Bitget UEX Daily Report | Hormuz Strait Blockade Triggers Significant Oil Price Rebound; US Stocks Under Pressure, Tech Stocks Lead Declines; SpaceX Announces Pricing Today

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Hormuz Strait Blockade Triggers Significant Oil Price Rebound; US Stocks Under Pressure, Tech Stocks Lead Declines; SpaceX Announces Pricing Today

Overall, institutions recommend focusing on energy-related stocks and defensive allocations, while remaining vigilant about the potential impact of geopolitical events on risk sentiment. Short-term volatility is expected to intensify, but there are no signs of a systemic collapse; the medium-term outlook hinges on de-escalation of the conflict and economic data.

I. Top News Highlights

Federal Reserve Updates

Mixed inflation data: Core metrics remain moderate, but energy prices push headline inflation higher

- U.S. CPI rose 4.2% YoY and 0.5% MoM in May—matching consensus expectations and marking the first time in three years that it has exceeded 4%; core CPI rose 2.9% YoY and increased only 0.2% MoM—below expectations.

- Rising energy costs are the primary driver; underlying inflationary pressures remain relatively contained. Market impact: Data is broadly neutral and does not significantly alter market expectations for Fed rate cuts. However, combined with geopolitical energy shocks, it may increase uncertainty around monetary policy decisions. Investors should closely monitor upcoming FOMC signals.

International Commodities

Iran closes Strait of Hormuz; U.S. military confirms retaliatory strikes—oil prices surge

- Iran’s Armed Forces declared closure of the Strait, warning all vessels face attack risk; the U.S. military conducted additional defensive strikes against Iranian targets in response to acts of aggression.

- Trump-related statements and Iran’s denial of direct communication, coupled with additional agreement conditions, have complicated negotiations. Market impact: A critical global oil transport route is now under threat, pushing up oil prices in the short term and transmitting inflationary pressure across markets. Energy assets benefit, while overall market risk-aversion sentiment rises.

Macroeconomic Policy

Trump’s additional demands delay Iran deal; economists urge stabilization of Strait situation

- Additional requirements include diluting enriched uranium stockpiles and committing to transit fees—delaying final agreement.

- Inflation aligns with expectations, though energy-related factors warrant close monitoring; Trump must provide policy certainty for the Fed. Market impact: Geopolitical uncertainty叠加 inflation data may reinforce market caution toward easing expectations. Short-term beneficiaries include safe-haven and energy-related assets.

II. Market Recap

Commodities & FX Performance (Real-time Update)

- Spot Gold: ~$4,080/oz, +0.59% over 24 hours.

- Spot Silver: ~$64/oz, +1.24% over 24 hours.

- WTI Crude Oil: ~$92/barrel, +2.2% over 24 hours.

- Brent Crude Oil: ~$95/barrel, +1.68% over 24 hours.

- U.S. Dollar Index (DXY): ~99.92, -0.12% over 24 hours.

Key Drivers Analysis: Iran’s closure of the Strait of Hormuz—a vital oil shipping channel—has directly amplified global supply disruption risks, fueling a strong rebound in oil prices. U.S. military action and controversy surrounding Trump-Iran communications have further intensified geopolitical tensions. Although May’s U.S. CPI data met expectations, rising energy prices remain the main driver pushing headline inflation to a three-year high; the moderation in core metrics has limited extreme market reactions. The dollar index remained relatively stable, reflecting market balancing amid risk events. Institutional consensus holds that near-term energy volatility will feed into inflation expectations; if the Strait issue persists, the Fed may be forced to adopt a more cautious stance. Gold and other safe-haven assets face short-term pressure but retain medium-to-long-term support; oil and energy-linked assets show strong correlation; market volatility is expected to remain elevated.

Cryptocurrency Performance

- BTC: ~$62,130, +0.42%.

- ETH: ~$1,640, -0.28%.

- Total Crypto Market Cap: ~$2.2 trillion, -2.4% over 24 hours.

- Liquidations: $409 million total over 24 hours, including $240 million long liquidations.

