J.P. Morgan Mid-Year Research Report Analysis: The AI Super-Cycle Is Far From Over—Reduce Cash Holdings and Increase Physical Asset Allocation

TechFlow Selected TechFlow Selected

J.P. Morgan Mid-Year Research Report Analysis: The AI Super-Cycle Is Far From Over—Reduce Cash Holdings and Increase Physical Asset Allocation

Global Asset Allocation Outlook for the Second Half of the Year Amid Trade Tensions and AI Trends

By David, TechFlow Research

TechFlow Insight:

J.P. Morgan’s Wealth Management division released its 2026 Mid-Year Outlook report on June 1—a semi-annual update guiding its high-net-worth clients on portfolio strategy for the second half of the year.

Against a backdrop of the Strait of Hormuz blockade pushing oil prices higher, inflation re-emerging, and AI narratives shifting from euphoria to skepticism, the report strikes an overall tone of cautious optimism—albeit with concrete adjustments to asset allocation.

J.P. Morgan argues that markets have overpriced three key global risks: fragmentation, inflation, and AI-driven disruption—making current market volatility precisely the right entry window.

The overarching recommendation is:

Maintain exposure to the AI supercycle and U.S. equities; hedge inflation via real assets and alternative strategies; reduce cash holdings; and increase focus on emerging markets.

If you hold U.S. tech equities—or are weighing whether to add or reduce exposure in H2—this report’s framework and data merit close attention. We’ve condensed and interpreted the original report, reordering insights by investment relevance.

Six Key Takeaways:

① The AI supercycle is not over—and markets are overly pessimistic.

