$300 billion per quarter—AI consumes 80% of global venture capital

TechFlow Selected TechFlow Selected

$300 billion per quarter—AI consumes 80% of global venture capital

Venture capital in 2026 is increasingly defined by concentration, selectivity, and widening divergence—not uniform recovery.

Author: insights4vc

Translation & Editing: TechFlow

TechFlow Intro: insights4vc reviews the global venture capital market in Q1 2026. Total funding reached approximately $300 billion—setting a new all-time quarterly record—but 80% flowed into AI. OpenAI raised $122 billion in a single round, Anthropic $30 billion, xAI $20 billion, and Waymo $16 billion; these four deals alone accounted for two-thirds of global VC funding. Crypto funding showed signs of recovery—around $8.6 billion in Q1—but two-thirds of that occurred in March, and capital flowed predominantly toward stablecoin payments and compliant infrastructure; speculative projects remained sluggish.

Full Text:

The venture capital market in 2026 has entered a new phase. It no longer resembles a broad-based financing engine supporting startups across sectors; instead, it functions more like a late-stage capital allocation machine orbiting a handful of AI platforms. Behind the record-breaking numbers lies extreme concentration at the top, fragile market breadth, and a crypto recovery that remains highly selective.

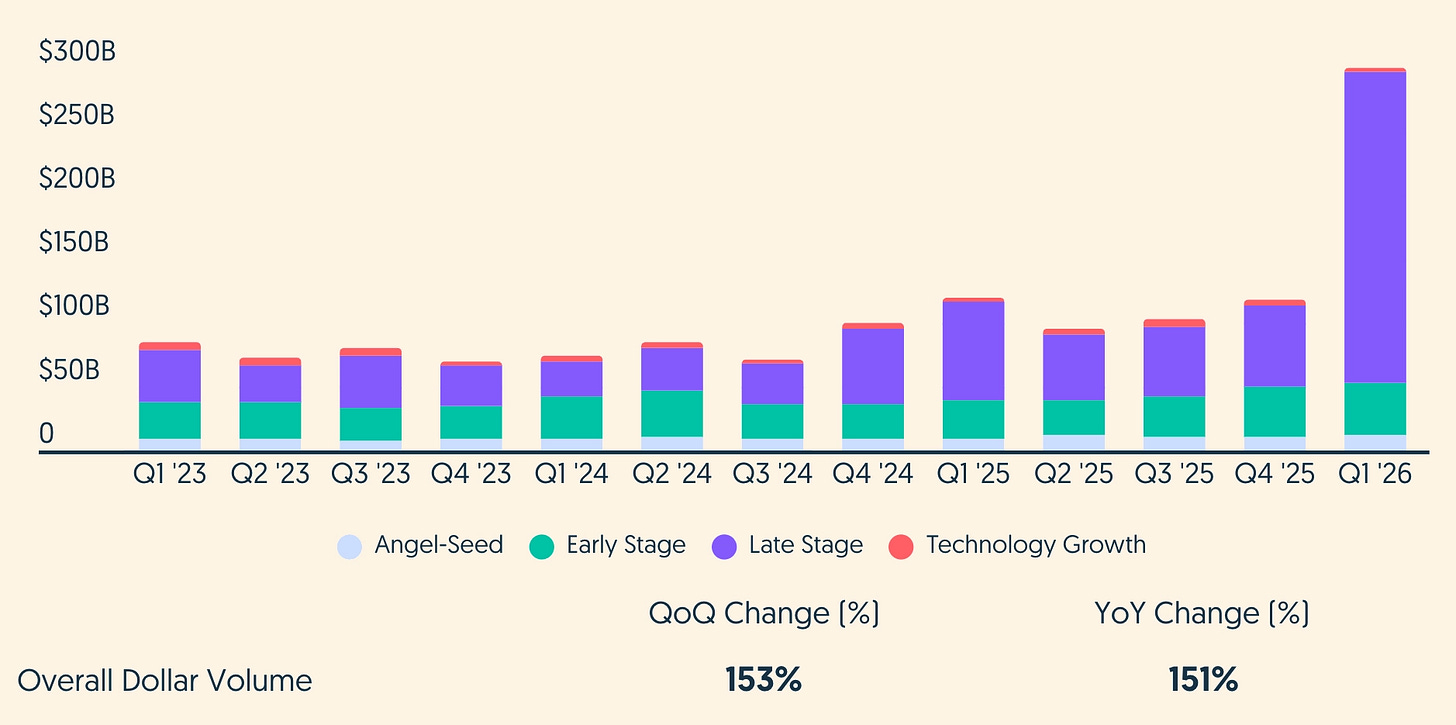

Caption: Global VC Funding in Q1 2026 (Source: crunchbase.com)

Key Takeaways

- Global VC funding in Q1 2026 totaled approximately $300 billion across ~6,000 companies—the highest quarterly figure on record. Late-stage and growth-tech rounds contributed the bulk of capital.

- AI captured the overwhelming majority of capital: Crunchbase estimates ~$242 billion, or 80% of the quarter’s total—up sharply from AI’s share a year earlier.

- The market exhibits a “dumbbell” structure: a small number of global strategic platforms secured unprecedented capital pools, while the broader volume of deals remains depressed, and most funds continue to face difficult fundraising conditions.