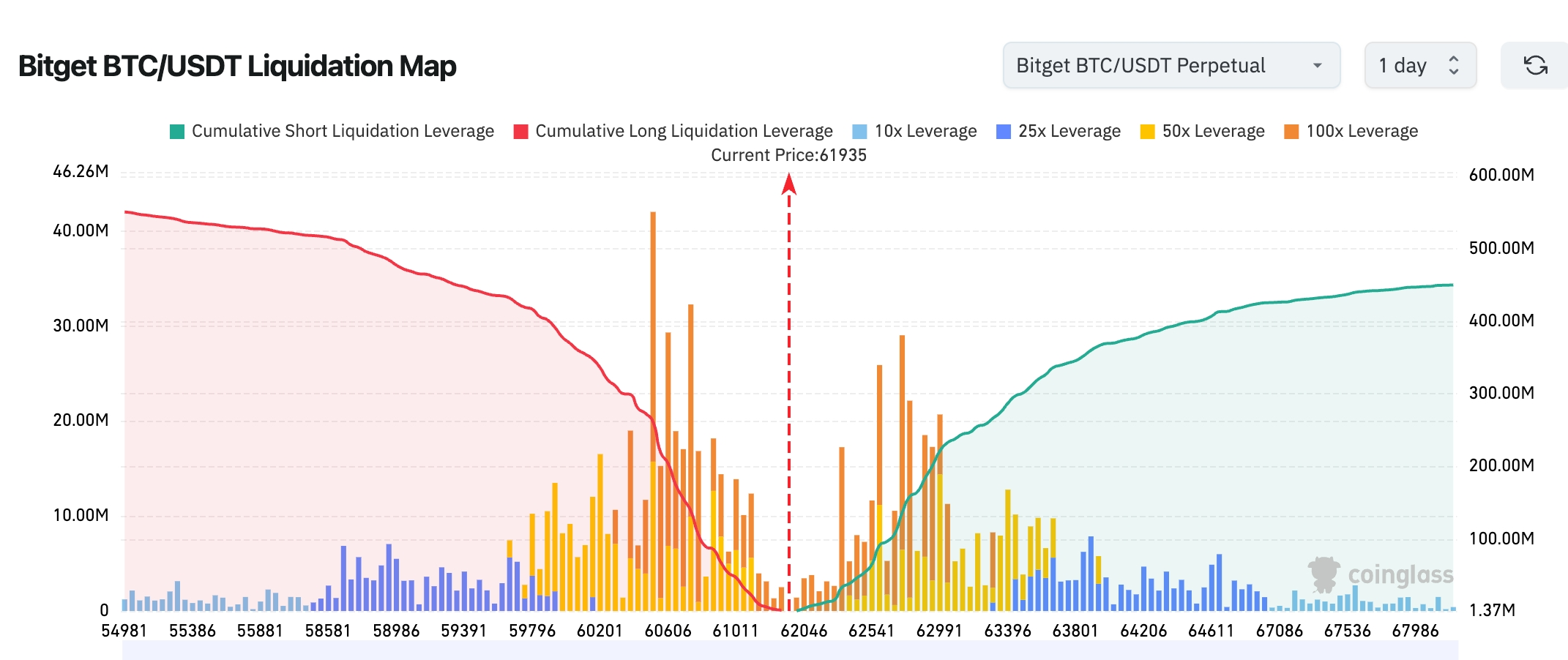

- Bitget BTC/USDT Liquidation Map: Current BTC price ~$61,935. A dense cluster of long liquidation orders lies between $60,000–$60,600; a renewed downward move could trigger cascading long stop-outs and test the key $60,000 support level. Above $62,800–$64,000, accumulated short liquidation pressure exceeds $400 million; if BTC breaks above $62,500 and sustains momentum, short covering (“short squeeze”) may propel price rapidly toward $64,000.

- Spot ETF Net Inflows/Outflows: BTC spot ETFs recorded $77.4 million net outflow yesterday.

Key Drivers Analysis: Geopolitical conflict lifted energy prices and inflation expectations, creating macro headwinds for risk assets. Crypto markets moved in tandem with U.S. equities. Modest ETF outflows reflect investor caution; leveraged liquidations exacerbated price volatility. BTC showed relative resilience versus ETH, underscoring its role as a store-of-value asset amid uncertainty. Technically, price remains range-bound; institutional views hold that near-term macro and geopolitical developments dominate, while medium-term focus shifts to Fed policy and capital flows—overall trend remains cautious but shows no systemic risk signals.