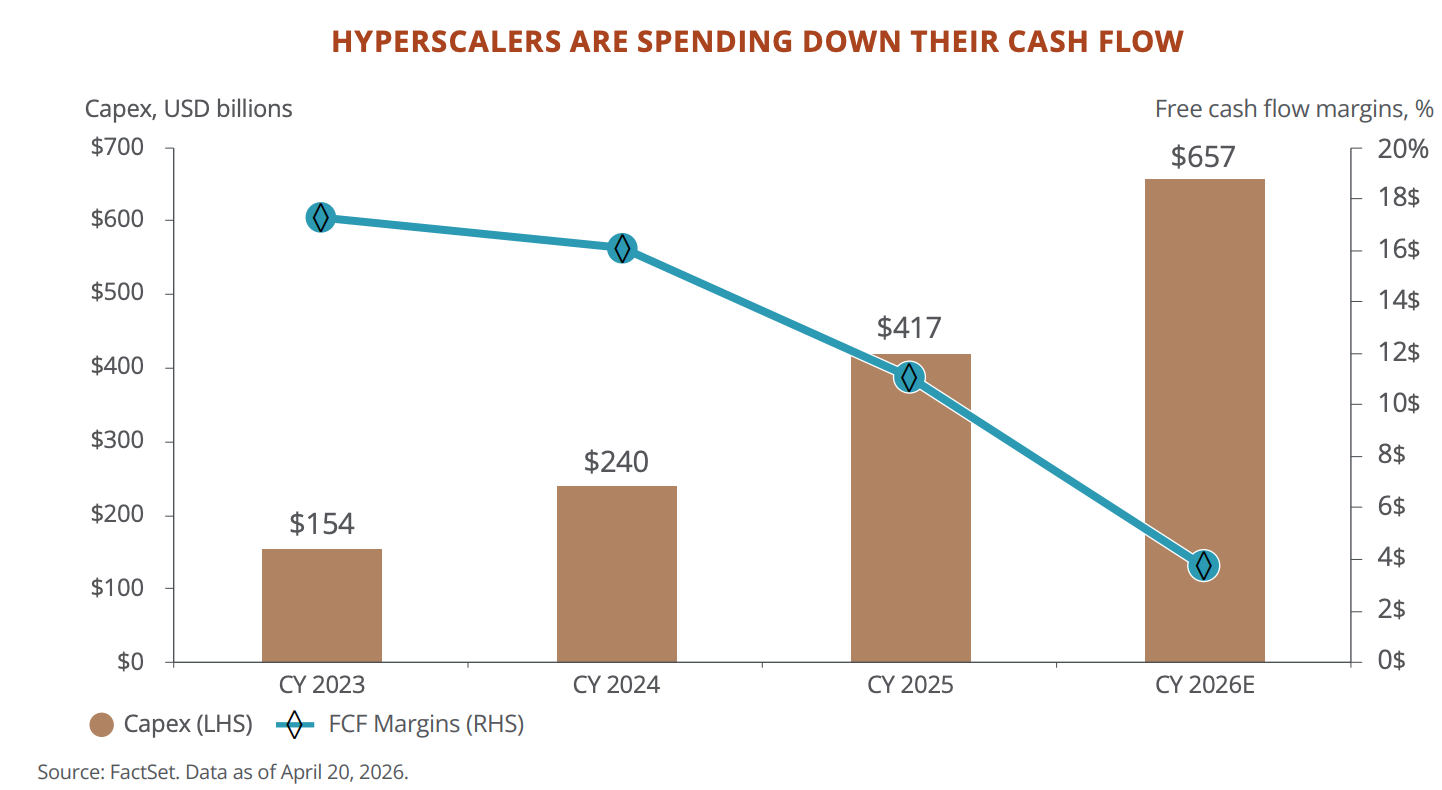

Capital expenditures (capex) for the five hyperscalers—Microsoft, Meta, Oracle, Google, and Amazon—are projected to exceed $650 billion in 2026, up $130 billion from the prior earnings season. AI-related investment contributed 25 basis points to U.S. real GDP growth in 2025. Taiwan’s GDP growth exceeded 7%, the fastest since 2010, driven primarily by semiconductor exports. JPM believes markets are pricing in “AI peaking”—but the data do not support this narrative.

② Yet the financial profile of hyperscalers is changing.

Free cash flow (FCF) is expected to fall from $240 billion in 2024 to $73 billion by end-2026. Microsoft’s forward P/E has declined from a peak of 35x during the early AI era to 22.5x. These firms are shifting from “light-asset, high-return” models to “heavy-asset, high-investment” ones—and markets are still digesting this transition.