- Crypto and digital assets improved modestly from their lows, but the rebound is narrow and highly time-dependent. In some data sources, March’s surge accounts for most of Q1’s crypto VC funding.

- Within crypto, capital continues migrating toward regulated channels and utility-oriented infrastructure (stablecoin payments, custody, compliance, tokenization)—consistent with increasingly clear regulatory frameworks in the U.S. and EU.

- Outside AI, capital still flows to robotics (typically AI-integrated), defense tech, cybersecurity, and select fintech segments—but their relevance is increasingly framed by “AI adjacency” and sovereign/corporate strategic logic.

Q1 Data Overview

According to Crunchbase, global VC funding in Q1 2026 stood at ~$300 billion across ~6,000 startups—a rise of over 150% both quarter-on-quarter and year-on-year. This amount represents nearly 70% of the full-year 2025 VC total.

Yet record-breaking headline figures do not imply record-breaking breadth. By stage, late-stage funding totaled ~$246.6 billion across 584 deals; early-stage amounted to ~$41.3 billion across 1,800 deals; seed-stage reached ~$12 billion across ~3,800 deals. Even at the seed stage, some data show rising amounts but sharply declining deal counts year-on-year. In other words, average round size increased—but deal volume did not expand. Investors are concentrating time and capital on fewer targets.

A simple but useful distinction is to separate “total funding” from “total funding excluding outliers.” Just four mega-rounds accounted for a large share of Q1’s global VC total. Stripping out those outliers leaves roughly $100 billion—comparable to “strong but non-record” quarters in 2024–2025. Q1 2026’s record was mechanically dependent on a handful of transactions.

Geographically, U.S.-based companies raised ~$250 billion—~83% of global VC—further increasing an already elevated share. China ranked second (~$16.1 billion), followed by the UK (~$7.4 billion). This aligns with a basic reality: frontier AI and compute investment lands most easily in the U.S., where hyperscale cloud providers are dense, GPU supply chains are concentrated, and investors are willing to fund multi-year infrastructure burn.

