct judgment:

Phase 1: <$1M Market Cap (Lottery Phase)

“Below $1M market cap, you can bet on dev endorsement—but high zero-out probability—mindset akin to lottery tickets.” — Wendy

Wendy’s approach:

- Small positions (hundreds of USDC) betting on dev background/intent

- Mindset: “Invest in 100; one 100x winner funds all.”

Ranran’s approach:

- Scan chains, inspect trenches—rapid screening

- Mindset: “Shitcoins need no stop-loss—hundreds of USDC is trivial.”

Phase 2: $1–5M Market Cap (Meme Traders’ Sweet Spot)

“Below $3M/$5M, buy at sufficiently low prices—downside risk is limited.” — Wendy

Why sweet spot?

- Limited downside:

- Narrative established, liquidity flowing

- Max loss = 100% (zero-out), but $3–5M market cap lowers zero-out probability to 30–50%

- Massive upside:

- $30M = 6–10x

- $100M = 20–30x

Phase 3: >$30M Market Cap (Warning Zone or Red Line)

“I’m not skilled at chasing highs—nor can I casually deploy hundreds of thousands. So I first check market cap—if above $30M, I ignore it.” — Wendy

For systematic meme traders, large-cap tokens mean:

- Narrowing upside:

- To $100M = 3x

- To $1B = 30x (extremely unlikely)

- Expanding downside:

- Revert to $10M = -66%

- Zero-out = -100%

- Raised psychological barrier:

- Requires larger capital (hundreds of thousands USDC)

- Greater psychological pressure from potential losses

This fails the mathematical expectation test—so they often choose “no action.”

Phase 4: Exit Timing

“Core pain point remains: when to sell. Biggest reflection: GOAT. Bought low, remained bullish, added LP early—but reflection is: don’t add LP to bullish tokens. Later, I sold prematurely.” — Wendy

Even correct entry timing fails if exit timing is wrong—this is Wendy’s current pain point. Her current approach is partial profit-taking; she explicitly notes “take-profit/take-loss needs more information support to combat emotion and enhance discipline.”

For Ranran, his validated system—narrative confirmed, healthy candlesticks—means holding diamond-hand until candlestick patterns signal exit.

State Management: Using AI to Combat Emotion

Ranran mentions using AI for deeper self-understanding:

“Chat more with AI—currently mainly GPT, which feels most self-aware. I share personal and trading info: sleep duration, exercise, etc.” — Ranran

To him, AI isn’t a trader—but a “coach”:

“I reference AI’s trading plans—not specific strategies, but prompts guiding self-questioning: ‘Am I fit to trade now?’ etc.” — Ranran

“Great traders follow plans—not emotions—executing like machines. If my mental state doesn’t support trading, I skip emotional stop-loss or skip trading entirely.” — Ranran

“Recently using clawdbot, integrating GMGN’s API for automation—still debugging, feasibility confirmed. Friends are doing this too; some successfully integrated APIs but haven’t profited yet—all still suffering.” — Ranran

Beginner’s Guide to Memecoin Trading

Tip 1: Taste Is Trained—Not Innate. How?

Method 1: Scan Extensively

- Daily scan dozens to hundreds of new launches + 4–5 large caps emerging from liquidity-rich venues like Solana—observe what succeeds vs. zero-outs

Method 2: Real-Money Testing

- Test with small sums (hundreds USDC)—experience real P&L, building intuitive frameworks

“Started meme trading by funding myself—no observation of others—requires real-money commitment.” — Wendy

Method 3: Review

- Log every trade: Why buy? Why sell? Which judgments were right/wrong?

“Understanding oneself requires review.” — Ranran

Tip 2: Strictly Control Downside Risk

- For Wendy and Ranran, ideal FDV ($3M/$5M) and red-line FDV ($30M) are ingrained muscle-memory disciplines.

Tip 3: Confirm Narrative Viability First—Then Use Candlesticks to Select Tokens

“Candlesticks and narratives complement each other. Strong narratives attract whales—breakouts occur among 1–3 tokens sharing the same narrative. After narrative assessment, analyze candlesticks.” — Ranran

Tip 4: Small Positions Need No Stop-Loss—Large Positions Require Reward-Risk Calculation

“Shitcoins need no stop-loss—hundreds USDC is trivial. Above $20,000 USDC is on-chain large position—reward-risk ratio must be calculated pre-entry.” — Ranran

[Chapter Three] Value Investing: Long-Term Heavy Positions & Buidl (Huanxiong)

In one sentence: value investors profit from liquidity concentration during major trends.