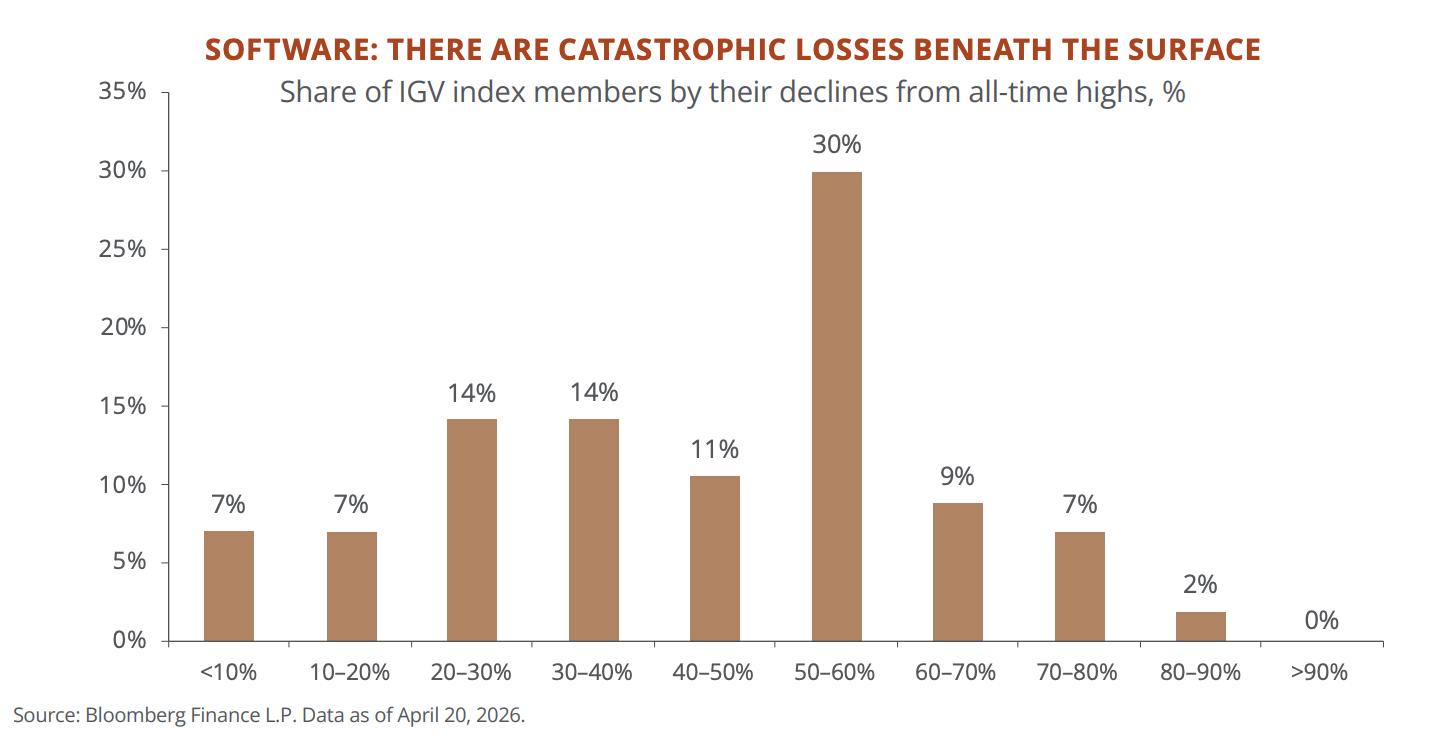

③ SaaS is undergoing a silent bloodbath.

Approximately half the constituents of the S&P Software Index (IGV) have fallen more than 50% from their all-time highs. JPM’s basket of “AI-vulnerable stocks” is down nearly 20% YTD. In private credit markets, software companies account for 21% of exposure; adding tech and business services brings the total to 40%. The impact of AI on subscription-based software business models is already materializing.