AI Dominated the Quarter

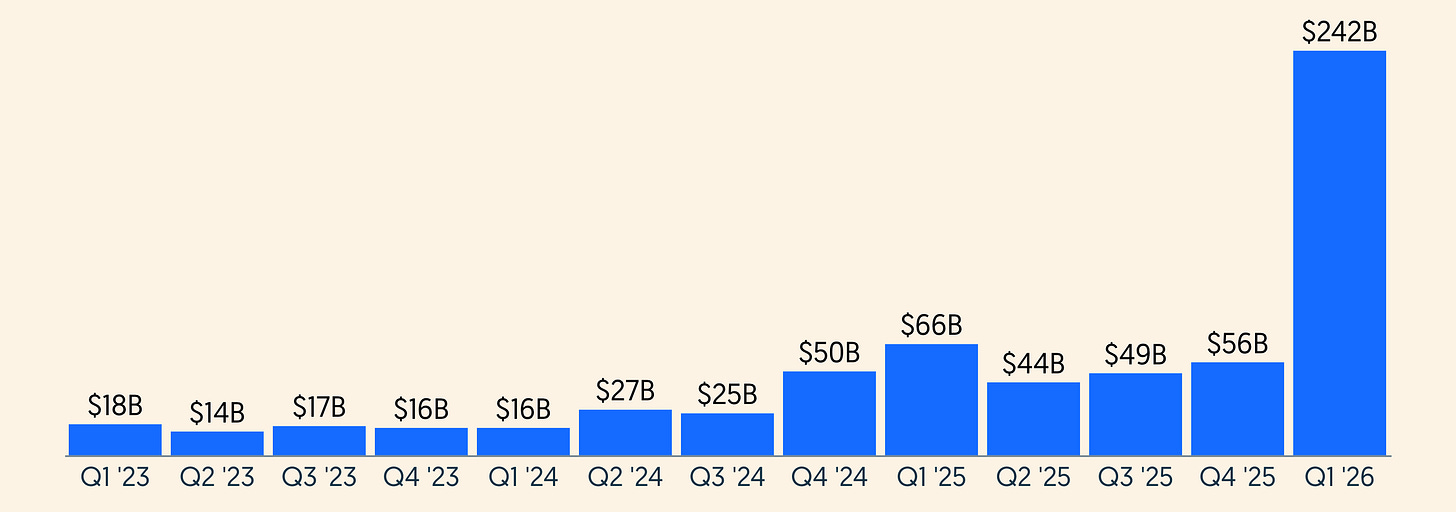

AI’s dominance in Q1 2026 is unmistakable. Crunchbase estimates AI-related companies raised ~$242 billion—80% of global VC. For context: AI funding in Q1 2025 was ~$59.6 billion, or 53% of that quarter’s total. Even accounting for database backfilling and definitional drift, the direction is clear: AI has evolved from the largest vertical in VC into, by capital-weighted measure, the VC market itself.

Caption: Quarterly Global AI Funding Trend (Source: crunchbase.com)

The shift goes beyond intensity of enthusiasm. The financing model itself is moving toward infrastructure underwriting—few companies’ funding rounds resemble capital markets events more than traditional VC. Four of the five largest VC rounds in history closed in Q1 2026: OpenAI ($122B), Anthropic ($30B), xAI ($20B), and autonomous driving company Waymo ($16B), totaling $188 billion—or ~65% of global VC.

