Standing in the Light: A Comprehensive Guide to Optical Modules and the CPO Industry Chain

TechFlow Selected TechFlow Selected

Standing in the Light: A Comprehensive Guide to Optical Modules and the CPO Industry Chain

Standing in the light, walking alongside the light.

Author: Xiao Bing, TideFlow Research

June 1, 2026, Taipei Pop Music Center. Jensen Huang, clad in his signature leather jacket, unveiled the Vera Rubin architecture and a new blueprint for AI factories. Beneath this highly anticipated keynote, a central theme dominating the first half of 2026 has become unmistakably clear:

NVIDIA is betting big—on light.

In March, NVIDIA invested $2 billion each in Lumentum and Coherent to secure capacity and technology roadmaps for next-generation silicon photonics lasers. In May, NVIDIA committed another $500 million in partnership with Corning—the century-old fiber optics giant—to boost U.S.-based optical interconnect manufacturing capacity tenfold and increase fiber production by over 50%. On June 2, Huang declared directly at the event: “Marvell is poised to become the next trillion-dollar company.”

Stand in the light. Believe in the light. Once an internet meme on China’s A-share market, this phrase is now being turned into an industry consensus—by Jensen Huang, backed with real capital.

Imagine building 10,000 skyscrapers in a massive city—each housing tens of thousands of genius mathematicians (GPUs), all computing vast numbers of problems every second. Here’s the question: How do these mathematicians transmit their answers? And how do buildings coordinate with one another?

If you only build country lanes (traditional copper cables) between them, then no matter how many geniuses you have—or how fast they compute—their results will stall in transit. The entire city grinds to a halt.

This is the very real bottleneck facing today’s AI data centers.

Since ChatGPT’s explosive debut, AI has propelled GPUs (compute), HBM (memory), and CPUs (orchestration) into the spotlight—spawning one trillion-dollar company after another. Yet within AI infrastructure lies a critically overlooked piece: data transmission.

And the core physical medium enabling that transmission is the optical module.

As conventional optical modules begin falling short of AI’s insatiable demands, a next-generation technology—CPO (Co-Packaged Optics)—is rapidly rising to prominence.

This article walks you from “What is an optical module?” to “Why CPO is the future,” and finally to “Which companies across the value chain are worth watching”—all explained in plain language, unpacking this trillion-dollar赛道.

I. Optical Modules: The “Simultaneous Interpreters” of Data Centers

1.1 Why Light?

Inside data centers, chips communicate using electrical signals—akin to electrical impulses in the human nervous system. But electrical signals suffer from one fatal flaw: they don’t travel far, and distort easily at high speeds.

Transmitting electrical signals over copper cables resembles pushing water through a pipe: the longer the distance, the greater the pressure drop; the narrower the pipe, the lower the flow rate. Copper cables currently max out at ~2 meters in reach and ~1.8 TB/s in bandwidth.

Optical signals behave entirely differently. Light traveling through optical fiber is like a bullet flying through a vacuum tube—experiencing almost no attenuation, moving at extreme speed, and immune to electromagnetic interference. A single hair-thin fiber can theoretically carry dozens of Tbps simultaneously.

But here’s the catch: chips only “understand” electrical signals, while optical fiber only “carries” light signals.

Hence we need a “simultaneous interpreter”: converting electrical signals into light for transmission, and light back into electrical signals upon reception.

That interpreter is the optical module.

1.2 What’s Inside an Optical Module?

Disassembling an optical module reveals it as a precision translation box, composed of several key components:

Transmitter (Electrical → Optical):

- Driver: Amplifies weak electrical signals from chips to levels strong enough to modulate laser output—like a power amplifier before a microphone. Without it, the laser “can’t hear.”

- Modulator: Takes the amplified electrical signal and controls light intensity and timing—“writing” digital 0s and 1s onto the light beam. It doesn’t emit light itself—it merely “directs” it.

- Laser: The actual “light source,” emitting stable, continuous laser light. The modulator controls its output to “write.”

Receiver (Optical → Electrical):

- Photodetector / Photodiode (PD): Receives incoming light signals via fiber and converts them into extremely weak currents—like the retina converting light into neural signals.

- TIA (Transimpedance Amplifier): PD-generated current signals are too weak; the TIA amplifies them into voltage signals usable by downstream circuitry—effectively turning a whisper into normal speech volume.

Signal Restoration:

- DSP (Digital Signal Processor): Electrical signals degrade over long distances. The DSP acts like Photoshop—restoring clarity to blurred images. It consumes significant power and ranks among the most expensive, power-hungry components in an optical module.

- CDR (Clock and Data Recovery): Re-establishes precise timing from degraded signals—ensuring exact spacing between 0s and 1s. Typically integrated into the DSP.

Optical Pathway:

- Waveguide: Microscopic “fiber-like” channels etched directly onto the chip, guiding light propagation.

- Fiber Interface: The physical port connecting the optical module to external fiber.

In one sentence: An optical module = light source + modulator + photodetector + driver/amplifier circuits + signal restoration ICs.

1.3 The “Speed Evolution History” of Optical Modules

The speed progression of optical modules parallels mobile communication generations:

Each doubling of speed triggers a full supply-chain upgrade and value re-rating. Today, we stand at the pivotal transition from 800G to 1.6T—explaining why optical modules have become the hottest A-share sector over the past year: the Wind Optical Module Index has surged over 500% from its 2025 low.