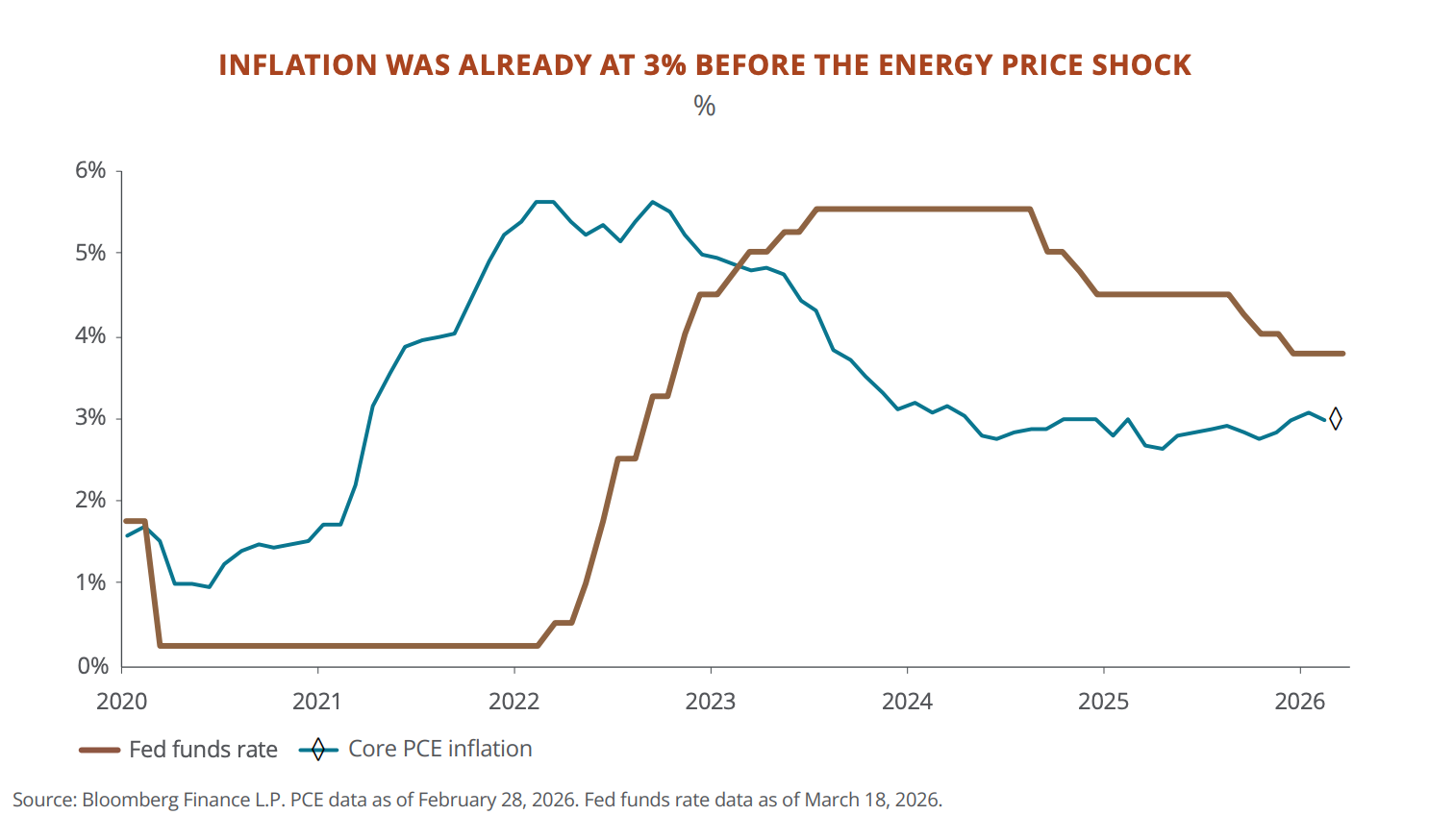

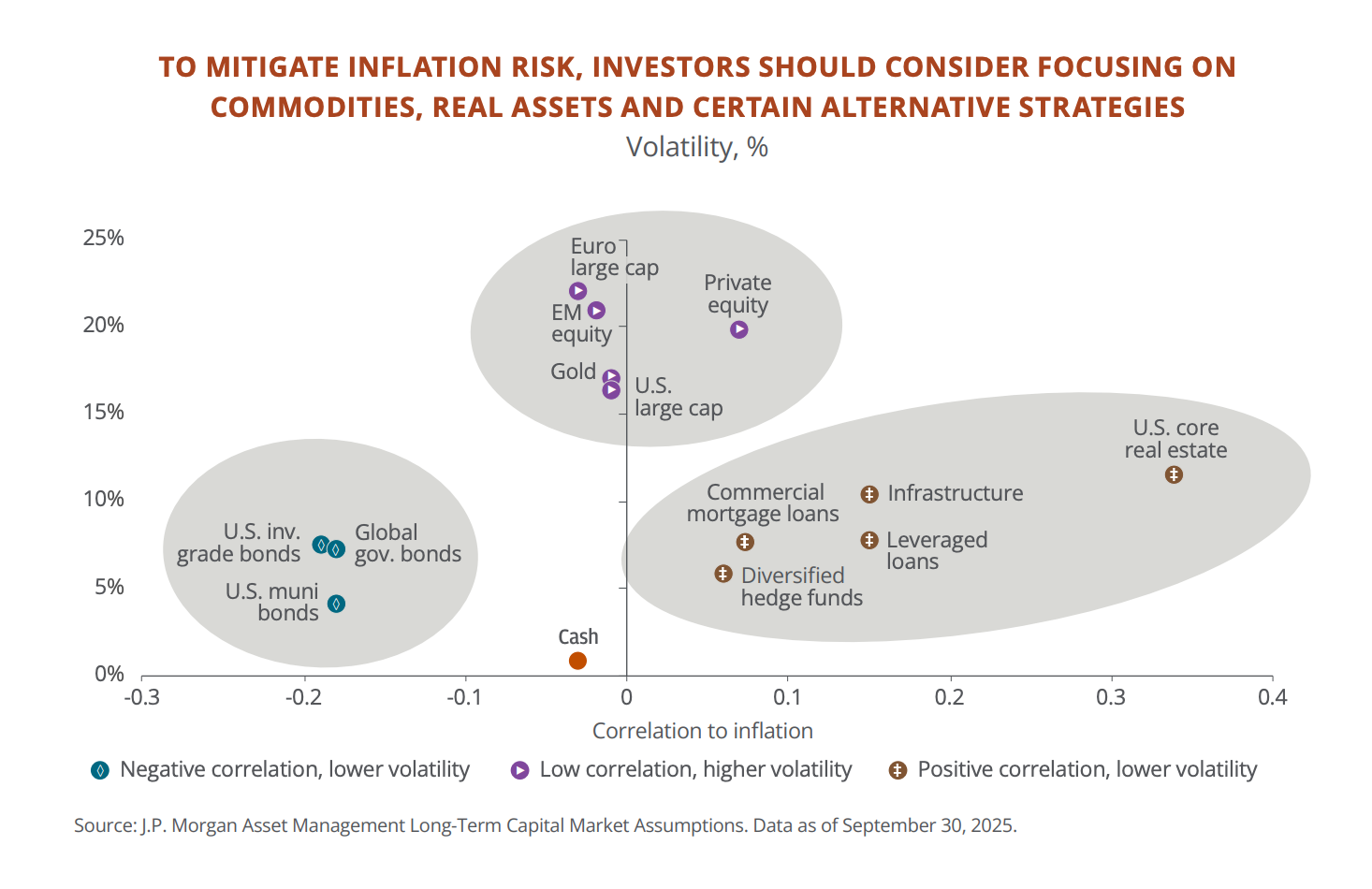

④ The inflation floor is structurally higher than pre-pandemic levels—and cash is losing value gradually.

U.S. core PCE was already sticky at 3% before the energy shock. Consumer prices have risen cumulatively by 25% since 2020, while core fixed income returned only 6%. Nearly 20% of JPM’s client assets remain in cash and short-term bonds. The message is clear: You think you’re avoiding risk—but you’re actually losing money.

⑤ The Strait of Hormuz blockade represents the largest oil supply shock since WWII—but JPM recommends buying the dip.

Oil prices nearly doubled, triggering a ~10% correction in U.S. equities and briefly pushing the S&P 500’s P/E below 20x. Historical JPM data show that buying after VIX breaches 30 yields positive returns 70–83% of the time within six months, with an average return of 12.4%.

⑥ Emerging markets may present the strongest opportunity in H2.

EM corporate earnings are expected to grow 46%, while the region’s P/E stands at just 11.8x. Taiwan and South Korea anchor critical nodes in the AI hardware supply chain. Latin America holds over 40% of global copper reserves and nearly 60% of lithium reserves. Chinese equities trade at their deepest discount to other Asian markets in 20 years; JPM’s stance is shifting toward “cautious warming.”

On AI: Markets Are Pricing “Peak AI”—J.P. Morgan Says It’s Too Early

JPM opens by stating that Wall Street’s narrative around the AI supercycle is “already too pessimistic.”

Core supporting data:

The five cloud giants—Microsoft, Meta, Oracle, Google, and Amazon—are collectively expected to spend over $650 billion on capex in 2026. Cloud-based GPU rental prices—the core chips used to train AI models—have risen 40% since last October, with supply still lagging demand. Nvidia trades at a 40% discount to its 10-year average P/E. Markets are pricing in “peak chip sales,” yet cloud revenue continues to accelerate.

