The Most Dangerous Superstition in Venture Capital: The More You Value Founders’ Educational Background, the Worse Your Investment Returns

TechFlow Selected TechFlow Selected

The Most Dangerous Superstition in Venture Capital: The More You Value Founders’ Educational Background, the Worse Your Investment Returns

Investors make their worst decisions when they overly rely on founders’ academic credentials.

Author: Odin

Translation & Editing: TechFlow

TechFlow Intro: Global VCs loudly proclaim “invest in people, not projects,” but data from the University of Chicago reveals a harsh truth: investors make their worst decisions precisely when over-relying on founders’ educational credentials.

This credential obsession costs the industry hundreds of millions of dollars annually. The irony is sharper still: Thiel and YC—the firms most renowned for truly investing in people—don’t scrutinize résumés at all. Instead, they evaluate the complex, inseparable whole formed by founder and idea. For crypto investors, this serves as a stark warning against institutions that merely pattern-match elite academic backgrounds.

Long ago, eight researchers from Shockley Semiconductor walked into the San Francisco office of a young banker named Arthur Rock. These “Traitorous Eight” proposed starting a rival company. Rock saw something in them—perhaps a rare blend of brilliance and frustrated fury—and helped them raise capital to found Fairchild Semiconductor, widely regarded as the seed of Silicon Valley. Thus began Rock’s story: the first believer in the founding team, and thereby the first modern venture capitalist.

Rock held steadfastly to the belief that backing talent lies at the heart of venture capital. He often said that an outstanding management team could find great opportunities—even if forced to pivot out of its current market.

His peers disagreed. Tom Perkins of Kleiner Perkins focused on technology: Was it proprietary? Was it demonstrably superior to alternatives? Don Valentine—who had handled marketing at Fairchild before founding Sequoia—was obsessed with markets. In the mid-1980s, when Sequoia considered early investment in Cisco, most peers declined, deeming the founding team weak. Valentine invested anyway, reasoning that the networking market was so vast that even a mediocre team could sell massive volumes of equipment.

These three men birthed three distinct philosophies of American venture capital—but Rock won the cultural war. “Venture capital is a people business” is not just a catchy slogan; it places founders at the center of the narrative. And if you’re selling capital to founders, that’s exactly what they want to hear.

But is it really that simple? What does the “people business” actually look like in practice?

Normative Herding

Today, nearly every VC firm claims to prioritize founders.