II. CPO: Welding the Interpreter Next to the Brain

2.1 Bottlenecks of Traditional Optical Modules

Traditional pluggable optical modules function like USB devices—plug-and-play, swap-and-replace. This design offers flexibility—but in the AI era, it hits three critical bottlenecks:

Bottleneck 1: Bandwidth Ceiling

Switch panel space is limited, and shrinking pluggable modules further is physically difficult. Currently, single modules top out at 1.6 Tbps; per-switch maximum is 51.2 Tbps. Future 3.2-Tbps modules may push switches to 102.4 Tbps—but that’s nearly the absolute physical limit for pluggable solutions.

Bottleneck 2: Power Explosion

Each GPU requires six pluggable optical modules, each consuming ~30W. Building a supercluster of one million GPUs would demand 180 MW just for optical modules—equivalent to a mid-sized city’s electricity usage. Utterly unsustainable.

Bottleneck 3: Signal Attenuation

Pluggable modules mount at switch panel edges—far from core ASIC chips—with long PCB traces in between. Higher speeds worsen signal degradation over this “last-mile” path, forcing additional DSPs—further increasing power draw and latency.

2.2 What Is CPO?

CPO (Co-Packaged Optics) adopts a simple core idea: place the interpreter directly beside the brain.

Specifically, the “optical engine” responsible for electro-optical conversion is integrated directly onto the same substrate or interposer as the switch ASIC—not as an external “plug-in” peripheral, but as chip-level “native integration.”

Analogy:

- Traditional optical module: Like making a phone call via Bluetooth headphones—signal leaves the phone, undergoes Bluetooth encoding, travels wirelessly, then gets decoded by the headset. Each step adds loss and delay.

- CPO: Like speaking directly into someone’s ear—eliminating all intermediaries, achieving both speed and energy efficiency.

According to NVIDIA, CPO improves power efficiency by 3.5×. IDTechEx forecasts the CPO market will grow at a 37% CAGR starting in 2026, exceeding $20 billion by 2036.

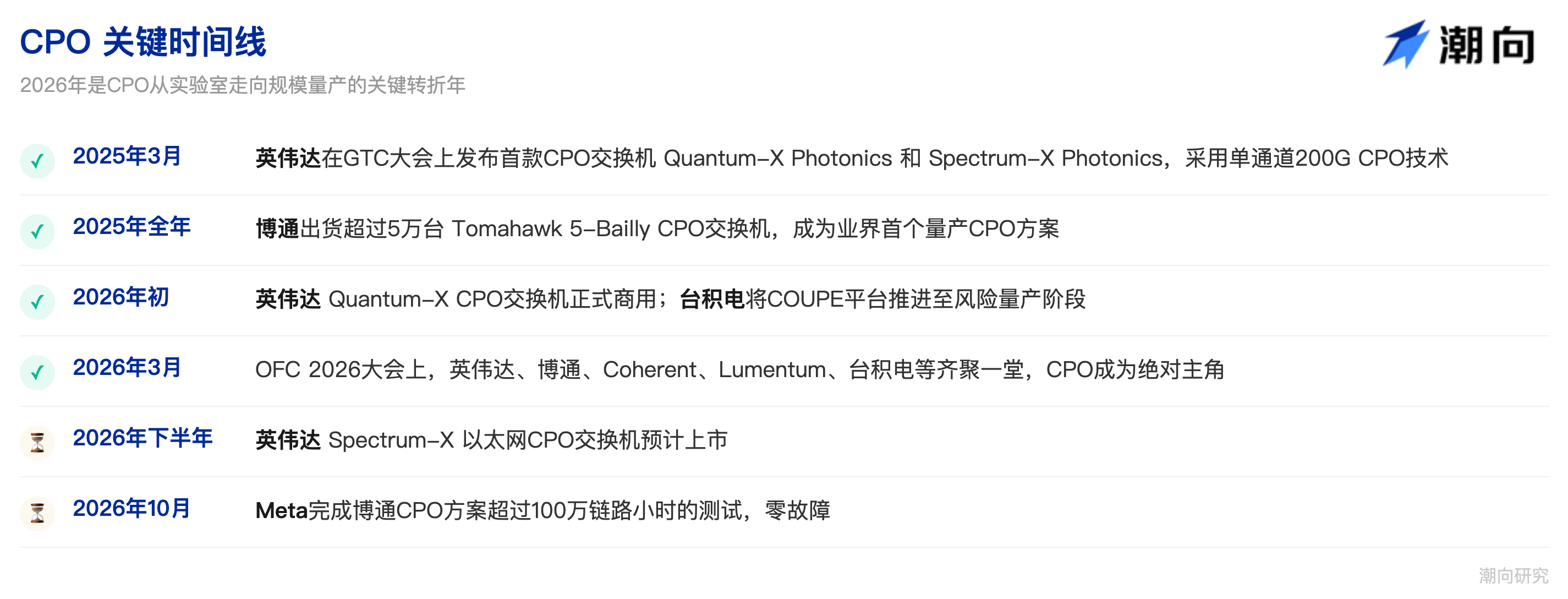

2.3 Key CPO Timeline

2.4 Challenges Facing CPO

While CPO represents the future direction, several hurdles remain:

Advanced Packaging Capacity: CPO requires “heterogeneous integration” of photonic and electronic circuits—demanding cutting-edge packaging technologies such as TSMC’s COUPE/SoIC. Current capacity remains constrained, yields still improving, and costs far exceed traditional solutions.

Maintenance & Repair: Faulty pluggable modules can simply be swapped out. But CPO modules are “welded” onto chips—making repairs extremely difficult. Redundancy and fault-tolerance mechanisms must compensate.

Thermal Management: High-density co-packaging of optical engines and chips risks localized temperatures exceeding laser operating limits—requiring more efficient thermal solutions.

Standardization: NVIDIA, Broadcom, and others promote competing architectures. No industry-wide standard yet exists—hindering coordinated R&D and production across the supply chain.