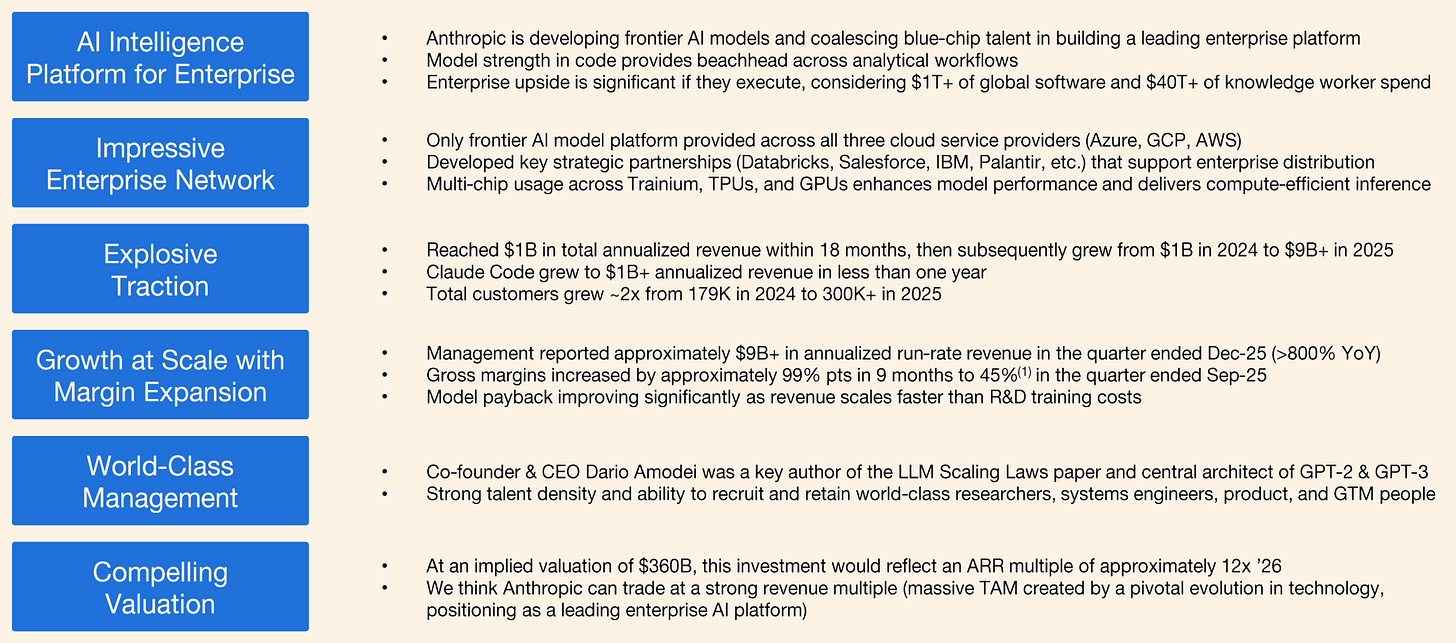

Caption: Anthropic – Coatue Forecast Model

Anthropic’s valuation logic is further supported by exceptionally strong operating metrics. According to Reuters, Anthropic’s annualized revenue reached ~$14 billion around its February 2026 funding round, with its Claude Code product alone generating >$2.5 billion in annualized revenue; enterprise subscriptions quadrupled in 2026. By early March, Reuters reported annualized revenue had risen further to ~$19 billion. Investor enthusiasm stems not only from the option value of cutting-edge models but also from accelerating enterprise monetization. This explains why Anthropic is increasingly viewed as a cleaner commercial AI exposure—particularly in programming and enterprise workflow infrastructure.

Caption: Coatue Projects Anthropic’s 2030 Valuation at $1.995 Trillion

One transaction epitomizes this paradigm shift. On March 31, OpenAI announced a $122 billion round at an $852 billion post-money valuation. The company explicitly identified compute acquisition as its core strategic bottleneck and unveiled an infrastructure strategy spanning multiple cloud partners and chip platforms. Two other frontier labs reinforced the same model: Anthropic’s $30 billion Series G in February (post-money $380 billion) was earmarked for frontier research, product development, and infrastructure expansion; xAI’s expanded $20 billion Series E in January likewise prioritized large-scale compute infrastructure buildout.

OpenAI’s record-setting round also exposed an important market tension. Though it remains the largest capital magnet in AI, reports indicate its shares have lost appeal in secondary markets—some institutional holders struggle to find buyers—while demand for Anthropic equity has strengthened. Bloomberg reports investors are shifting toward Anthropic, suggesting sheer scale may no longer suffice to sustain infinite demand for OpenAI at current valuations.

This point is critical because OpenAI’s latest round featured an investor composition unlike a traditional VC syndicate. It was a strategic financing anchored by key suppliers and ecosystem partners—including Amazon, NVIDIA, SoftBank, and Microsoft—as well as over $3 billion raised from individual investors via bank channels. Effectively, this resembled an infrastructure-support balance sheet mobilization around a company deemed systemically important to the AI stack—not a pure expression of broad market confidence.

This distinction matters. It implies that frontier labs can sustain massive primary-market funding even as secondary-market buyers grow more valuation-sensitive. Anthropic’s $30 billion raise at a $380 billion post-money valuation reinforces this: for many investors, Anthropic may offer a cleaner upside-to-price ratio relative to OpenAI at $852 billion. The broader implication is that late-stage AI capital is fragmenting—strategic capital is willing to support compute-intensive leaders at ultra-large scales, while financial capital seeks the next relative winner rather than today’s category leader.