They’re traders seeking value signals amid market noise—not chasing every wave, actively avoiding short-term contracts. Their alpha stems from identifying major trends, deploying heavy positions, and holding firm.

Value investing is a research arena, a “vision” game, a patient gold-rush through public information.

Investment Narrative Framework

We interviewed a classic value investor: Huanxiong. His core thesis: value emerges from trend-driven liquidity concentration.

Huanxiong: Following Narratives

“Started on Binance in 2019—initially followed Telegram, not Twitter.”

“DeFi Summer ended 2020—many great projects emerged, e.g., dydx, GMX. I received an airdrop from a DeFi project, then explored BSC yield farming.”

“First major non-airdrop win: a Perp DEX—I bought its token at very low market cap (a few million), later expanded across chains, rapidly increasing market cap.”

“Around 2023, new trading tools emerged—I used them, dabbled in memecoins—but didn’t profit much.”

“Later returned to airdrops—accompanying projects’ growth remains my comfort zone. Continuing as a DeFi yield farmer—this offers deterministic returns.”

Huanxiong’s path typifies “project-accompaniment”: discovering promising projects extremely early, holding long-term until exchange listing.

“I don’t watch candlesticks—I don’t stay up late.”

“Narrative assessment: count how many ‘narrative-savvy’ people discuss it—long-term vs. short-term—and assess potential buy-side.”

Huanxiong’s self-definition is precise: narrative trader. His core competency isn’t technical analysis—but judging narratives and people.

- How many “narrative-literate” people discuss it?

- Are they long-term or short-term players?

- Are there signs of “crowding” in the token?

Through prolonged market participation, he developed a unique “buy/sell-side” analytical framework supporting narrative-entry timing:

Potential Buy-Side Signals:

- Many talk but don’t buy—even skeptical—these are latent buyers, having “noticed but not boarded.”

Potential Sell-Side Signals:

- Already holding the asset and publicly bullish—likely seeking profit-taking exits, thus latent sellers.

“If the entire market is bullish, it’s time to exit.”

Core Competency: “Riding Trends” Based on Public Information

Huanxiong’s “buy/sell-side framework” further means: assessing whether value-generation logic holds—and when the market will “buy in.”

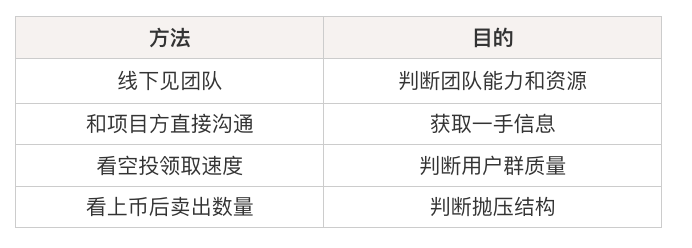

Information Sources: Deep-Dive Mining

Huanxiong’s narrative emphasizes exhausting information—especially first-hand/original sources—as the foundation for credible judgments.

“Starting 2020, I aggressively contacted founders—DMing/calling daily. Though I had only 2,000–3,000 followers, founders engaged willingly.”

“Conversations revealed quality—if 5–6 founders praised a project, the sector is promising—so accompany smaller projects’ growth.”

His observational angles include:

Contrasting Further to Understand Value Investing:

- Meme Profits Rely on “Speed”:

“Memes profit via speed—entry speed includes information and execution velocity.”

“Some meme narratives are merely adequate—not excellent—but fast entry yields profit. Excellent narratives with slow entry still lose.”

- Narrative Investing Profits Rely on “Vision”:

“Buying below $10M market cap tests vision—not timing.”

Why Huanxiong Chooses Narratives Over Memes?

“My information and execution speeds are slow—I can’t join WeChat groups; can’t instantly scroll all info.”

“Still uncomfortable with many on-chain monitoring tools.”

His advantage lies in high subjective initiative in information gathering—and direct human judgment—granting multidimensional verification capabilities: his “vision.”

