What will be the "ultimate form" of stablecoin chains?

TechFlow Selected TechFlow Selected

What will be the "ultimate form" of stablecoin chains?

A stablecoin-based Layer 1 conquers fintech.

By: Terry Lee

Translated by: Saoirse, Foresight News

In less than 12 years, stablecoins have evolved from niche cryptocurrency experiments into an asset class exceeding $280 billion. As of September 2025, their growth momentum continues to accelerate. Notably, the rise of stablecoins has been driven not only by demand but also by clearer regulatory environments—the recent passage of the U.S. GENIUS Act and the European Union’s Markets in Crypto-Assets Regulation (MiCA). Today, major Western nations formally recognize stablecoins as legitimate cornerstones of future financial systems. Interestingly, stablecoin issuers are not only "stable" but also highly profitable. Fueled by high interest rates in the United States, Circle, the issuer of USDC, reported revenue of $658 million in Q2 2025, primarily derived from interest on reserves. As early as 2023, Circle achieved profitability with a net profit of $271 million.

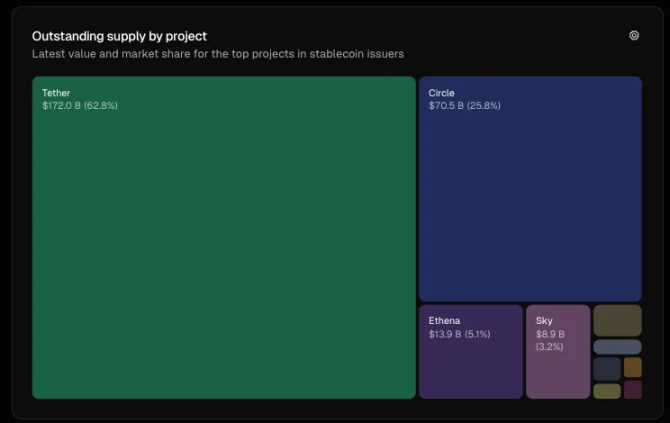

Source: tokenterminal.com, current stablecoin circulating supply data

This profitability has naturally sparked competition. From Ethena launching its algorithmic stablecoin USDe to Sky issuing USDS, numerous challengers have emerged, aiming to disrupt the dominance of Circle and Tether. As the competitive focus shifts, leading issuers like Circle and Tether are adjusting strategies by building proprietary Layer1 blockchains to control future financial rails. These financial rails can deepen competitive advantages, capture more fees, and potentially reshape how programmable money flows across the internet.

A trillion-dollar question arises: Can industry giants like Circle and Tether withstand disruption from non-native entrants such as Tempo?

Why Choose Layer1 Blockchains? Background and Differentiating Features

At their core, Layer1 blockchains are foundational protocols that support entire ecosystems, responsible for processing transactions, finalizing settlements, achieving consensus, and ensuring security. For readers familiar with technology, they can be understood as operating systems in the crypto space (e.g., Ethereum, Solana), upon which all other applications are built.

For stablecoin issuers, the strategic rationale behind building Layer1 blockchains is "vertical integration." Instead of relying on third-party blockchains like Ethereum, Solana, or Tron—or Layer2 networks—they are proactively creating their own rails to capture more value, strengthen control, and better align with regulatory requirements.

To understand this "battle for control," we can examine the Layer1 blockchains of Circle, Tether, and Stripe—each sharing common traits while pursuing distinct development paths.

Common Features

-

Using their issued stablecoin as the native currency, eliminating the need to hold ETH or SOL for gas fees. For example, transaction fees on Circle’s Arc blockchain must be paid in USDC; on certain chains like Tether’s Plasma, fees are even fully waived.

-

High throughput and fast settlement: These Layer1 blockchains promise sub-second finality (transactions become irreversible within fractions of a second) and thousands of transactions per second (TPS)—ranging from over 1,000 TPS on Plasma to over 100,000 TPS on Stripe’s Tempo.

-

Optional privacy and compliance environment: These blockchains create "curated crypto ecosystems" with stronger privacy and higher compliance, albeit at the cost of some centralization.

-

Ethereum Virtual Machine (EVM) compatibility: Ensures developers can build applications using familiar standards, lowering technical barriers.

Key Differences

-

Circle’s Arc: Designed for both retail and institutional users. Its proprietary foreign exchange engine is highly attractive for capital markets trading and payment use cases, positioning it as a potential “Wall Street’s preferred rail” in crypto.

-

Tether’s Stable Chain and Plasma Chain: Centered on “accessibility,” featuring zero gas fees to enable seamless, frictionless transactions for retail and peer-to-peer (P2P) users.