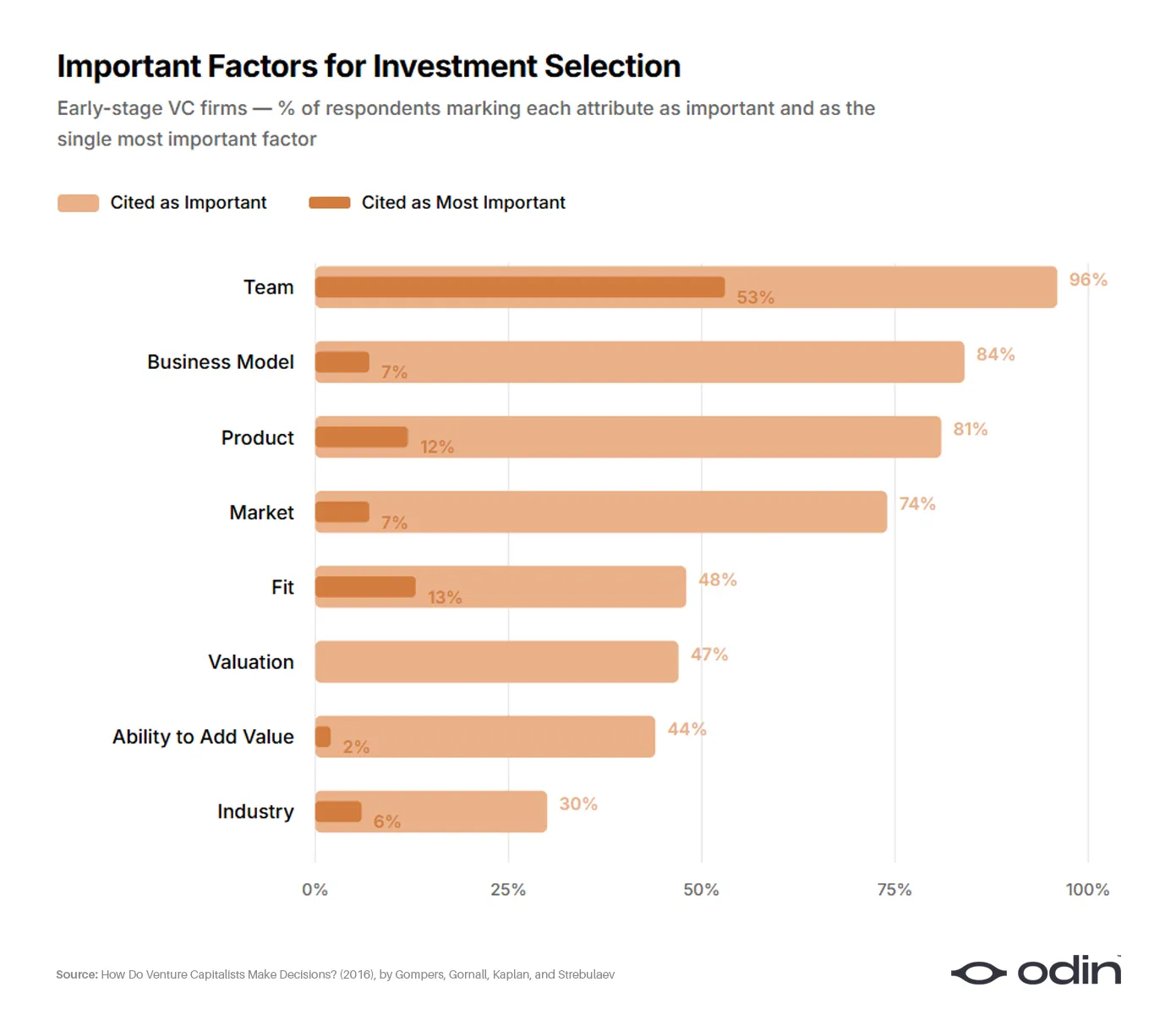

In 2016, four economists—Paul Gompers, William Gornall, Steven Kaplan, and Ilya Strebulaev—surveyed 885 venture capitalists across 681 firms to understand how they make decisions. This study remains the most comprehensive analysis of decision-making in the industry—and appears to have definitively buried Perkins’ and Valentine’s philosophies.

About 53% of early-stage respondents ranked founders as the single most important factor in deal selection. Business models and products—the traditional domain of Perkins—were selected by roughly 10%. Markets and industries—Valentine’s focus—by only about 6%. The remainder scattered across valuation, fund fit, and the investor’s own value-add capability.

“96% (92%) of VC firms consider the team an important factor; 56% (55%) consider the team the most important factor for success (failure). The team ranks highest across all sub-samples—but especially for early-stage and IT-focused VC.”

—“How Do Venture Capitalists Make Decisions?”, Gompers, Gornall, Kaplan, and Strebulaev

Looking at other survey responses, 9% of investors admitted to using no financial metrics whatsoever—a figure rising to 17% among early-stage investors. An industry so heavily reliant on qualitative judgment ought to have deeply contemplated its criteria—and tracked outcomes rigorously.

Unfortunately, the answer remains vague commitments: investing in the “best founders,” without clarifying what that means—or why.

“The findings suggest that venture capitalists are poor at introspecting their own decision processes. Even in controlled experiments where the amount of information considered was drastically reduced, VCs lacked deep insight into how they actually decide.”

—“Lack of Insight: Do Venture Capitalists Really Understand Their Own Decision Processes?”, Andrew Zacharakis and G. Dale Meyer

As a result, the founder-first approach has spawned an epidemic of lazy thinking—permeated by bias and credentialism. This, in turn, manifests in declining performance and recurring scandals involving fraud and negligence.