Meanwhile, the financial profiles of these five firms are evolving. Free cash flow is expected to drop from $240 billion in 2024 to $73 billion by end-2026; Microsoft’s P/E has fallen from a peak of 35x in the AI era to 22.5x. The light-asset model that attracted investors over the past decade is being rewritten by heavy capital commitments. JPM advises focusing on revenue growth—not cash flow—for now, but warns that these investments could become a drag if demand slows.

A few additional AI-related observations serve as localized risk signals amid broader trends:

Traditional software firms are AI’s first true victims. Roughly half the stocks in the U.S. software index have fallen more than 50% from their peaks, with median operating margins at just 4%. The logic is straightforward: SaaS charges per user—and AI reduces headcount. This pressure has spilled into lending markets: ~21% of U.S. direct loan market funding goes to software companies, and publicly traded tech loan funds have dropped near their prior cycle lows. JPM’s stress tests suggest leveraged losses could reach 4% under extreme scenarios—but systemic risk remains low for now.

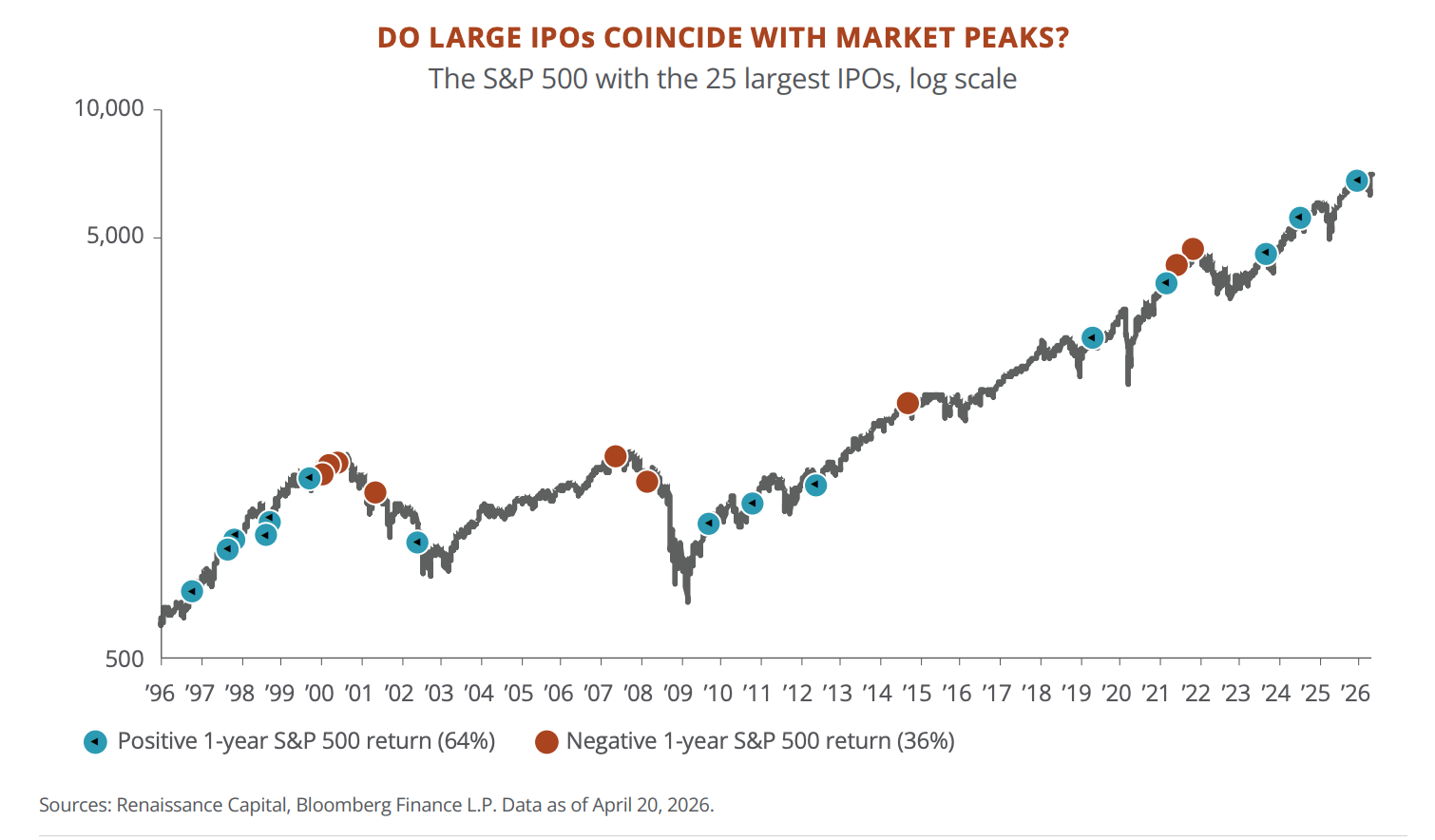

SpaceX, Anthropic, and OpenAI may go public en masse this year—a historically bearish signal. Following the 25 largest IPOs over the past 25 years, new issues underperformed the broad market by 30 percentage points in their first year; 12 of 18 underperformed. Years featuring mega-IPOs saw median market returns of just 3%, far below the long-term average of 10%. JPM doesn’t declare a peak outright—but explicitly treats SpaceX’s IPO as a “cycle thermometer.”

On Inflation: Inflation Won’t Return to 2%—Your Cash and Bonds Are Losing Value

The crux of this section isn’t just the Strait of Hormuz driving up oil prices—it’s that U.S. inflation had already failed to revert to normal before the oil shock.

Core PCE stood at 3.1% YoY in January 2026, with particularly solid gains in local-service categories like food services and personal care. Then oil prices doubled. The Fed estimates each $10/barrel rise lifts inflation by ~0.3 percentage points—this time, the rise was $40.