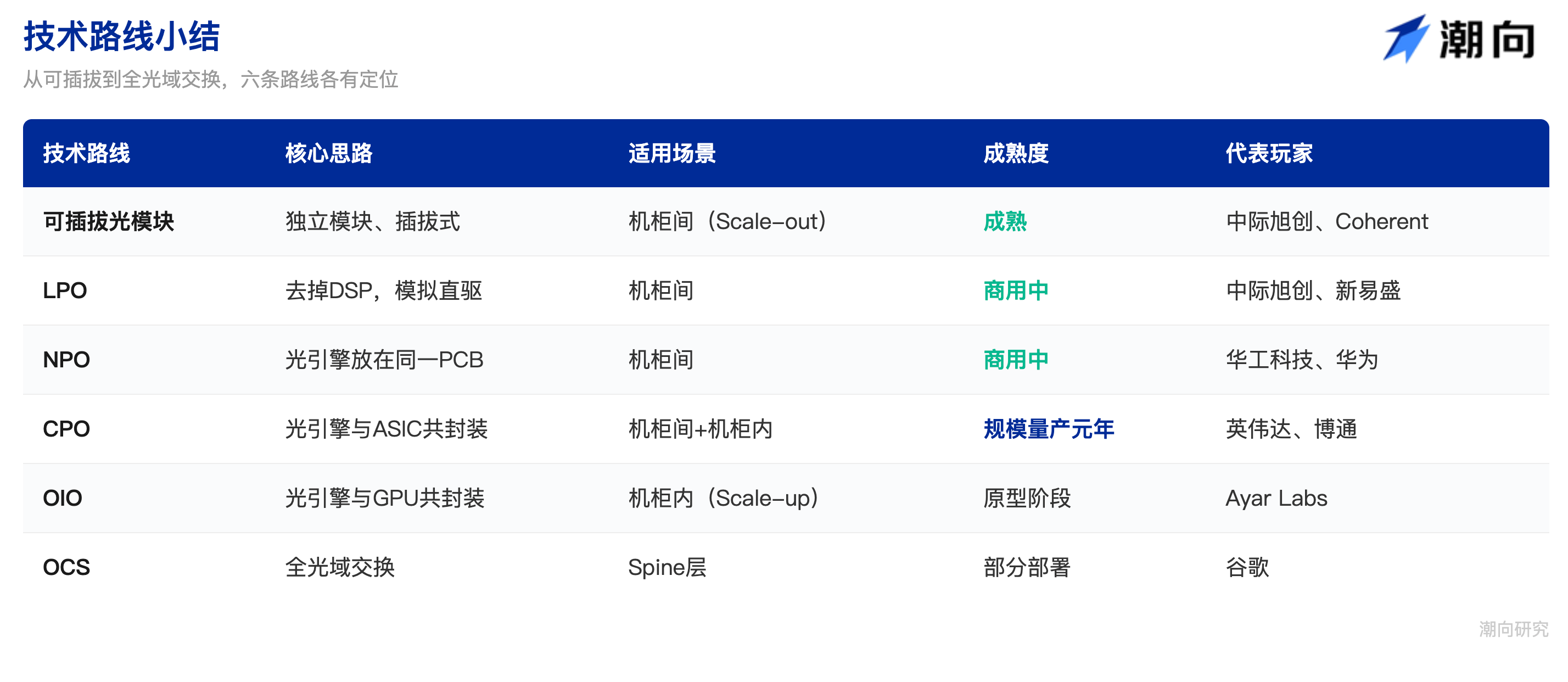

III. Full Technology Landscape: CPO Is Not the Only Contender

Beyond CPO, several parallel technical paths are advancing. Clarifying them reveals where each company stands competitively.

3.1 NPO (Near-Packaged Optics)

NPO is a “simplified version” of CPO—not integrating the optical engine onto the ASIC’s substrate or interposer, but placing it on the same PCB motherboard. Closer than pluggables—but not quite “face-to-face” like CPO.

A pragmatic compromise, especially in China—where advanced packaging capacity (e.g., TSMC-grade) is scarce—Alibaba, Huawei, and others actively promote NPO. Huagong Tech has already launched the world’s first 3.2T NPO product, deployed with top-tier customers.

NPO serves as a transitional phase toward CPO—dominant in China short-term, but evolving toward CPO long-term.

3.2 OIO (Optical I/O)

If CPO integrates optical engines with switch chips, OIO goes further—integrating them directly with compute chips (GPUs/XPUs), even at the silicon level.

OIO targets intra-rack scenarios (scale-up), replacing copper cables entirely. Ayar Labs leads here—having demonstrated a fully CPO-based scale-up rack prototype with Wistron at OFC 2026.

OIO is expected to enter large-scale deployment in GPU interconnect applications around 2028–2030.

3.3 LPO (Linear-drive Pluggable Optics)

LPO is a “slimmed-down” version of traditional optical modules—removing the highest-power-consumption component, the DSP, and relying instead on analog amplification. Benefits: lower power, lower cost. Drawbacks: stricter signal quality requirements, limited reach, and bottlenecks beyond 1.6T.

LPO extends the life of traditional modules—but doesn’t alter the overarching shift toward CPO.

3.4 OCS (Optical Circuit Switch)

OCS is a specialized switch that performs no electro-optical conversion. Instead, it routes light signals directly in the optical domain using “micro-mirror arrays”—tiny mirrors whose angles are adjusted to reflect light beams in different directions.