-

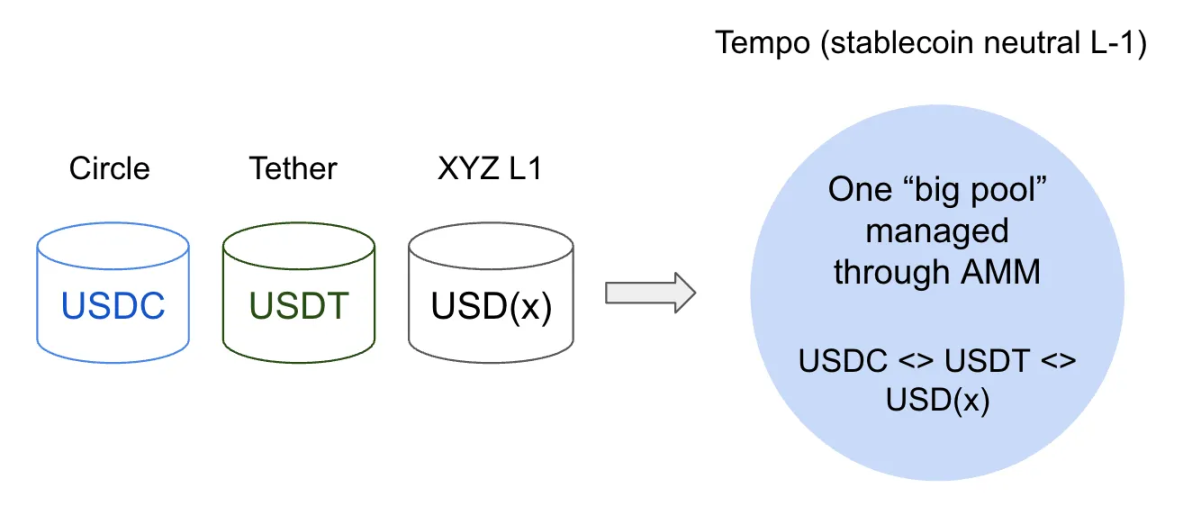

Stripe’s Tempo: Takes a different approach by remaining “stablecoin-neutral.” It does not tie itself to a single stablecoin but supports multiple USD stablecoins via a built-in automated market maker (AMM), offering greater flexibility that may appeal to developers and users not tied to one specific dollar-denominated token.

Application Trends of Layer1 Blockchains

Based on my analysis, three major trends are currently emerging:

Trend One: Traditional Finance Integration – Building Trust and Regulatory Alignment

For stablecoin issuers, a key goal in building proprietary Layer1 blockchains is to “earn trust.” By controlling the rails or ecosystem rather than relying solely on third-party networks like Ethereum or Solana, Circle and Tether can more easily offer “compliance-ready” infrastructure that meets regulatory frameworks such as the U.S. GENIUS Act and EU MiCA.

Circle positions USDC as a “compliant product”: institutions handling USDC redemption must adhere to KYC and anti-money laundering (AML) compliance frameworks. Its newly launched Layer1 blockchain, Arc, goes further by combining “auditable transparency” with “privacy features,” making it a potentially reliable choice for institutional users. Tether adopts a similar strategy through Stable Chain and Plasma Chain, aiming to become the “infrastructure backbone” for banks, brokers, and asset managers.

Under this trend, a promising application could be foreign exchange trading. Leveraging Circle’s Arc blockchain—with sub-second finality, over 1,000 TPS throughput, and FX processing capabilities—market makers and banks could achieve instant settlement in FX trades. This opens opportunities to enter the daily $7+ trillion FX market, creating strong network effects. Stablecoins like USDC and EURC could become “native settlement assets,” locking developers into their ecosystems. It could also unlock doors for DeFi applications: enabling institutional-grade quote systems and reducing counterparty risk through smart contracts for rapid settlement.