A Billion-Dollar Blind Spot

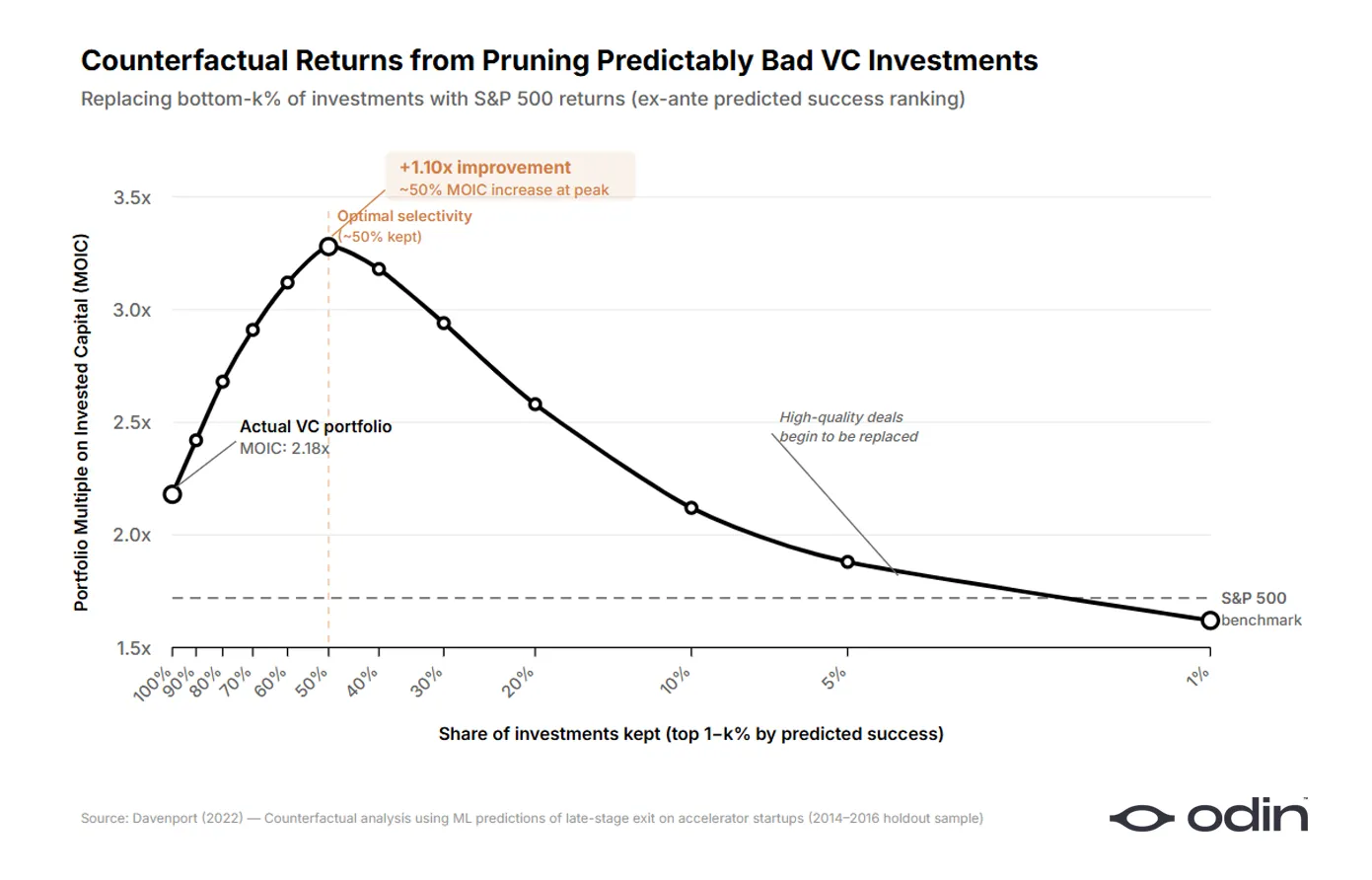

In 2022, Diag Davenport, an economist at the University of Chicago Booth School of Business, quantified the cost to the industry of this oversimplified mindset.

Davenport built machine learning models on a dataset of over 16,000 startups, representing more than $9 billion in committed capital. He trained the models exclusively on information available to investors at the time of decision—and asked: Of the investments VCs actually made, how many could have been identified ex ante as worse than simply allocating the same capital to standard public-market alternatives? The answer: roughly half.

By eliminating the worst half of investments and reallocating that capital to public-market alternatives, Davenport found that VC returns in the sample could have been 7–41 percentage points higher. Across his dataset, that represents over $900 million in avoidable losses. The cost of bad investments—expressed as the spread relative to external alternatives—averaged approximately 1000 basis points.

Davenport trained two parallel algorithms: one predicting which startups would become top-tier investments, the other predicting which would become the worst. When comparing the signals each model relied upon, a strange pattern emerged. The “good outcome” algorithm leaned heavily on product characteristics. The “bad outcome” algorithm leaned heavily on founder background. When investors made good decisions, they scrutinized ideas closely. When they made bad ones, they appeared to scrutinize teams instead.