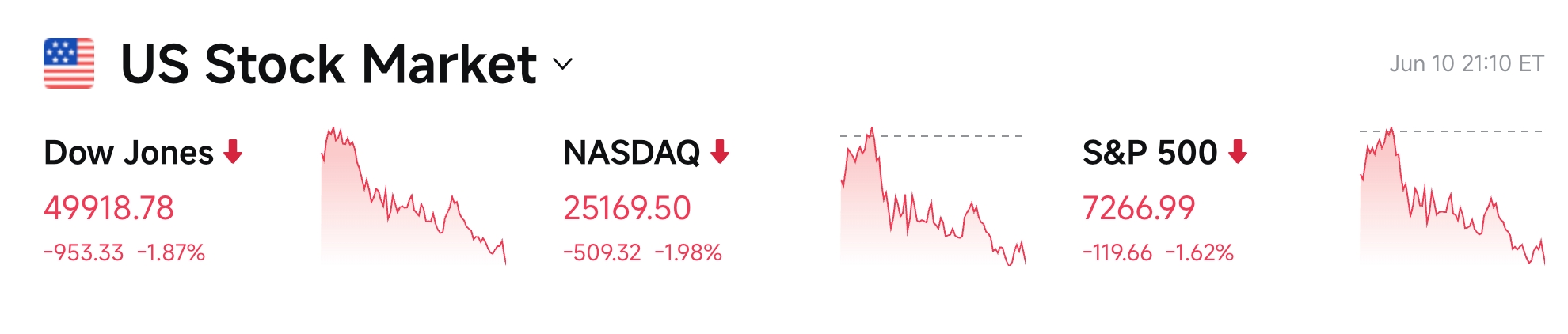

U.S. Equity Index Performance

- Dow Jones Industrial Average: Closed at 49,918.78 (-1.87%), extending consecutive declines.

- S&P 500: Closed at 7,266.99 (-1.62%), with clear divergence between tech and energy sectors.

- Nasdaq Composite: Closed at 25,169.50 (-1.98%), dragged down heavily by tech stocks.

Tech Giants’ Performance

- NVDA: $200.42, -3.73%.

- AAPL: $291.58, +0.35%.

- MSFT: $397.36, -1.46%.

- GOOGL: $356.85, -2.16%.

- AMZN: $239.03, -2.11%.

- META: $575.94, -1.48%.

- TSLA: $384.66, -3.03%.

Summary & Key Drivers: Tech giants broadly followed broader market weakness, with semiconductors under particular pressure. AI-linked stocks weakened amid valuation concerns and sector rotation; consumer-tech names like Apple proved relatively resilient. Geopolitical developments and inflation data formed the common backdrop, prompting partial fund reallocation from high-valuation tech to energy—highlighting stock-specific divergence: some benefit from long-term AI narratives, while others face macro or company-specific headwinds.

Crypto Stock Futures Market Overview

Core Metrics

- 24H Total Trading Volume: $29.87 billion (+32.21%)

- Open Interest (OI): $7.54 billion (-3.05%)

- 24H Total Liquidations: $80.99 million

- Trading Volume Share: 15.22%

- Open Interest Share: 7.40%

- Liquidation Share: 19.79%

Sector Open Interest Ranking

- Technology Sector: $1.12 billion

- Financial Sector: $145 million

- Consumer Sector: $69.64 million

- Biotech Sector: $18.81 million

- Industrial Sector: $16.91 million

Capital Flow Observations

Market trading volume surged 32%, yet open interest declined 3%—indicating heightened trading activity alongside partial position unwinding, reinforcing short-term speculative behavior.

The technology sector continues to dominate open interest, but its liquidation share approaches 20%, signaling accelerated leveraged turnover and elevated market volatility.

III. Heatmap: Capital Allocation (by Open Interest)

Commodities

- Gold (GOLD): $3.33 billion (largest open interest in the market)

- Silver (SILVER): $675 million

- WTI Crude Oil: $629 million

- Brent Crude Oil (BRENT): $433 million

Tech Stocks

- NVIDIA (NVDA): $238 million

- Marvell Technology (MRVL): $172 million

- Google (GOOGL): $98.6 million

- Circle (CRCL): $94.2 million

- Tesla (TSLA): $83.8 million

- MicroStrategy (MSTR): $65.1 million

- Intel (INTC): Active positions

- SanDisk (SNDK): Active positions

Capital Flow Observations

Gold open interest climbed further to $3.33 billion, maintaining its position as the largest single-position holding across the entire market—underscoring persistent investor demand for safe-haven assets amid inflation, interest-rate, and geopolitical uncertainty.

Within the technology sector, capital remains concentrated on AI supply-chain leaders—NVIDIA and Marvell maintain high open interest. Meanwhile, crypto-focused names MicroStrategy and Circle continue drawing significant attention, suggesting ongoing strategic positioning in digital asset-related themes. Concurrent increases in WTI and Brent crude open interest signal heightened trader engagement with energy price volatility.