Lifestyle as Strategy: Steady and Balanced

Huanxiong’s position allocation reflects strict layering:

- Narrative positions: New narratives typically use only 1–2% of capital—observing directional validity; holdings rarely exceed 1–2% FDV—otherwise becoming “project employees.”

- DeFi farming: Pursues stable returns (~20% APY); holds long-term if security confirmed.

- Strict separation prevents narrative volatility from undermining stable-return positions.

“Every strategy has capacity—small capital accesses lower-capacity strategies. E.g., Polymarket arbitrage fits only $10K–$20K USDC—not $100K+.”

“My main funds are in banks, medium in DeFi, small in memes for fun.”

Tool Pros/Cons: Core Purpose Is Judgment Support

Huanxiong’s Tool Philosophy: Accuracy > Comprehensiveness

“Don’t prioritize data comprehensiveness—mainly need basic data.”

“Don’t need platforms to analyze—e.g., guessing wallet owners or labeling Jump as market maker. Inaccurate info misleads. I prioritize accuracy over comprehensiveness.”

Common tools:

Beginner’s Guide to Value Investing

Huanxiong advises explorers of trading styles:

Tip 1: Be Frugal During Exploration: Priority is maintaining the mindset and ability to keep experimenting (even failing)—test with small sums, scale up after profiting.

“Still exploring? Be frugal—hundreds suffice; don’t spend thousands. Profit first, then scale.”

“Don’t disrupt life—play until you develop a system. Don’t test your system with large capital.”

Tip 2: Understand Strategy Capacity

“Every strategy has capacity—small capital accesses lower-capacity strategies.”

- Another benefit of small capital: accessing low-capacity strategies (e.g., arbitrage) allows more system experimentation—potentially finding the right fit faster.

- Long-term, every investment strategy requires clear capital upper limits—don’t mismatch capital with strategy.

Tip 3: Account for Uncertainty in Time and Realization Pace

“Participated in some trades that never materialized—positions zeroed out.”

- For aspiring traders: confirm pre-entry your ability (psychological and financial) to endure long realization cycles and potential zero-out risks.

[Chapter Four] Rule Arbitrage & Primary Opportunity Capture (Feng Wuxiang, Huashui Champion)

Though similarly labeled “arbitrage” as on-chain spread arbitrage, rule arbitrageurs don’t chase short-term structural inefficiencies—but grasp the essence of “rules” and their payoff expectations upon fulfillment.

Rule arbitrageurs don’t bet on direction or narrative upside—they bet events *will* happen: airdrops *will* distribute, TGEs *will* occur, fixed-income contracts *will* settle. Once this “certainty” holds, they convert uncertainty into calculable expected returns.

They’re researchers pushed to extremes—using sector forecasting to screen opportunities, cost control to raise error tolerance, and scalable execution to amplify returns. They aren’t fastest or best-informed—but most deeply researched on rules.

This is a research path turning “opportunities” into “businesses.”

Scalable Studios vs. Refined Individuals

Feng Wuxiang and Huashui Champion are two rule arbitrageurs we interviewed. One industrializes rule arbitrage; the other refines it systemically. Though methodologies differ, their underlying logic is highly consistent: betting solely on *certain* profitability within a time window—not trend forecasts alone.

Feng Wuxiang: Scalable Research-Driven Airdrop Hunter

“Started monetizing via studio—mostly on-chain trading. Began IDO on CoinList in 2021.”

“Bought KYC accounts en masse from Southeast Asia/Africa. Paid $10K for two people—$15–$20 per KYC account—maintaining 800–1,000 accounts. 2% win rate—$500+ per account; $10K+ per project. Post-allocation, projects were near-guaranteed profit—returning $40K–$50K, even $100K+.”

“That era offered tailwinds—I entered with hundreds of thousands, earned $10M profit in a year. This ‘mindless’ capital rotation was rare then—few thought to industrialize IDOs.”

Feng Wuxiang’s rule arbitrage origin was CoinList’s 2021 IDO boom. Solana, Flow, and other “king-tier” projects launched on CoinList—participating guaranteed returns. He turned “airdrop farming” into industrial production: sourcing scalable accounts, assembly-line execution—every step yielding calculable expected returns.