Google is OCS’s biggest advocate—replacing traditional spine switches with OCS. Advantages: ultra-low power (no EO conversion). Limitation: OCS only “forwards” light—it lacks “decision-making” capability (cannot inspect packet headers to determine routing). Thus, OCS suits spine-layer replacement only—not leaf switches.

CPO and OCS are complementary: OCS handles all-optical forwarding at the spine layer; CPO manages EO conversion at the leaf and server layers. They coexist.

3.5 Technology Roadmap Summary

IV. CPO Value Chain Overview: Who’s Eating This Cake?

CPO isn’t a standalone product—it’s a complex systems engineering effort involving numerous upstream and downstream players. Understanding these segments is key to identifying investment opportunities.

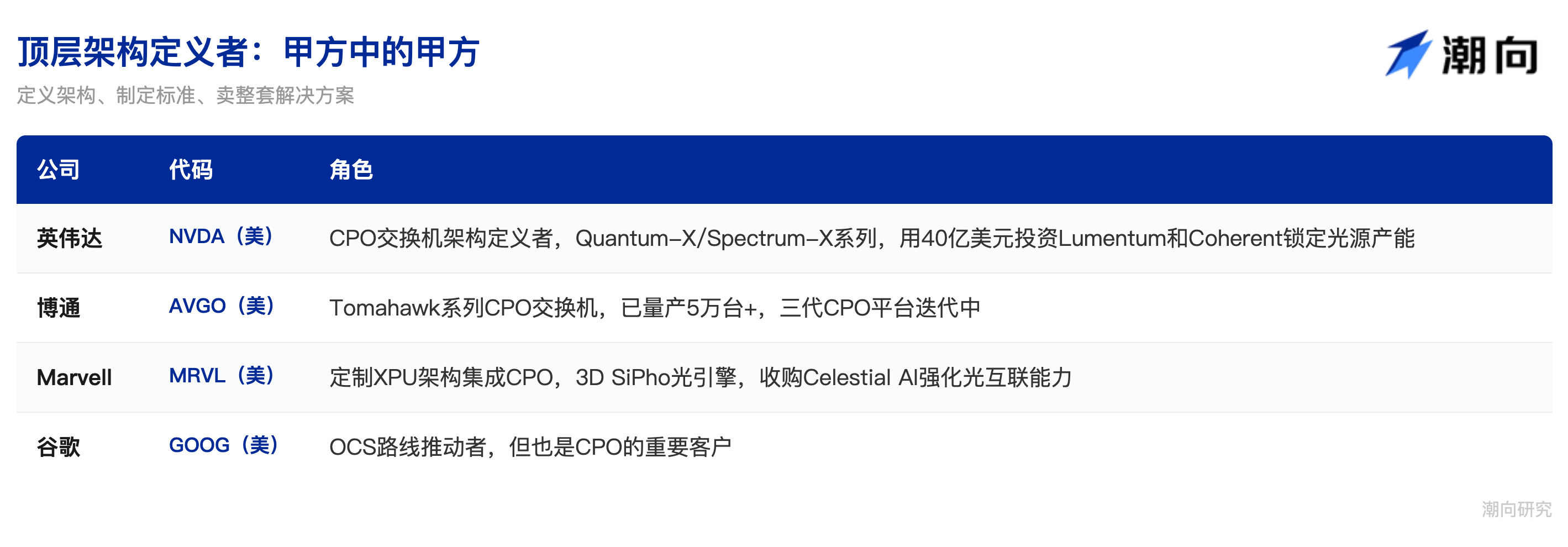

4.1 Top-Level Architecture Definers—The “Clients’ Clients”

One of the deepest shifts in the CPO era is the transfer of industry influence.

In the pluggable era, optical module vendors defined products independently and shipped directly. With CPO, optical engines are welded into chip packages—so whoever defines the chip architecture defines CPO. Influence shifts from optical module vendors to platform providers and switch-chip makers.

NVIDIA (NVDA): The most aggressive CPO proponent today. At GTC 2025/2026, it unveiled two major CPO switch series—Quantum-X and Spectrum-X—and in early 2026, committed $4 billion to Lumentum and Coherent plus $500 million to Corning—securing upstream laser and fiber capacity.

Broadcom (AVGO): The de facto pioneer in CPO mass production. Its Tomahawk-series CPO switches began with the first-gen Humboldt in 2021; Tomahawk 5-Bailly became the industry’s first mass-produced CPO solution in 2025, shipping over 50,000 units annually. Its third-gen 200G/lane platform is now underway. Broadcom’s strategy leans “selling shovels”—it supplies CPO switch chips to cloud vendors for in-house assembly, rather than building full systems.

Marvell (MRVL): Pursues a custom route—acquiring firms like Celestial AI to integrate 3D SiPho optical engines into its customized XPU architectures, delivering highly integrated CPO compute platforms for specific clients.

Google (GOOG): A unique case—it’s both OCS’s biggest advocate and a major CPO customer. Google uses OCS to replace spine switches but still needs CPO for EO conversion at leaf and server layers. So Google is both a CPO “competitor” and a CPO “buyer.”

4.2 Advanced Packaging & Manufacturing: Welding Light and Electricity Together

CPO’s core technical challenge lies in heterogeneous integration packaging—mounting photonic chips (silicon photonics or InP) and electronic chips (CMOS ASICs), fabricated on different materials and processes, onto the same substrate or interposer. This isn’t traditional “soldering components onto boards”—it demands sub-micron precision hybrid bonding, rivaling chip fabrication itself.

TSMC (TSM): The undisputed leader here. Both NVIDIA and Broadcom rely on TSMC’s COUPE platform and SoIC 3D packaging. In February 2026, TSMC advanced COUPE to risk-production status; its 6.4T-per-package solution with AMD is slated for high-volume production in H2 2026. TSMC’s advanced packaging capacity and yield directly dictate CPO’s rollout pace.