Sector Momentum Observations

Energy / Shale Oil Sector: Up ~1.5–2.5% (outperforming broader market)

- Key stocks: Devon Energy (DVN) up ~5.7–6.7%; Apache Corporation (APA) up ~4%.

- Drivers: Closure of the Strait of Hormuz directly boosted oil prices and heightened supply disruption fears—energy producers stand to benefit. WTI crude rose over 2%, supported by positive company-level production guidance and M&A integration tailwinds. Despite broad market weakness, energy stocks demonstrated strong defensive attributes; short-term performance may continue to reflect geopolitical risk premiums—but investors should watch for pullbacks should tensions ease.

Semiconductor Sector: Down ~3–5% (dragging down tech indices)

- Key stocks: Broadcom (AVGO) down >5%; Qualcomm (QCOM) down nearly 7%.

- Drivers: Amid broader market correction, profit-taking and valuation pressure emerged. While long-term AI chip demand remains robust, near-term macro uncertainty and sector rotation triggered capital outflows. As a high-beta segment, semiconductors reacted weakly to dual concerns over geopolitics and inflation. Institutions are watching AI capex execution closely, but near-term volatility is expected to persist.

IV. In-depth U.S. Equity Analysis

1. Oracle (ORCL) – Sharp Post-Earnings Decline

Event Summary: Oracle’s Q4 capex reached $15.9 billion, with full-year capex totaling $55.7 billion—significantly exceeding prior guidance of $50 billion. Adjusted revenue of $19.18 billion met or slightly exceeded expectations; however, cloud revenue (IaaS+SaaS) of $9.91 billion fell short of the $10 billion forecast. The company reaffirmed FY2027 revenue guidance of $90 billion and raised adjusted EPS guidance to $8.05, while also announcing refinancing-related news. Cloud infrastructure (IaaS) revenue grew strongly to $5.79 billion, reflecting robust AI-driven demand—but heavy capex raised market concerns about margins and cash flow, triggering a sharp after-hours decline.

Market Interpretation: Investors are focused on potential margin compression from high capex, even as cloud growth remains strong and remaining performance obligations rose sharply to $63.8 billion—highlighting sustained long-term AI infrastructure demand. Refinancing news further intensified valuation concerns, prompting short-term digestion of cost pressures.

Investment Implications: Cloud infrastructure and AI offer standout long-term growth potential. Monitor execution progress and margin improvement signals; short-term valuation pullback may present opportunities for phased accumulation.

2. Super Micro Computer (SMCI) – Announces Major Fundraising

Event Summary: The company plans a $7 billion equity and equity-linked financing round—including a $5 billion underwritten offering and a $2 billion ATM program—to procure components for ~$39 billion in AI server orders (from over 20 customers). Following a prior sharp price correction, this fundraising supports AI business expansion but raises dilution concerns, adding further downside pressure.

Market Interpretation: Though order backlog remains strong—reflecting red-hot AI server demand—the scale of equity financing at this high-growth stage triggers dilution and valuation concerns. Institutions view this move as strategically necessary to capture market opportunity, but execution efficiency and order conversion rates will be key watchpoints.

Investment Implications: AI server demand remains robust. Focus on capital utilization efficiency and delivery capability. Long-term outlook remains favorable—but short-term dilution impacts warrant caution.

3. Amazon (AMZN) – Secures Large Credit Facility

Event Summary: Amazon signed a $17.5 billion delayed-draw term loan facility led by Citigroup, with interest rates based on SOFR plus a spread (0.625–0.875%). The facility supports general corporate purposes and remains available until end-September. This bolsters liquidity to support business expansion and capital expenditures.

Market Interpretation: Demonstrates Amazon’s continued strong funding capacity even amid current interest-rate conditions—providing flexible capital for AI, cloud services, and retail expansion. Markets see this as enhancing financial resilience, though scrutiny remains on fund deployment and ROI.

Investment Implications: Strong liquidity supports long-term growth strategy. Investors should track transparency on fund usage and operational synergies.

V. Cryptocurrency Project Updates

1. Japanese gaming firm Enish sold its entire Bitcoin holdings—8.063 BTC—at a loss of ~$160,000, pivoting to a Solana ecosystem staking strategy targeting an annualized yield of 6–8%. The company stated that DAT 1.0—reliant on crypto price appreciation—has become increasingly unsustainable amid market volatility, whereas DAT 2.0—generating steady income via staking and validator operations—represents its new strategic direction.