From this perspective, Q1 2026 was not just an AI-funding record-breaker—it was also an early signal that valuation discipline is re-entering the space via secondary markets, even as primary-market round sizes continue expanding.

For institutional investors, a key segmentation is that Q1 2026’s AI funding should be broken into several subcategories with markedly different durability: frontier model companies, infrastructure & data centers, chips & compute supply chains, agents & enterprise workflow platforms, robotics & autonomous systems, and defense-related deployments. Most capital this quarter flowed to the most infrastructure-intensive layers, where competitive advantage is expressed through locked-in compute, distribution channels, and regulatory positioning—not just model quality.

Waymo exemplifies the “physical AI” effect. In February, it raised $16 billion at a $126 billion post-money valuation, explicitly targeting global expansion of autonomous mobility. Though often classified as autonomous driving, Waymo’s positioning and investment narrative increasingly sit within the broader “AI entering the physical world” category.

The resulting second-order effect is concentration risk. When four deals account for two-thirds of global quarterly VC, record-breaking funding figures become a fragile signal for startup health, job creation, and innovation breadth. For allocators: performance divergence between top-tier AI exposure and the rest of the VC ecosystem is likely to widen—not narrow.

Crypto’s Place in the New VC Cycle

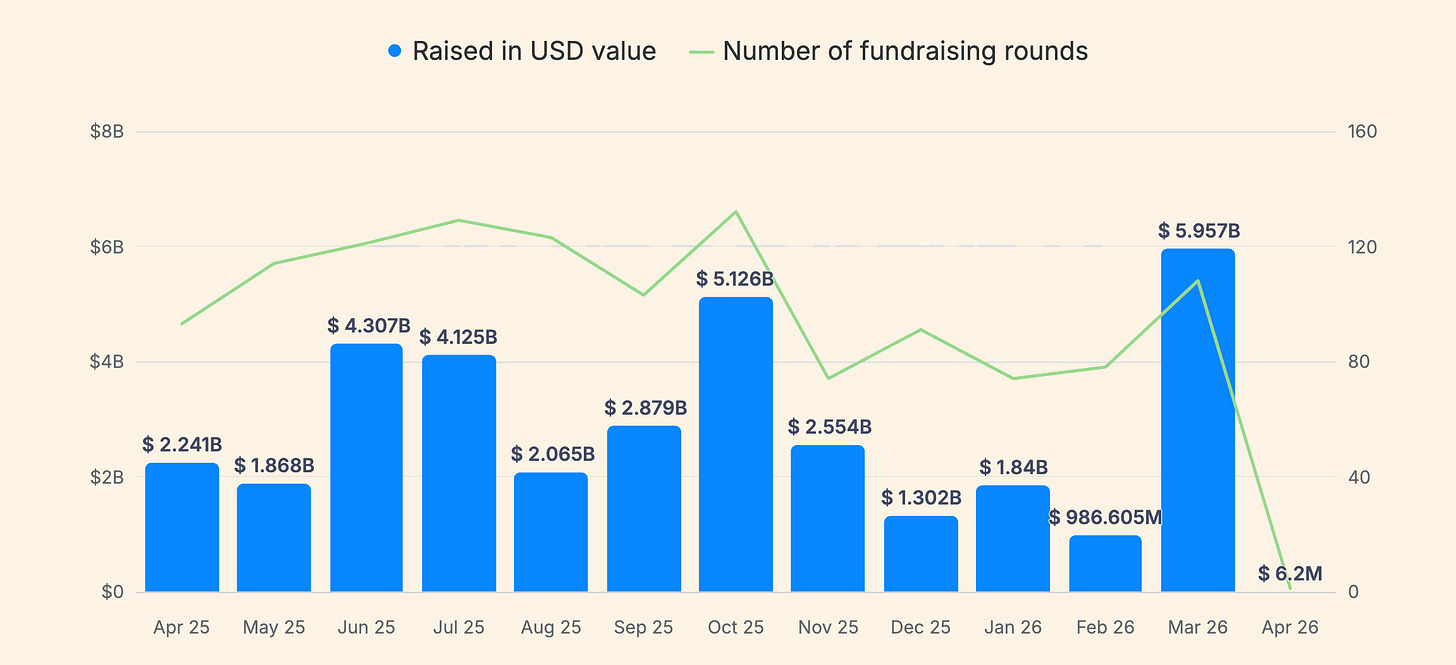

For professional investors, crypto and digital assets were the second-most relevant theme in Q1 2026—but absolute scale paled beside AI. Specialized crypto funding trackers typically place Q1 2026 in the high-single-digit billions, with large monthly volatility. CryptoRank reports 252 rounds totaling $8.632 billion. Of that, March alone contributed ~$5.95 billion (107 rounds)—meaning roughly two-thirds of Q1’s crypto VC landed in the final month.

Caption: Crypto Funding Trend (Source: cryptorank.io)

This temporal concentration is the first reason to treat the “rebound” cautiously. A quarter driven by a single month is vulnerable to data correction risks (delayed reporting, reclassification) and narrative risks (a few deals misread as broad-based recovery). A second caution is divergence among data providers. Other widely cited early-2026 crypto funding statistics show significant discrepancies in both amount and deal count—due to differing definitions (venture equity vs. debt, PIPEs, post-IPO funding, treasury strategies, acquisitions, undisclosed rounds).

Compared to historical cycles, Q1 2026’s crypto VC looks more like a continuation of the “utility and channel” phase—not a broad-based speculative boom. CryptoRank estimated $4.8 billion in crypto VC funding for Q1 2025, explicitly noting a single $2 billion investment drove much of that quarter’s data. Q1 2026 follows a similar pattern—crypto remains highly outlier-sensitive, but the narrative focus has shifted from exchanges to stablecoin infrastructure and institutional enablement.