To test for over-weighting, Davenport built a separate model using only founder education data—and asked: Among two companies that looked equally promising under the full model, would differing performance under the education-only model lead to different investment outcomes? The model indicated systematic over-weighting of education—and that this over-weighting was most severe for the startups that later performed worst.

“Investors appear genuinely convinced that the founder-first mental model is correct. This may cause them to overlook predictive features, sustaining a feedback loop in which they neither notice nor learn—consistent with the model and evidence presented in Hanna et al. (2014).”

—“Predictably Bad Investments: Evidence from Venture Capital”, Diag Davenport

Davenport’s paper is part of a growing body of research reaching similar conclusions: investors over-weight superficial founder attributes, leading to predictably bad investments (false positives) and predictably missed opportunities (false negatives).

There’s a structural explanation: In venture capital, “success” is easier to measure via incremental funding rounds than distant exits. If investment decisions devolve into simple checkbox exercises, friction around fundraising drops.

At some point, the industry convinced itself that fundraising ability itself is an ideal founder trait—and this logic became recursive. Investors began pattern-matching against prototypes most likely to raise the next round, making those prototypes easier to fund and reinforcing the pattern. Consequently, return quality broadly declined, while capital velocity (and fee income) accelerated.

Economist Daniel Kahneman explains this cycle: even sophisticated professionals can be seduced by simple, coherent narratives—if those narratives align with incentives—even when they produce clearly poor outcomes.

“Our statistical evidence of failure should have shaken our confidence in judgments of particular candidates, but it did not. It should also have made us more modest in our predictions, but it did not. We know as a general fact that our predictions are hardly better than random guesses, yet we continue to feel and act as though each specific prediction is valid.”

—“Don’t Blink! The Perils of Confidence”, Daniel Kahneman

The Paradox of Great Investors

This creates an intriguing puzzle. Data shows that over-weighting founder attributes leads to worse investment decisions—especially among the worst-performing deals. Yet some of the industry’s most successful firms are the most aggressively founder-first.

Founders Fund spent two decades backing unusual people—before others were willing. Peter Thiel launched the Thiel Fellowship specifically for young entrepreneurs without college degrees, yielding extraordinary success stories.

Y Combinator has operated for two decades on the premise of identifying exceptional founders. In fact, the program has been shown to reduce credentialism in venture capital by offering investors alternative signal sources.

If founder-first thinking were merely a systemic pathology, the firms most committed to it should perform worst. Instead, they perform best.

The answer is actually quite straightforward: When great investors say “founder-first,” they mean something far more complex than the industry’s shallow interpretation.

The Great Man Fallacy

The desire to reduce founder success to a checklist of predictable attributes is a modern manifestation of the Great Man Theory—the belief that history is shaped by exceptional individuals endowed with innate greatness, overlooking how success itself forges those qualities.

“A company with a strong track record of performance? Its leader appears visionary, charismatic, and powerfully articulate. A company struggling through hard times? That same leader suddenly seems indecisive, misleading—or even arrogant.”

—The Halo Effect, Phil Rosenzweig

Take Elon Musk, for example. Entrepreneurs like him shape investor expectations for hard-tech founders through countless stories about his cross-domain fluency, discipline, and certainty. So that’s what investors now seek in first-time founders—unaware that Musk developed those traits over time, and thereby denying others the chance to do the same.

Consider also Thiel’s investment in Mark Zuckerberg, then a Harvard dropout. Today, it’s routinely cited as proof of Thiel’s early ability to spot exceptional founders. Yet contemporary records show Thiel was drawn to Facebook itself, its early traction—and Zuckerberg’s specific framing of the problem of online identity.

If Zuckerberg had started a flower delivery startup, would Thiel have recognized anything special in him? It’s hard to imagine. It was the idea of how university social networks should function—and the precise form Zuckerberg had already given it—that constituted Thiel’s “magic.”

Indeed, at Andrew Ross Sorkin’s DealBook Conference, Peter Thiel was asked how he evaluates founders—and his answer aligned perfectly with the Facebook example.

“I don’t separate the idea, the business strategy, and the technology from the person very much. It’s all some kind of complicated packaged deal.”

—Peter Thiel, Co-Founder, Founders Fund

He explained that he cannot assess founder quality without evaluating the quality of the idea they’re pursuing—and cannot assess the idea without understanding how the founder shaped it. The two are inseparable.