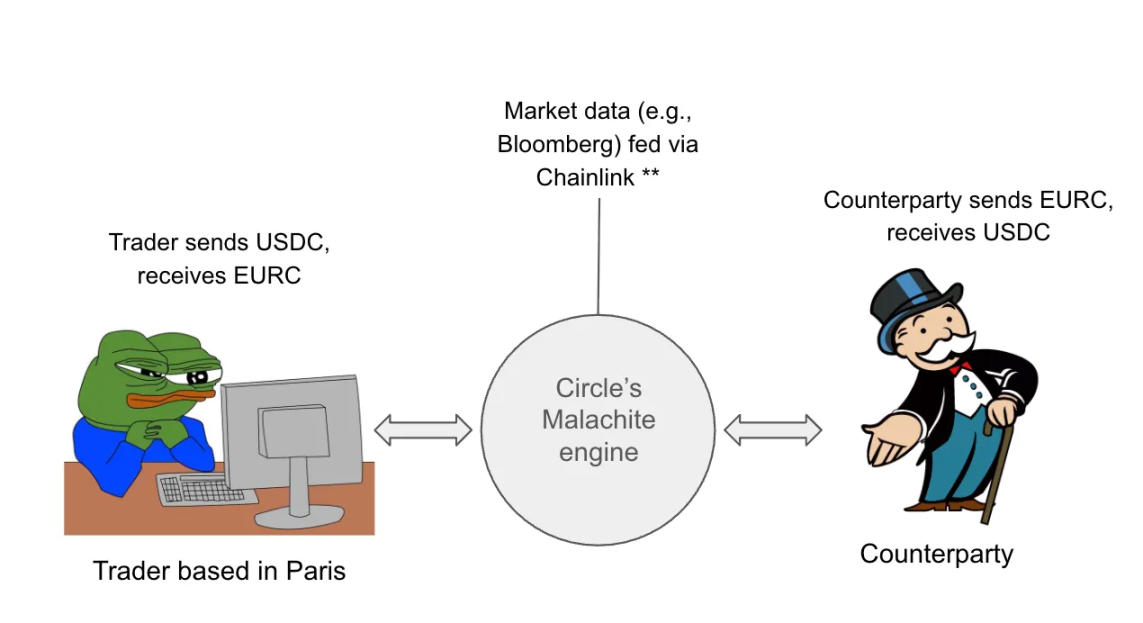

(Note: This scenario is illustrative, assuming data sourced from Chainlink oracles)

(Diagram: Trader completing a transaction via Circle’s Layer1 blockchain)

For a concrete example: A forex trader in Paris could use the USDC/EURC pair on Arc blockchain, leveraging Malachite FX engine to execute a $10 million USD-to-EUR swap. Assuming real-time exchange rates are fetched via Chainlink oracle (e.g., 1 USD = 0.85 EUR), the entire transaction completes within 1 second—reducing the traditional FX settlement cycle of “T+2” (two days post-trade) to “T+0” (real-time settlement). This is the transformative power of technology.

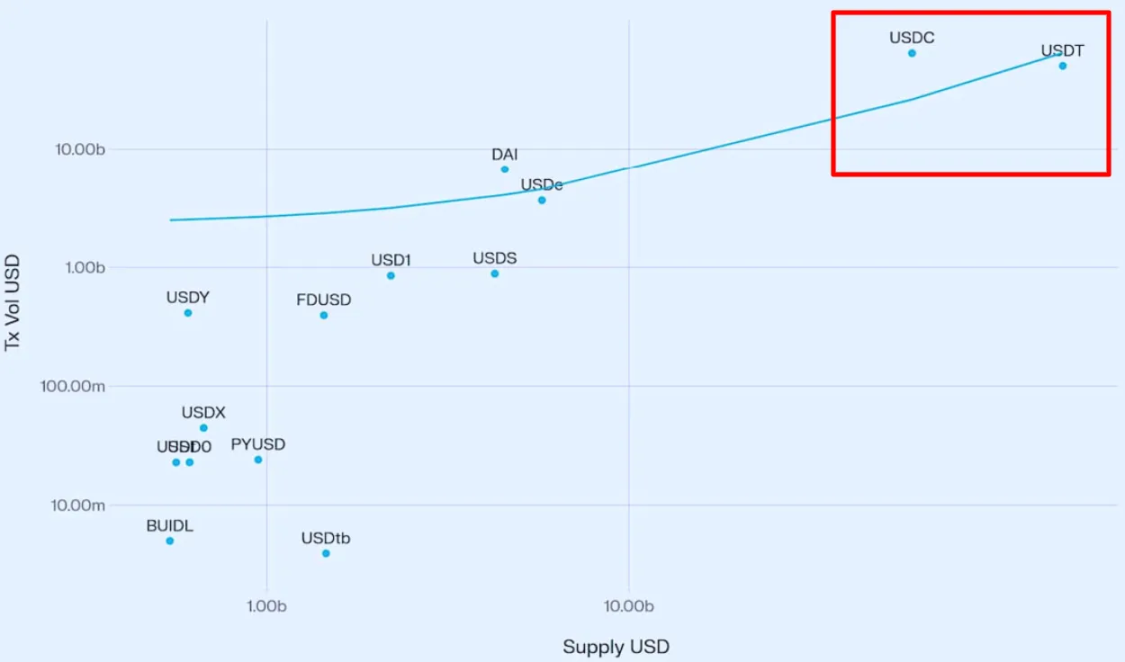

Source: Vedang Ratan Vatsa, “Stablecoin Growth and Market Dynamics”

Data supports this direction. Research by Vedang Ratan Vatsa shows a significant positive correlation between stablecoin supply and trading volume: larger supply leads to deeper liquidity and higher adoption. As the two leading issuers, Tether and Circle clearly hold an advantage in capturing institutional capital flows.