Concrete examples support this “channel-first” view. Per Reuters, stablecoin infrastructure firm Rain raised $250 million in a Series C round at a $1.95 billion valuation, targeting stablecoin-linked payment cards and wallets. Reuters also reported OpenFX raised $94 million to expand its stablecoin-based cross-border payment infrastructure—positioned as faster settlement and lower cost than traditional correspondent banking. These are not “token launch” stories—they are payment and capital pipeline stories built on crypto rails.

Macro and regulatory context helps explain why stablecoins and tokenization continue attracting capital despite crypto price volatility. KPMG’s *FinTech Pulse* report notes global investment in “digital assets” (including VC, PE, and M&A) nearly doubled to $19.1 billion in 2025, citing key drivers: the full implementation of the EU’s MiCA regulation, the U.S. GENIUS Act, and rising market interest in stablecoins and asset tokenization (especially money market funds). For Q1 2026, this means: when crypto can plug into regulated financial workflows (payments, custody, compliance, tokenized cash equivalents), the investor base expands to include previously absent institutional capital.

Yet the rebound remains narrow. Even if Q1 2026 crypto VC reaches $8–9 billion in some trackers, against a $300 billion global VC total, crypto’s share remains in the low single digits. This creates a critical strategic trade-off: crypto may marginally benefit from improved risk appetite, but it competes for attention with larger-ticket, faster-adopting AI opportunities.

A final nuance is that crypto funding figures may be distorted by large potential financings from mature incumbents—financings unlikely to translate into broad-based startup ecosystem funding. Per Reuters, Tether downplayed discussions around its potential multi-billion-dollar funding after reports of investor resistance emerged—indicating that even large deals reflect later-stage balance sheet strategy more than ecosystem-level early-stage expansion.

The Broader Market Map

Beyond AI and crypto, Q1 2026 offers signals about the next VC cycle’s positioning—but many of these increasingly carry “AI adjacency” attributes rather than standing independently. Crunchbase’s data and commentary from late 2025 and early 2026 highlight robust funding momentum in robotics, defense tech, cybersecurity, and select fintech segments—united by themes of automation, sovereignty, and infrastructure.

Robotics serves as a good case study. Crunchbase reports ~$14 billion in robotics VC funding in 2025—up ~70% year-on-year and surpassing the 2021 peak. For institutional investors, this is less a “robotics hype” story and more an outcome of AI capital allocation: as models commoditize, investors seek defensible moats in hardware integration, deployment constraints, and regulated operational environments.