JPM judges a full 1970s-style repeat unlikely. There’s no wage-price spiral in labor markets, voluntary quits are declining, housing inflation has eased from 5% at end-2024 to just over 3%, and China’s excess capacity continues to suppress global commodity prices. Still, the structural inflation floor sits meaningfully higher than pre-pandemic levels—likely hovering near 3%.

JPM’s recommended response: Increase allocations to real assets.

U.S. consumer prices have risen 25% since 2020, while bonds delivered only 6%—and cash even less. You think your money is sitting still—but it’s shrinking annually. Nearly 20% of JPM’s private banking clients’ assets remain in cash and short-term bonds.

Hence, JPM recommends reallocating part of that capital into inflation-linked assets:

- Commodities, infrastructure, and real estate—which tend to appreciate alongside inflation—should collectively make up ~5% of portfolios.

- Gold alone is recommended at 3–6%.

- Macro-oriented hedge funds also offer diversification: They gained 9% in 2022 when both equities and bonds fell. That said, JPM acknowledges 94% of its private banking clients have never invested in hedge funds—and 86% have never held infrastructure products.

In one sentence:

Inflation may not spiral out of control—but it won’t return to 2%. If your portfolio still follows a traditional 60/40 equity-bond split plus large cash holdings, JPM believes you’re preparing for a world that no longer exists.

On Geopolitics: Chinese Equities May Be Due for a Structural Re-rating

This section covers the broadest terrain—from Middle East conflict to U.S.-China rivalry to European challenges. We focus exclusively on points directly relevant to investment decisions.

1. The Strait of Hormuz blockade was the biggest market shock of H1. Around 20 million barrels of oil transit the strait daily—roughly one-fifth of global oil consumption. Following U.S.-Israeli strikes against Iran, oil prices nearly doubled in days, and European natural gas prices surged ~100% in two days. Qatar Energy’s CEO warned that 15% of global LNG capacity may remain offline for up to five years. Qatar also supplies ~30% of the world’s helium—a critical input for chip manufacturing; South Korea has already warned of potential chip-fab shutdowns.