ASE (ASX): As the world’s largest OSAT, ASE plays a major role in CPO advanced packaging.

Amkor (AMKR): The U.S.-based Amkor is also vying for CPO foundry orders.

In China’s A-share market, HC SemiTek (002185) and Jiangsu Changjiang Electronics (600584) are primary beneficiaries in packaging. HC SemiTek’s packaging business benefits directly from CPO adoption; JCET (Changjiang’s brand) participates in advanced packaging and possesses heterogeneous integration capabilities. That said, CPO’s core packaging remains highly concentrated at TSMC—Chinese OSATs benefit mainly in peripheral support and mid-/low-end testing.

Notably, Fabrinet (FN)—a global EMS leader in precision optical manufacturing—fabricates high-end optical modules for Coherent and Lumentum, playing a role analogous to TSMC in semiconductors.

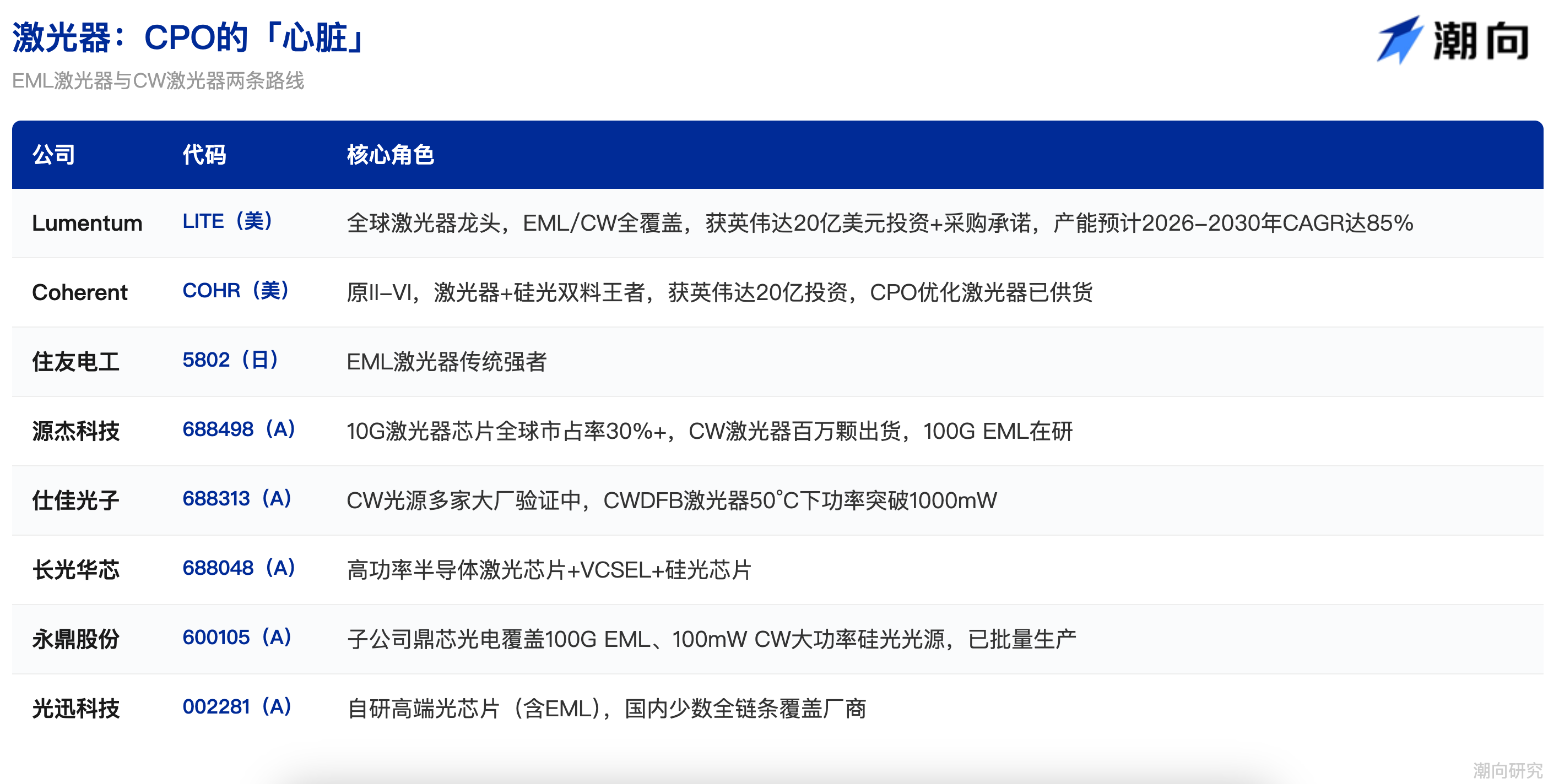

4.3 Lasers: The “Heart” of CPO

If chips are CPO’s “brain,” lasers are its “heart”—without light, EO conversion is impossible.

Two competing laser technologies exist:

EML (Electro-Absorption Modulated Laser) is the traditional approach—integrating laser emission and signal modulation onto one chip—ideal for high-bandwidth, long-distance transmission. Technical barriers are extremely high; global suppliers are few. Lumentum (LITE) pioneered 200G EML mass production in 2023 and demonstrated the world’s first 400G EML in 2025; Coherent (COHR, formerly II-VI) followed closely. Together, they hold >80% market share. Japan’s Sumitomo Electric (5802.T) and Mitsubishi are also EML leaders—but lag significantly in capacity expansion versus demand growth.