Defense and dual-use technologies similarly sit at the intersection of geopolitics and AI capability. Crunchbase reports $8.5 billion in defense tech funding in 2025—the highest on record. In Europe, the *Financial Times* described growing VC activity in AI and defense in 2025, tied to sovereign security concerns. These trends matter for Q1 2026’s market positioning because they reinforce a broader thesis: VC funding increasingly follows national capability agendas—not just TAM narratives for consumer software.

Geography remains a key differentiator. The U.S. claimed an unusually high share of global VC in Q1 2026. Europe, though not leading in aggregate totals, continues producing significant AI financings—including, per the *Financial Times*, Europe’s largest-ever seed round: a new AI startup raising over $1 billion. China’s VC landscape follows a distinct pattern: Reuters reports Chinese VC fundraising is expected to set a quarterly record, driven by state-led capital formation and policy pushes around AI and robotics—with government and state-owned entities as primary backers.

The implication is that “global VC” in 2026 is not one market, but at least three partially independent machines—the U.S. system dominated by private mega-rounds for frontier platforms; the Chinese system increasingly mediated by state capital allocation logic; and the European system sustaining innovation but constrained by expansion-financing gaps, yielding selective mega-rounds rather than broad late-stage depth.

Looking Ahead: H2 2026

The most useful way to think about the remainder of 2026 is scenario-based—because Q1’s headline totals are unusually sensitive to categorization and timing.

First, headline VC totals may remain elevated even if broad deal activity does not recover. Deal volume remains far below historical norms, while average round size continues rising. Q1 2026 appears more like a continuation than a reversal of this pattern. If mega-rounds persist, allocators may see “record VC” coexisting with emerging managers struggling to raise funds, seed funds lacking AI exposure facing distress, and founders outside thematic categories finding fundraising difficult.

Second, valuation discipline is more likely to be tested—not relaxed. Carta data shows early-stage valuations hit records by Q4 2025: median post-money seed valuations reached $24 million, and Series A valuations hit $78.7 million—while the top 10% of U.S. startups on its platform captured ~50% of 2025’s funding. Historically, this combination correlates with greater outcome dispersion: category leaders enter at higher entry prices, while median companies face heightened shutdown or consolidation pressure.

Third, exit environments have improved in aggregate but remain fragile in execution windows. Global exit activity has recovered from its trough, aided by IPO resumption and sustained M&A—but fundraising conditions remain weak, and public market volatility could shut windows at any time. Early 2026 saw Crunchbase note market volatility delaying some listings—even as private funding surged. The practical implication is that 2026 exits may remain uneven: open for elite assets, intermittently closed for others.

Fourth, for crypto investors and founders, the core question is whether crypto benefits from AI-driven risk-appetite recovery—or gets crowded out by it. Evidence is mixed. On one hand, stablecoin and payment projects are securing meaningful rounds and attracting mainstream VCs. On the other, AI funding’s sheer scale—and its ability to attract sovereign, corporate, and strategic capital—may divert marginal capital away from mid-sized crypto opportunities.

From insights4vc’s perspective, the most telling signal for the remainder of 2026 will be whether crypto funding can expand from channel infrastructure to genuine consumer adoption—and whether tokenization can scale from pilot projects to repeatable institutional workflows. The direction is constructive—especially in payments, custody, compliance, and tokenized financial infrastructure—but regulatory and prudential thresholds may still slow real-world implementation even as investor interest rises.

Conclusion

Q1 2026 was less a broad-based VC recovery and more the emergence of a new financing paradigm. Record-breaking headline figures were propelled by an unprecedented scale of funding for a small cohort of AI- and compute-intensive platforms, while underlying deal breadth remains far weaker than the surface numbers suggest. Crypto improved—but primarily in areas tied to regulated financial infrastructure, not broad-based speculative demand. For investors and founders alike, the signal is clear: VC in 2026 is increasingly defined by concentration, selectivity, and widening divergence—not uniform recovery.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News