Problems Worth Solving

Academia has developed a complementary argument. In a 2022 paper published in the Journal of Business Venturing Design, Mattia Bianchi (Stockholm School of Economics) and Roberto Verganti (Politecnico di Milano) argue that entrepreneurship has been systematically misunderstood as a problem-solving activity—when in reality, it is primarily a problem-finding activity.

In their framework, the founder’s most critical creative act is identifying and defining a problem worth solving. Everything else—pitch decks, go-to-market plans, product roadmaps—flows directly from the quality of that initial definition.

“Viewing problem-finding as a design act—not mere discovery—expands the potential impact of design practice: from creatively generating solutions, to creatively generating problems themselves. Speculatively redefining problems is another lever for breakthrough innovation, because unconventional problem formulations can open unexpected solution pathways.” —Bianchi and Verganti, “Entrepreneurs as Designers of Problems Worth Solving”

If this framework holds, then the core dichotomy of “jockey vs. horse” is fundamentally flawed. Evaluating founders must focus on the problems they choose to tackle—and the specific frameworks they use to understand those problems. Ideas cannot be assessed in isolation, either: they are material expressions of founders’ beliefs about what the world will look like a decade hence. The two mutually illuminate each other—and any investor claiming to assess them separately is almost certainly failing at both.

“By Their Fruit You Shall Know Them”

Nabeel Hyatt of Spark Capital articulates this integrated approach beautifully. When asked how to distinguish genuine executors from founders who merely tick many boxes superficially, his answer was unexpectedly direct.

“The way we differentiate slick charlatans from real executors is by looking at what they’ve built with their own hands. I’ve never evaluated a company and decided, ‘This person deserves a $15 million check,’ just by looking at their product or website. You look at the product—and then use the product to understand the person behind it.” —Nabeel Hyatt, General Partner, Spark Capital

The product embodies the founder’s ambition—and profoundly reflects their judgment, priorities, and the problem they chose to solve.

An investor who says “I invest in people” but doesn’t deeply examine the product is either investing in shallow patterns—or in charm and charisma. These are precisely the habits that reliably generate predictably bad investments.

Sam Altman expressed the same idea—albeit in slightly different language—during his 2016 talk with Keith Rabois at Khosla Ventures’ conference, sharing his heuristic for screening applications:

“The hardest-to-identify trait we look for is determination. In between, there are several themes we pay attention to: clarity of vision, communication skills, and the non-obvious brilliance of the idea—we study those very carefully. These aren’t always easy to judge correctly, but you can usually gather substantial data on them, and they’re easier to assess than determination.” —Sam Altman, Former President, Y Combinator

He didn’t say the founder was brilliant. He said the *idea* was brilliant—qualified as “non-obvious,” implying the founder chose a novel problem. He mentioned clarity of vision—suggesting scrutiny of how they perceive and articulate that problem. And, of course, the determination they bring to the process.

In Bianchi and Verganti’s terms, he described the founder as a designer of problems worth solving.

The Ocean in a Drop

When investors say they “invest in people,” they may mean one of two things.

The first meaning assumes attributes like pedigree, résumé, charisma, and prior fundraising success carry stronger signals than what the founder chooses to spend time building. At its core, this treats founders as interchangeable, rankable commodities. This is the version most directly refuted by Davenport’s data.

The second, rarer meaning assumes the object of evaluation is the unique alchemical fusion of person and idea. The investor’s job is to assemble a complete picture: the choice of problem, the form of the solution, the character of the team. Only then can they fully perceive the opportunity before them.

The two are easily confused—because they share the same vocabulary. Both speak the language of supporting people and celebrating human potential. The first is lazy—and richly rewarded by industry norms. The second is difficult, frequently misunderstood—but clearly the path to higher-quality investing.

The argument isn’t that investors should abandon qualitative team analysis and revert to Perkins’ and Valentine’s approaches. The conclusion is simply that teams cannot be effectively evaluated outside the context of what they’re doing—and attempting to do so is precisely where investors fall into problematic pattern-matching.

That’s why the atomic unit of entrepreneurship is neither founder nor idea alone—but their unity. Venture capitalists must stand far enough back to see both simultaneously—and evaluate them as a single entity.

Rather than obsessing over the old jockey-vs.-horse question, the investor’s job is to identify the centaur.

Note: A 2009 paper provided empirical support for prioritizing ideas over teams by analyzing how many companies had replaced their leadership teams or core products by IPO. However, this covered an era when VCs frequently installed new executives pre-IPO—and appears less relevant today.

Run your VC firm from your phone—with Odin.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News