CW (Continuous-Wave) Lasers represent the emerging path—fully separating “light generation” and “modulation.” CW lasers emit steady, uninterrupted light; modulation is handled by silicon photonics chips. CW offers lower power consumption and better cost structure—naturally aligning with CPO and silicon photonics. Crucially, Chinese vendors have achieved breakthroughs on the CW path.

Yuanjie Technology (688498) holds >30% global market share in 10G laser chips; its CW lasers have reached million-unit shipments, and 100G EML development/testing is underway. Revenue growth in Q1 2026 hit 321%; net profit surged over 11×—making it one of the most leveraged upstream optical chip plays.

Shijia Photonics (688313) has validated and introduced CW light sources with multiple leading customers; its latest CWDFB laser achieves >1000mW output power at 50°C.

Changguang Huacore (688048) covers high-power semiconductor lasers, VCSELs, and silicon photonics chips.

Yongding Shares (600105)’s subsidiary Dingxin Optoelectronics operates China’s rare IDM laser chip fab—mass-producing 100G EML and 100mW CW high-power silicon photonics light sources. Accelink (002281) is among China’s few vertically integrated vendors capable of self-developing high-end optical chips—including EML.

In March 2026, NVIDIA invested $2 billion each in Lumentum and Coherent—with procurement commitments spanning 2027–2030. Lumentum will use the funds to build a new U.S. wafer fab—projecting 85% CAGR in laser capacity from 2026–2030. Coherent will expand indium phosphide (InP) capacity at its Sherman, Texas factory. These investments send a clear signal: lasers represent the largest supply-demand gap and highest strategic value segment in the CPO value chain.

4.4 Silicon Photonics Chips: The “Brain” of the CPO Optical Engine

Silicon photonics is the dominant implementation path for CPO optical engines. Its core concept: fabricate optical structures—waveguides, modulators, detectors—directly onto silicon chips using standard CMOS processes. This enables native large-scale integration, shared manufacturing infrastructure with electronics, and steep cost reduction with scale.

Overseas players lead in silicon photonics experience.

Broadcom (AVGO) is among the earliest semiconductor giants investing in silicon photonics—its CPO switch optical engines run on proprietary silicon photonics platforms.

Intel (INTC)’s Intel Photonics team boasts >10 years of silicon photonics R&D—though less visible in consumer markets, it remains a core player in data center optical interconnects.

Marvell (MRVL) integrated silicon photonics capabilities via acquisitions like Celestial AI—its 3D SiPho optical engine supports 200Gbps optical interfaces. Cisco (CSCO) acquired Acacia Communications in 2019 for ~$4.5B, gaining a leading silicon photonics coherent technology platform.

Domestic players are accelerating catch-up.

Accelink (002281) has achieved mass delivery of 400G and 800G silicon photonics chips—and jointly launched a 1.6T silicon photonics optical module with Cisco at OFC 2026.

Yuanjie Technology (688498) supplies high-power silicon photonics light sources—complementing silicon photonics modules.

Shijia Photonics (688313) leads in PLC splitters and AWG chips—and is expanding into silicon photonics chips.

Silicon photonics’ versatility enables compatibility with CPO, LPO, thin-film lithium niobate, and other cutting-edge paths—making it a strategic priority for major vendors. Zhongji Xunwei previously disclosed rapid growth in silicon photonics adoption across its 800G products—indicating silicon photonics isn’t exclusive to CPO but is also penetrating traditional pluggables.

4.5 Fiber Interconnect Components: A Pure Incremental Market Fueled by CPO

If earlier segments represent upgrades to existing markets, fiber interconnect components constitute a pure incremental market created by CPO. These components were rarely used in traditional pluggable modules—but become mission-critical in CPO architectures—making them one of the most leveraged segments in the value chain.

(1) FAU (Fiber Array Unit)

In traditional modules, fibers plug directly into standardized ports. CPO is different: fibers must align with waveguides on optical chip surfaces at micron-level precision—if misaligned, light coupling fails entirely. FAUs perform this alignment—precisely fixing multiple fibers to ensure perfect对接 with corresponding on-chip waveguides.

A traditional FAU costs ~$15; CPO-grade polarization-maintaining (PM) FAUs jump to $70–$100+. Per NVIDIA’s 115.2T switch, 72 FAUs are needed per unit—total FAU value per switch: $6,000–$7,000. FAU market size is projected to surge from ¥6–7B to >¥10B in 2025–2026—growing extremely fast. FAU expansion is difficult and yield-sensitive—supply remains tight.

(2) PMF (Polarization-Maintaining Fiber)

Traditional modules use direct modulation—insensitive to light polarization. CPO uses external lasers; if polarization shifts during fiber transmission, massive optical loss occurs. PMF ensures polarization stability throughout—acting as a “dedicated channel”—costlier than standard fiber, but unavoidable in CPO.

(3) Fiber Shuffle

Traditional modules typically use just two fibers (one Tx, one Rx)—manual cabling suffices. CPO increases fiber counts to dozens or hundreds—requiring high-density fiber rearrangement to route each precisely from optical engine to correct external interface. Fiber Shuffle is the data center’s “cable organizer”—indispensable in CPO.

(4) MPO (Multi-fiber Push-On Connector)

For CPO speeds ≥400G, parallel transmission requires 8 or even 16 fibers—yet panel space is severely constrained. MPO is a “multi-port plug” enabling simultaneous multi-fiber connection—demand exploding in the CPO era.

In this segment, Corning (GLW) dominates globally in fiber and optical materials—core supplier of FAUs and fiber, and NVIDIA’s $3.2B strategic partner. Corning’s optical communications revenue hit $6.3B in 2025—up 35% YoY—its largest and fastest-growing division. Private players US Conec and SENKO are global leaders in MPO/MTP connectors.