Of course, market mechanics ensure arbitrage spaces don’t persist—more participants quickly flooded IDO farming, further compressing returns. Feeling returns decline, Feng Wuxiang promptly shifted focus from IDO platforms to forecasting which new crypto sectors would emerge. In 2023, Hyperliquid’s launch—driving massive market attention via generous airdrops—highlighted Perp DEX as an unrecognized mainstream sector. At that moment, Feng Wuxiang targeted Perp’s “dragon-two” project.

“Initially, few believed in Perp—until Hyperliquid launched, signaling the entire Perp market would rise. If dragon-one hits $40B, dragon-two could reach ~20% FDV—Lighter entered my view.”

Huashui Champion: Lean Rule Arbitrage

“Started with Ethereum ecosystem’s major airdrops—around 2022–2023. For ARB, tiered accounts—cost ~$200 per account. Top-tier accounts yielded ~$20,000; junk accounts ~$1,000. Post-airdrop, I split proceeds half ETH, half USDC.”

“AltLayer used OG NFTs—bought for 0.x ETH—top-tier airdrops reached $100,000 USDC.”

“StarkNet also tiered accounts—top-tier airdrops ~$10,000 USDC. Left $3,000–$5,000 USDC in accounts, held 3–6 months—burned >200 USDC gas—earned 10,000 STRK. To recoup gas, weekly rebalanced stablecoin APR on Ekubo—good on-chain data meant accounts earned thousands of STRK.”

“Turning point: post-Hyperliquid—I largely stopped airdrops, shifting to YT.”

Huashui’s origin was Ethereum ecosystem’s major airdrop boom. From airdrops to YT strategies, he stresses not rushing into narratives/directions—but confirming TGE/settlement events *will* occur before positioning. This “rule fulfillment + cost accounting” approach, forged during airdrops, later extended to YT.

Core Competency: Research + Accounting

Whether Feng Wuxiang’s sector forecasting or Huashui’s profit estimation, both do the same: quantify all calculable expected returns—judging by numbers, not feeling.

Research Competency: Immersive Market Observation

Feng Wuxiang’s research logic:

“I conduct my own research—profits come from knowledge gaps and execution. Markets reacted slowly before—but now react fast, with smarter participants.”

“High research ability stems from reviewing enough projects—forming independent sector judgments. Seeing more enables earlier identification of breakout sectors—dragon-one’s success implies dragon-two’s potential.”

“Compared to peer studios, we faster implement info-to-execution—e.g., one call with top studios yields full airdrop-rule-to-strategy blueprints.”

Huashui’s research logic:

“Early ‘ancient’ airdrop farming and project cold starts taught blockchain browser usage—more useful than 90% paid groups. Check recent gas burn leaders to identify hot categories.”

“Now in early bear market, environments changed drastically—previously useful tools (e.g., browsers) no longer apply. Now assess: as retail, what’s the project’s chip-distribution behavior toward you—and how does it affect your chips’ value?”

“I always assume information disadvantage. Never think I’m fastest or smartest—or smarter than founders. So default: I’m slower than founders, slower than insiders, external capital. Thus, I avoid earliest, most extreme, or last-bid bets—I wait for info to shift from ‘fuzzy’ to ‘certain,’ even accepting less profit.”

Accounting 1: Cost Control

Feng Wuxiang’s cost mindset:

“Low enough cost—e.g., Lighter points average $3—bans still profit.”

“Being a KOL enables earlier founder contact—access to info, allocations, better rebate plans—lowering costs, building cost advantages.”

“Diversify to control risk/cost—allocate 2–3% per project, ≤$500K total cost.”

Huashui’s cost mindset:

“YT’s real cost is consumed USDC—the actual money invested.”

“Last year, most non-TGE YTs lost—but tiny purchases for testing caused no harm.”

Accounting 2: Profit Space Within Rules

Feng Wuxiang’s profit estimation:

“Pure early-stage may lack advantage: point inflation, founder betrayal, project death. Over-allocating invites ganking; Perp DEX witch rules are arbitrary.”

“If dragon-one hits $40B, dragon-two could reach ~20% FDV. Kraken’s data and Backpack’s are similar—but Kraken’s pre-TGE valuation is $15B, actually worse than Backpack.”

Huashui’s profit estimation:

“Falcon initially signed 10% APR fixed-income contracts—pre-TGE timing estimated end-of-year; delay meant decay. Bullish sentiment existed—so reverse-calculated TVL→APR→reasonable FDV. Pendle YT ~8% served as benchmark. Calculated Falcon YT purchase ≈ <$100M FDV—bought first tranche.”