JPM expects de-escalation—but physical damage and persistent energy risk premiums will linger.

Thus, their advice to investors is: Buy U.S. equities on the dip.

U.S. equities fell ~10% in H1, and the S&P 500’s P/E briefly dipped below 20x. Historically, buying after VIX breaches 30 yields positive returns 70–83% of the time over six months—with an average gain of 12.4%.

2. The U.S. and China are building separate ecosystems—and markets may rapidly bifurcate into two camps. The U.S. restricts chip exports to China and coordinates with the Netherlands and Japan to constrain semiconductor equipment. China is expanding exports beyond the U.S., setting a record for Belt and Road investment in 2025—$53 billion into Brazil alone—and its trade volume with Latin America has already surpassed that with the U.S. JPM concludes that future investment returns may depend increasingly on which camp your assets belong to—not just the underlying company’s growth.

Yet fragmentation also creates opportunities—especially in emerging markets.

JPM highlights several areas:

- Latin America holds over 40% of global copper reserves and nearly 60% of lithium reserves, plus abundant nickel, rare earths, and agricultural resources. FDI has doubled over the past two decades; central banks demonstrate stronger inflation control than many developed-market peers; and politics are shifting toward more pragmatic, business-friendly governments.

- Gulf states are using oil revenues to build AI data centers: Saudi Arabia and Blackstone launched a $3 billion data center project costing 30% less than comparable U.S. builds.

- East Asia (Taiwan, South Korea) controls pivotal nodes in the AI hardware supply chain—if AI capex accelerates further, export strength and pricing power in these economies will continue rising.

- Chinese equities trade at their deepest discount to other Asian markets in 20 years. 80% of Chinese consumers express excitement about AI products (vs. 38% in the U.S.), and electricity costs are roughly half those in the U.S. JPM’s stance is “cautiously warming,” and a clearer pro-business policy signal could trigger a structural re-rating of Chinese equities.

In contrast, Europe is JPM’s most conservative call. Electricity prices are 2–4x U.S. levels; R&D spending is just 2.2% of GDP (vs. 3.6% in the U.S. and 5.2% in South Korea); and VC funding is one-tenth the size of the U.S.’s.

The energy shock may force the ECB to hike rates again. JPM recommends only defense- and infrastructure-related exposures in Europe—and avoids autos and consumer discretionary.

What JPM Is Betting On—and What It’s Avoiding

Condensing the 60-page report into one sentence: Volatile markets represent entry opportunities—but entry must be executed differently.

What to overweight:

- AI infrastructure (chips, optical modules, power), EM equities and bonds, real assets (commodities, infrastructure, gold), defense-related names, and Chinese AI-themed stocks (with caution).

What to avoid:

- Cash, traditional subscription-based software firms, European autos and consumer discretionary, and pure 60/40 equity-bond portfolios as a sole strategy for H2.

Original report link:

https://www.jpmorgan.com/content/dam/jpmorgan/documents/wealth-management/mid-year-outlook-2026.pdf

This article is a summary and interpretation of J.P. Morgan Wealth Management’s 2026 Mid-Year Outlook report by TechFlow Research. All judgments and recommendations cited herein reflect JPM’s views—not those of TechFlow Research—and do not constitute investment advice.

Sell-side reports are inherently biased toward bullishness. JPM also serves as investment banker to several companies named in this report. Its value lies in its framework and data—not any single conclusion. Focus on logic—not just directional calls.

Markets involve risk; decisions must be made independently.

Data sources: J.P. Morgan Wealth Management Mid-Year Outlook 2026 · Bloomberg · FactSet · U.S. Bureau of Labor Statistics · IEA · METR · Renaissance Capital

TechFlow Research · 4 June 2026

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News