In China’s A-share market, Tianfu Communications (300394) is the undisputed leader—covering FAUs, lens arrays, and MPO connectors—and a core supplier to both NVIDIA and Broadcom CPO solutions. In H1 2025, active optical device revenue share rose 8 percentage points to 63.78%, driven by CPO packaging orders—gross margin: 42%.

Taichen Light (300570) leads domestically in MPO connectors—products certified indirectly by NVIDIA.

OptiLink (300620) focuses on lithium niobate modulators—but its 90-degree bent fiber arrays have entered mainstream supply chains, and it maintains unique positioning in OCS all-optical switching devices.

Changxin Bochuang supplies integrated photonic devices—covering MPO, AOC (Active Optical Cables), and AEC—with supply relationships established with Google and NVIDIA.

4.6 Fiber Interconnect Components: A Pure Incremental Market Fueled by CPO

Compared to traditional optical modules, CPO creates substantial new demand for precision fiber components—rarely used before, now essential—making this one of the most leveraged incremental segments.

(1) FAU (Fiber Array Unit)

In CPO, fibers must align with optical chip waveguides at micron-level precision—FAUs handle this. Traditional FAUs cost ~$15; CPO-grade PM-FAUs jump to $70–$100+. Per NVIDIA’s 115.2T switch, 72 FAUs are required—value per switch: $6,000–$7,000.

FAU market size is projected to surge from ¥6–7B to >¥10B in 2025–2026—growing extremely fast.

(2) PMF (Polarization-Maintaining Fiber)

Traditional modules ignore polarization; CPO uses external lasers—polarization drift causes massive loss. PMF guarantees stable polarization—acting as a “dedicated channel.”

(3) Fiber Shuffle

CPO dramatically increases fiber counts—requiring dense fiber rearrangement, like a data-center “cable organizer.” Traditional modules use just one Tx/one Rx fiber—no need for this.

(4) MPO (Multi-fiber Push-On Connector)

For CPO speeds ≥400G, 8 or even 16 fibers transmit in parallel. MPO is a “multi-port plug” enabling simultaneous multi-fiber connection—demand surging in the CPO era.

4.7 Optical Fiber & Cable: The Infrastructure Foundation of the CPO Era

Though not part of the CPO module itself, optical fiber/cable is the physical carrier of the entire optical interconnect—without it, light has nowhere to go. AI data center construction is driving fiber demand into a super-cycle.

This cycle’s simultaneous price and volume surge is exceptionally rare. In March 2026, China’s G.652.D single-mode fiber price spiked to ¥83.4 per core-km—up >160% from January, hitting an all-time high. The last comparable surge occurred during China’s broadband construction boom in 2018. On the demand side, the four major North American cloud vendors plan $72.5B in capex for 2026—up 77% YoY; Meta alone signed a $6B long-term fiber cable deal with Corning.

Corning (GLW) leads globally in fiber preforms—and with NVIDIA’s $500M backing, is boosting U.S. optical interconnect manufacturing capacity tenfold.

Yangtze Optical Fiber and Cable (06869/601869), dual-listed in Hong Kong and Shanghai, is the world’s largest fiber preform and fiber manufacturer. Its Q1 2026 net profit surged 226% YoY. At OFC 2026, its hollow-core fiber (91.2km spool, attenuation just 0.04dB/km) reached world-leading performance—representing the next frontier in fiber tech.

Zhongtian Technology (600522) leads domestically in optical cable—leveraging integrated submarine/land cable capabilities.

Hengtong Optic-Electric (600487) covers the full optical fiber/cable product spectrum—and maintains forward-looking deployments in F5G solutions.

FiberHome Telecommunications (600498) anchors Wuhan’s Guanggu optical communications ecosystem—backed by China Information and Communications Technology Group.

4.8 PCB/Substrates: The Skeleton of CPO

Both traditional optical modules and CPO switches rely on high-performance PCBs (printed circuit boards) and ABF substrates. But CPO raises PCB requirements fundamentally: higher signal integrity (tighter trace tolerances due to optical engines adjacent to ASICs), mandatory low-loss materials (e.g., Megtron 6/7—5–8× pricier than standard FR-4), and stronger multi-layer stacking. Meanwhile, optical module PCBs themselves advance to higher speeds—PCBs for 800G/1.6T modules command far higher value than prior generations.

Shenzhen Shenghong Technology (300476) is the undisputed AI PCB leader. It’s the core supplier of baseboards for NVIDIA’s GB200 servers—AI server PCB revenue share exceeds 50%. In optical communications, Shenghong has achieved mass production of 800G switch PCBs and industrialized 1.6T optical module PCBs—covering both CPO and optical module demand. Its global share of AI compute PCBs leads, making it the broadest cross-over play in “CPO + PCB.”

Dongshan Precision (002384) pursues dual tracks—AI compute PCBs and optoelectronic modules. Its Q1 2026 net profit grew 119%–152% YoY—driven primarily by accelerated AI infrastructure investment.

Shenzhen SMT (002463) is the traditional leader in high-speed data center PCBs—reliably supplying global mainstream servers and switches.

Shennan Circuits (002916) differentiates via high-end IC substrates—covering higher-value segments from PCBs to chip packaging substrates.

4.9 DSP & SerDes Chips: A Segment Redefined by CPO

In traditional pluggable modules, DSPs are the single highest-power, highest-cost component—responsible for repairing degraded electrical signals. Essential—but power-hungry.