However, integrating traditional finance with blockchain rails still faces major challenges: coordinating regulators, central banks, and regional laws requires navigating complex environments (e.g., alignment with multiple central banks could take years); issuing stablecoins for emerging market currencies is harder—if products don’t match market needs, adoption may stall or fail entirely; even if these hurdles are overcome, banks and market makers may remain cautious about migrating “critical infrastructure” to new rails—migration could increase costs (not all currencies are on-chain, requiring institutions to maintain both legacy and crypto systems) and introduce uncertainty. Moreover, as Circle, Tether, Stripe, and even banks launch their own blockchains, the risk of “liquidity fragmentation” intensifies: if no single rail achieves sufficient scale and liquidity, none may dominate the $7 trillion daily FX market.

Trend Two: Can Stablecoin Chains Challenge Legacy Players in Traditional Payments?

As Layer1 blockchains attract traditional financial institutions with “programmability,” their rise may also challenge established payment giants like Mastercard, Visa, and PayPal. The reason is that Layer1 blockchains can deliver “instant, low-cost” settlement through various decentralized applications. Unlike the “closed, single-platform” models of traditional payment giants, these blockchain rails are “open and programmable,” offering developers and fintech firms flexible foundations—similar to “renting AWS cloud services” instead of “building proprietary payment infrastructure.” This shift enables developers to rapidly launch cross-border remittances, AI-driven payments, tokenized assets, and more—all with “near-zero fees” and “sub-second settlement.”

For instance, a developer could build an “instant settlement payment DApp” on a stablecoin chain: merchants and consumers enjoy fast, low-cost transactions, while Layer1 issuers like Circle, Tether, and Tempo capture value as “core infrastructure.” The biggest difference lies here: this model eliminates intermediaries like Visa and Mastercard, allowing developers and users to directly reap more benefits.

But risks remain: as more issuers and payment firms launch their own Layer1 blockchains, ecosystems may become “fragmented”—merchants might face multiple “dollar tokens” from different chains that lack interoperability. Circle’s Cross-Chain Transfer Protocol (CCTP) aims to solve this by maintaining a “single liquid version” of USDC across chains, but it only applies to Circle-issued tokens and has limited reach. In this “oligopolistic” market, “cross-chain interoperability” may become a critical bottleneck.

Recently, Stripe announced Tempo—a stablecoin-neutral Layer1 blockchain incubated by Paradigm—further shifting the landscape. Unlike Circle and Tether, Stripe has not launched its own stablecoin but supports multiple stablecoins for payments and gas fees via a built-in AMM. This “neutrality” could be highly attractive to developers and merchants—offering greater flexibility without lock-in to a single stablecoin—potentially giving Stripe a breakthrough in areas dominated by crypto-native companies.

Trend Three: Duopoly Dynamics – Competition Between Circle and Tether

While Layer1 blockchains challenge traditional players, they are also reshaping the stablecoin market. As of September 2025, Circle and Tether dominate the stablecoin market, collectively holding nearly 89% of issuance—Tether at 62.8%, Circle at 25.8%. By launching Layer1 blockchains like Arc, Stable, and Plasma, both further solidify their advantages and set high entry barriers (e.g., Tether’s Plasma chain imposes a $1 billion cap on treasury deposits for token sales, significantly raising the bar for new entrants). Using the Herfindahl-Hirschman Index (HHI) to measure market concentration, the current HHI stands at 4600 (62.8² + 25.8² ≈ 4466), far exceeding the traditional antitrust review threshold of 2500.

Yet, a potential threat is emerging—“stablecoin-neutral Layer1 blockchains.” Stripe’s Tempo lowers merchant onboarding barriers and alleviates regulators’ concerns about “market concentration.” If “neutrality” becomes the industry standard, Circle and Tether’s “closed competitive edge” could turn into a disadvantage—risking loss of network effects and market attention. In that case, today’s “duopoly” may evolve into a “multi-polar oligopoly,” with different rails dominating niche segments.

Conclusion

In summary, stablecoins have become a significant sector exceeding $280 billion, with highly profitable issuers. The rise of stablecoin-based Layer1 blockchains reveals three key trends: (1) enabling traditional finance to access crypto-native rails and enter the growing foreign exchange market; (2) reshaping payments by removing intermediaries like Mastercard and Visa; and (3) shifting the market structure from a “duopoly” (HHI 4600) toward a broader “oligopoly.” Together, these shifts point to a larger trajectory: stablecoin issuers like Circle and Tether, along with new entrants like Stripe’s Tempo, are evolving beyond being mere “bridges between crypto and fiat” to becoming core pillars of future financial infrastructure.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News