Beginner’s Guide to Rule Arbitrage

As crypto participation grows and accessible intelligence rises, rule arbitrage difficulty increases. Both traders clarified the sector’s intensifying competition. For beginners, they offer these tips:

Feng Wuxiang’s Tips

Tip 1: Prioritize Research & Thinking Ability

“Ask: what abilities won’t be replaced by tools? Strengthen those—e.g., research and thinking—not coding.”

“Opportunities/year: 3–5—must capture ≥1.”

Tip 2: Selection > Execution

“Selection matters more than execution—execution capabilities are now similar; selection and timing are paramount.”

Tip 3: Recognize Tool Limits

“Top tools were quant funds; ordinary tools were sticks. Vibe-coding offered ‘rice-and-vegetable rifles’—but now everyone has them, so they’re just sticks.”

Huashui’s Tips

Tip 1: Only Engage Largest Projects

“Only largest projects are safest. Small projects offer high returns—but risk-unfriendly for beginners.”

“Judging large projects is subjective—focus on narrative, VC backgrounds, and competitiveness.”

Tip 2: Small Capital for High Odds—Large Capital for Stability

“Seek high returns? Small capital buys memes. Never use large capital for memes.”

“Airdrop farming and shitcoin hunting resemble each other. Early stages: observe with $100–$1,000—losses harmless. When momentum builds, chase higher.”

Tip 3: Think Like Project Founders

“In today’s market, a key project evaluation criterion is your participation cost—e.g., others pay $1, you pay $0.1—your safety margin widens. Test strategies via small payments—estimate FDV acquisition points, maximize safety buffers. Also, think from your opponent’s (founders’) perspective—monitor founder/official Twitter for hints of breach.”

From our interviews, further distilled rule arbitrage insights: though this approach relies on “certainty” suggesting higher win rates, seeing a good opportunity doesn’t mean blindly entering.

In fact, both traders repeatedly stressed cost control and position structuring. Feng Wuxiang lowers costs via KOL status; Huashui controls risk via small positions. We suspect this stems from arbitrage’s inherently high risk-aversion—requiring explicit downside controls in execution.

[Chapter Five] Technical Indicators: Dancing With Volatility (0xMumu, Yu Ren, Qingyun, Jex, Heima)

After covering value investing and rule arbitrage—two “slow-is-fast” approaches—this chapter interviews five traders whose methods starkly contrast: 0xMumu, Qingyun, Yu Ren, Jex, and Heima.

To them, technical indicators—or price—are paramount, as all market information (sentiment, capital, expectations) ultimately consolidates into this singular “report card.”

Despite shared technical foundations, these five exhibit diverse cross-verification methodologies: some monitor liquidations and extreme-volatility windows; others validate divergence gaps using sentiment premiums and contract structures; some confirm trends via leader diffusion and OI/order-flow; others revert to simple moving averages or naked candlesticks. Thus, some appear narrative-trading-like—but fundamentally, all multi-dimensional inputs anchor to price.

Trading History & Profit Sources: Evolution Paths of “Technical Traders”

0xMumu: From Luck to Systematic Short-Term Trading

“I encountered BTC in 2017 during university—no system, just random playing: DeFi mining, etc. Profited due to overall market rallies.”

“DeFi mining required contracts for hedging—so I learned contracts, hedging LUNA. Market shifts led to naked LUNA shorts—downtrends triggered bottom-buying, rebounds triggered shorts. Later learned Binance halted LUNA deposits—LUNA rebounded, blowing all my FTX shorts.”

“LUNA’s failure made me realize I needed contract trading education—failure stemmed from emotional trading. Then I began systematic contract trading.”

0xMumu’s start seems lucky—entering during a bull market, profiting via simple methods. But this “ease” meant he didn’t know *why* he profited—and luck-driven gains inevitably reverse when luck fades.

The LUNA contract blow-up made 0xMumu realize long-term profitability demands contract systems and risk discipline.

Contract failures ironically spurred 0xMumu’s systematic contract trading. Currently, he focuses on short-term trades in ranging markets—where he observes price-imbalances more clearly, enabling repeated tops-and-bottoms.