2. Tom Lee: ETH supply is contracting; BitMine may not need to hold more than 5% of total supply.

3. According to The Block, SpaceX’s Thursday IPO could materially impact crypto markets, as some investors may sell crypto assets to purchase SpaceX shares. Spencer Hallarn, Global Head of OTC Trading at GSR, noted the IPO requires ~$75 billion in funding—and that capital must come from somewhere. Vetle Lunde, Head of Research at K33, pointed out that investor anticipation around hot IPOs like SpaceX may already be pressuring Bitcoin prices downward. Jeff Park, Advisor at Bitwise, added that Bitcoin is being used to finance upcoming high-profile capital transactions.

Meanwhile, SpaceX-related crypto trading activity is already robust. Talos data shows perpetual contract trading at ~$155—above the $135 IPO price—with open interest exceeding $385 million and cumulative volume reaching $2.7 billion. Alvin Kan, COO of Bitget Wallet, noted that self-custodial wallets are becoming a key conduit for capital market access; Bitget’s tokenized SpaceX IPO subscription has surged from $3 million to $13 million—achieving oversubscription.

4. Matt Hougan, Chief Investment Officer at Bitwise, reported that, based on meetings this week with over 40 financial advisors, advisor interest in stablecoins and tokenization has surpassed interest in Bitcoin. Despite the ongoing bear market, advisors remain engaged with crypto—but their focus is shifting beyond Bitcoin. Two reasons drive this: first, fiat depreciation trade narratives have faded from investor consciousness; second, stablecoins and tokenization have become central industry topics—regularly discussed by SEC Chair, Goldman Sachs CEO, and BlackRock CEO.

5. Julio Moreno, Head of Research at CryptoQuant, stated Bitcoin’s bottom may lie near $53,600—the current realized price—which historically has marked bear-market lows. Bitcoin currently trades at ~$62,150—about 9% above that level—but demand conditions remain weak. CryptoQuant estimates total demand fell by 652,000 BTC last week—the largest weekly drop since January 2022. 30-day ETF demand growth has fallen to -74,000 BTC—the weakest since ETF launch. Meanwhile, 30-day realized losses stood at 187,000 BTC—far below the 400,000 BTC seen when price first broke below $60,000 in February, and dramatically lower than the 1.2 million BTC loss during the November 2022 FTX collapse—suggesting capitulation-level selling has not yet occurred.

6. According to The Information, OpenAI founder Sam Altman expects OpenAI to go public within the next year.

VI. Today’s Market Calendar

Upcoming Data Releases

June 11 (Thursday)

- SpaceX IPO Final Pricing: One of history’s largest IPOs ($135/share, ~$75 billion raised, ~$1.77 trillion valuation)—a major catalyst for space/tech equities. ★★★★★ (plus major investor event)

- U.S. May PPI Release: A key gauge of inflationary pressure (expected to rise notably).

- U.S. Earnings: Adobe (ADBE) reports after market close (watch AI software demand).

- FIFA World Cup USA-Mexico-Canada (June 11–July 19): U.S. equities linked to sports value chains may draw attention.

June 12 (Friday)

- SpaceX Official Nasdaq Listing (Ticker: SPCX): Historic IPO event; first trading day; market sentiment boost. ★★★★★

- U.S. Economic Data: June University of Michigan Consumer Sentiment (preliminary), June 1-Year Inflation Expectations (preliminary).

*This Week’s Key U.S. Equity Themes:

“Super Event Week”: SpaceX IPO + Apple WWDC + Critical Inflation Data (CPI/PPI) + Oracle/Adobe Earnings—set to dominate U.S. tech and macro sentiment. Focus especially on AI, tech infrastructure, and space-related equities.

Institutional Views:

Multiple investment bank analysts note that escalating Iran-U.S. tensions—driving oil price spikes and Strait of Hormuz closure risks—represent the market’s core source of uncertainty, potentially elevating inflation and testing Fed patience. Institutions like BlackRock maintain relative optimism on U.S. equities—especially tech and AI—while highlighting potential drag on European and global growth from energy shocks. Gold faces short-term pullback pressure but remains bullish longer-term; crypto assets—including Bitcoin—show divergent performance amid macro volatility, with ETF outflows reflecting caution. Overall, institutions recommend focusing on energy beneficiaries and defensive allocations, while guarding against expanded geopolitical risk’s impact on risk appetite. Near-term volatility is expected to intensify—but no systemic collapse appears imminent. Medium-term outlook hinges on de-escalation and economic data trends.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice. Data presented herein may contain unavoidable inaccuracies; please refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News