One of CPO’s greatest power savings comes from eliminating standalone DSPs. This doesn’t eliminate signal processing—it redistributes it: core DSP functions integrate into the switch ASIC; CDR integrates into high-speed SerDes. SerDes (Serializer/Deserializer) resides inside the ASIC—converting internal parallel data into high-speed serial streams for transmission, or reconstructing received serial streams into parallel data. CPO pushes SerDes speeds from today’s 112Gbps toward 200Gbps and beyond—posing extreme demands on ASIC design.

Broadcom (AVGO) dominates integrated switch ASIC/SerDes design—its Tomahawk-series chips embed high-speed SerDes that drive CPO optical engines directly—no extra signal conditioning ICs needed.

Marvell (MRVL) excels in custom switch ASICs—tailoring integrated CPO compute platforms for specific clients.

In specialized SerDes and connectivity chips, Astera Labs (ALAB) positions as an intelligent connectivity chip provider—covering PCIe/CXL retimers and SerDes IP. Credo (CRDO) specializes in high-speed SerDes IP cores—holding significant share in data center connectivity. London-listed Alphawave Semi (AWE) is also a key player in high-speed connectivity IP.

4.10 Optical Module Vendors: From Lead Actors to Transformers

In the pluggable era, optical module vendors were the undisputed stars—sourcing optical/electrical chips and mechanical parts, assembling complete modules, and selling directly to data centers. But CPO integrates optical engines into ASIC packages—diminishing the independent module role. Optical module vendors face a fundamental question: Will our slice of the pie disappear?

Answer: Not in the short term—but transformation is inevitable long-term.

Short term: Pluggable modules remain in a super-boom cycle. Zhongji Xunwei (300308) posted Q1 2026 revenue of ~¥19.5B—up 192% YoY—and net profit of ¥5.7B—up 262% YoY. Before CPO fully replaces pluggables, demand for 800G/1.6T modules continues doubling. New Bright (300502) accelerates 1.6T product ramp. Of the global top 10 optical module vendors, seven are Chinese—Zhongji Xunwei holds #1.

Medium term: Vendors pursue multi-pronged strategies for the CPO era. First, continue supplying 800G/1.6T/3.2T pluggables—capturing peak-cycle profits. Second, offer transitional solutions like NPO and LPO—Huagong Tech (000988) launched the world’s first 3.2T NPO product for top-tier customers. Third, transform into CPO optical engine suppliers—shifting from “selling cars” to “selling engines.” This is natural: optical engine core processes (optical chip packaging, fiber coupling, test validation) overlap heavily with optical modules. Fourth, enter OCS all-optical switching—Zhongji Xunwei has entered this space using digital liquid crystal technology, backed by Google and Amazon.

Accelink (002281), a state-owned veteran in optical communications, has built a full chain—from chips to devices to modules to subsystems—and can mass-deliver 1.6T silicon photonics modules.

U.S.-listed Coherent (COHR) and Fabrinet (FN) remain core optical module players—Coherent is a dual leader in modules and optical chips; Fabrinet, the “foundry king,” manufactures virtually all high-end optical modules—and recently stated CPO is “more real than ever before,” already generating related revenue.

V. Investment Map: One Table for the Entire Value Chain

VI. Timeline & Investment Cadence

Short Term (2026–2027)

This is the “final feast” for pluggable modules—and the “zero-to-one” stage for CPO.

800G/1.6T pluggables remain supply-constrained—Zhongji Xunwei, New Bright, and other leaders post explosive earnings. Simultaneously, CPO begins initial mass shipments—primarily at the spine switch layer—driven by NVIDIA and Broadcom.

Core beneficiaries: Optical modules (Zhongji Xunwei, New Bright), lasers (Lumentum, Coherent, Yuanjie Technology), fiber interconnect components (Tianfu Communications, Taichen Light).

Medium Term (2027–2029)

CPO expands from spine to leaf; pluggable share in scale-out scenarios begins eroding. NPO peaks in China as a transitional solution. 3.2T modules commercialize.

Core beneficiaries: Advanced packaging (TSMC), external lasers (value surges 3–4×), FAU/MPO (price and volume rise).

Long Term (2029–2032+)

CPO penetrates scale-up (intra-rack); OIO technology commercializes in GPU interconnects—copper cables replaced en masse by optical interconnects. By 2030, CPO penetration in AI data center optical modules is projected to reach 35%.

Core beneficiaries: OIO-related players (Ayar Labs), silicon photonics platforms, the entire optical interconnect value chain.

VII. Epilogue: Walking with Light

If GPUs are AI’s “brain,” HBM is its “memory,” and electricity is its “food,” then optical interconnects are AI’s “nervous system”—without it, even the most powerful brain cannot connect to the world.

Jensen Huang put it plainly: Energy is our most critical resource. And CPO’s core value lies precisely in reducing data transmission energy consumption—fundamentally—by replacing electricity with light.

On this track, the U.S. holds architectural definition rights (NVIDIA, Broadcom) and high-end optical chips (Lumentum, Coherent); TSMC controls packaging manufacturing; while Chinese enterprises have built formidable competitive moats in optical module assembly (Zhongji Xunwei, New Bright), fiber interconnect components (Tianfu Communications), CW lasers (Yuanjie Technology), and fiber/cable (Yangtze Optical Fiber and Cable).

In coming years, investment logic on this trillion-dollar track will evolve—from “selling shovels” (optical modules) to “building highways” (CPO/OIO infrastructure). Ultimately, winners will be those who both keep pace with technological iteration—and secure control over critical bottlenecks in the value chain.

Disclaimer: This article provides only an overview of industry knowledge and does not constitute investment advice. Companies and securities mentioned herein are not recommendations. Investment involves risk—enter the market with caution.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News