“I prefer short-term ranging-wave trades—comfortable in ranging or downtrend markets. Small losses usually occur, but big rallies are captured. I love catching spikes during crashes—large fund liquidations cause 3–5% spot-contract spreads, easiest for structural rebounds.”

“Short-term only relates to position sizing—if positions are heavy or leverage high, I can’t hold long—constantly watching makes tiny moves trigger exits. Comfortable holding means sleeping soundly—suitable for long-term.”

“Short-term encourages frequent entries—increasing losses—so I’ve lengthened holding periods—from minutes to hours—but still under one week.”

“I watch markets daily but rarely act—maybe once every few days—though intraday for majors. Altcoins hold longer—small positions, ≤$5,000 USDC at 20x—maximum tolerable loss—but higher volatility, bigger upside.”

Yu Ren: From “Gambling” to Systematically Profiting From Sentiment-Pricing Errors

“Started trading March 12, 2020—previously a pro poker player familiar with USDC concepts. Saw the crash March 12—first real-money buy, entering the market.”

“Started with spot, then moved to contracts. First spot buy: $4,000+ bottom—profited. Later lost heavily in bear-market contracts—BTC/ETH contracts lost ~$20M—painful. Realized poor risk control and treating trading as gambling—not work.”

“Poker was work—excellent risk/emotion control. Crypto felt casual—poker profits provided infinite off-table cashflow, so crypto attitude lacked seriousness.”

“Regained $20M+ around 2022—I gradually treated crypto as my main profession.”

“Summarizing my approach: I seek market structural cracks—arbitraging vulnerabilities.”

Yu Ren’s journey: Entered March 12 → profited in spot, then lost massively in bear-market contracts → rebuilt system centered on risk control, focusing on BTC/ETH contracts.

Applying poker’s professional mindset to crypto, Yu Ren built a complete system: positive EV + risk control + emotion management. Key profit source: finding market structural cracks—defined as price-sentiment misalignments:

- Take profits when sentiment premium peaks but price acceleration stalls—or even short. Buy when sentiment discount bottoms but price stops falling. Overall, profit from “sentiment premium errors + price-behavior divergences.”

- Price behavior is the primary standard—not sentiment. Sentiment diffusion, fee/position structures, on-chain/contract data cross-verify price behavior.

Qingyun: From Major-Coin Moving Averages to Altcoin Sector Rotation

“Entered 2017—only traded majors, paused, re-entered 2021 as external capital flowed—started with moving averages, establishing core logic.”

“2021 also began news trading—capturing Musk news, manually tracking DOGE, building first fortune.”

“My comfort zone is alts—riding altcoin waves. Recently learning commodity, forex, and futures swing-trading logic.”

Qingyun started with traditional technical analysis—moving averages—but grew into altcoin cycles, finding his path—developing a mature sector/leader framework. His description suggests ongoing learning of Price Action and order-flow logic from mature markets.

Why Alts?

“Alts profit from market profits—seasonal, affecting capital capacity—can’t trade constantly. Current large-capital movements are inconvenient—so I watch market sentiment.”

“Fundamental analysis isn’t always effective—I prioritize sentiment presence. For each sector, leader emergence signals sentiment—e.g., 2022 NFT/GameFi booms drew consensus/capital. Leaders mean tokens rallying >1 week, widely discussed.”

“Once prerequisites met—sector leader identified—I use details like OI to confirm—basically only trade leaders.”

In Qingyun’s System, Profits Come From:

- First judge BTC/ETH trends—then screen sectors via gainers’ lists and OI/position changes.

- “Trend continuation + sector capital diffusion” profits: new sector concepts emerge, leaders form, driving sector-wide rallies—then heavy positions.

- Exits rely more on technical triggers—not fundamental changes.

Jex: From “Loss Aversion” to Moving-Average Systems

“Entered 2021—drawn by altcoin boom hype. Deposited $2,000 to learn—later deemed spot too slow, tried leveraged contracts—inevitably lost.”

“I intensely hate losses—so I pivoted. Started airdrop farming, dog hunting, NFTs—luckily caught the boom, building first fortune. Later realized on-chain retreat—resumed trading, serendipitously joined Jingxin’s teaching group—systematically studying basics.”

“Unfortunately, 2022’s brutal bear market hit right after starting—teaching me risk and position management are most critical. Following Jingxin’s shorts yielded modest gains—but 2023’s recovery left me clueless—aim

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News